Fannie Mae, Freddie Mac Add New Rate Buydown Disclosures

•February 13, 2026

0

Why It Matters

Providing granular buydown data lets investors better forecast prepayment speeds, protecting portfolio returns. It also aligns GSE reporting with regulator concerns about housing affordability and market stability.

Key Takeaways

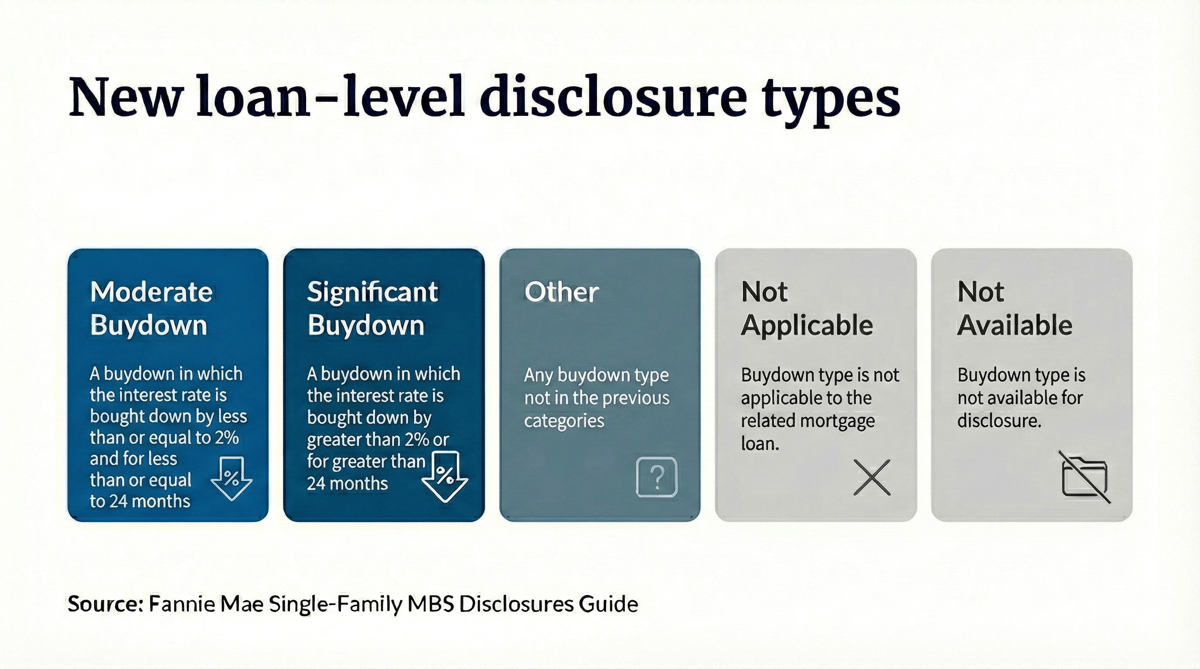

- •New loan-level buydown attribute L-117 effective April 20

- •Five categories distinguish moderate, significant, other, N/A, unavailable

- •Freddie uses MT, SE, O, 7, 9 identifiers

- •Retroactive data available for MBS issued after Jan 2022

- •Tracking buydowns helps investors manage prepayment risk

Pulse Analysis

Interest‑rate buydowns have become a common tool for builders and lenders to lower borrower payments in the early years of a mortgage. By embedding a loan‑level attribute (L‑117) into mortgage‑backed securities, Fannie Mae and Freddie Mac are giving market participants visibility that was previously only inferable at the security level. This granular data enables analysts to separate temporary rate reductions from longer‑term extensions, improving the precision of cash‑flow models used to price and hedge MBS portfolios.

For investors, the ability to identify moderate versus significant buydowns directly impacts prepayment assumptions. Temporary buydowns often trigger early refinancing when rates fall, accelerating principal return and forcing reinvestment at lower yields. With the new five‑category framework—moderate, significant, other, not applicable, not available—portfolio managers can adjust duration and convexity measures more accurately, reducing unexpected volatility. The retroactive inclusion of buydown information for securities issued after January 2022 further enhances historical performance analysis, allowing firms to back‑test strategies and refine risk‑adjusted return expectations.

Regulators have highlighted buydowns as a factor inflating new‑home prices, prompting the Treasury and FHFA to demand greater transparency. By standardizing disclosures, the GSEs address these concerns while supporting their broader strategic goal of eventual conservatorship exit. The enhanced reporting may also influence future policy discussions on mortgage pricing, builder incentives, and affordable‑housing initiatives, positioning Fannie and Freddie as more data‑driven participants in the evolving housing finance ecosystem.

Fannie Mae, Freddie Mac add new rate buydown disclosures

0

Comments

Want to join the conversation?

Loading comments...