Dispersion & Correlation Are Screaming Overbought. Downside Hedging Is Cheap.

Key Takeaways

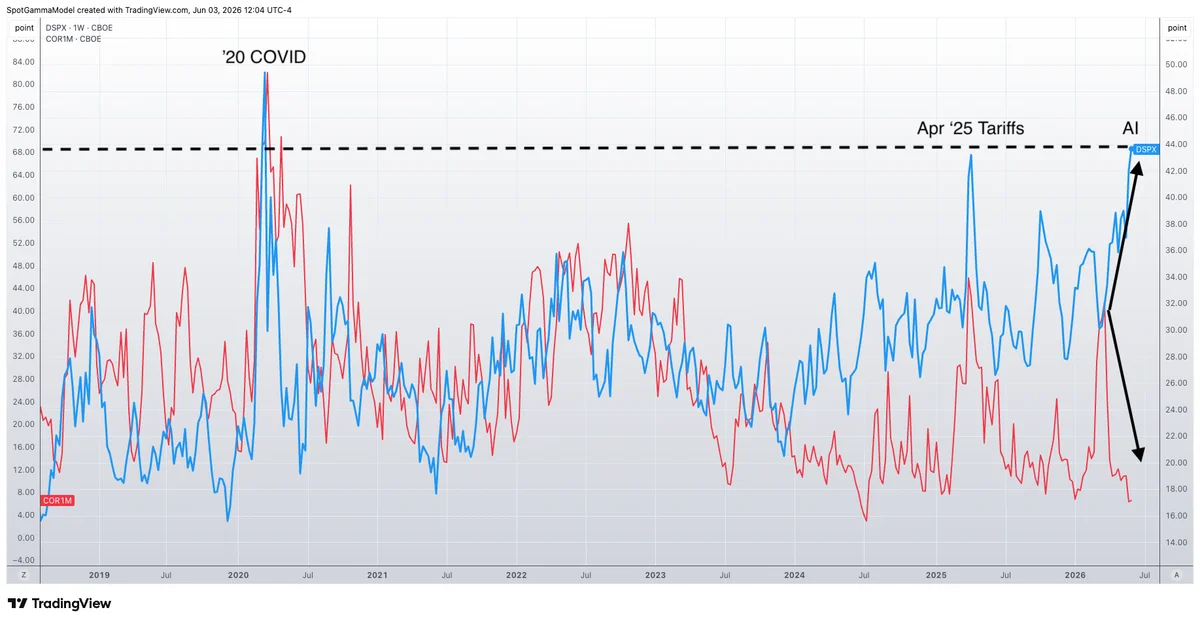

- •DSPX hits Covid-era highs, driven by AI stock frenzy.

- •COR1M falls to its lowest since July 2024, indicating low correlation.

- •Divergence signals extreme positioning risk and cheap SPY put hedges.

- •Options on SMH and QQQ show bullish skew, while SPY leans bearish.

- •Traders can exploit cheap downside hedges via SPY puts or call sells.

Pulse Analysis

The CBOE’s Dispersion (DSPX) and Correlation (COR1M) indexes have become barometers of market stress, measuring how differently investors price options across top U.S. stocks versus the broad SPX. When DSPX spikes, it means traders assign vastly divergent volatility to individual names, often reflecting a concentrated rally in a few sectors. Conversely, a plunging COR1M indicates that the market’s overall correlation is low, suggesting investors are not hedging the broader index against downside moves. The current combination—DSPX at Covid‑era peaks and COR1M near its July 2024 trough—signals an unprecedented split between stock‑specific optimism and systemic complacency.

That split is largely driven by the AI frenzy, where names like MU and SNDK have seen call premiums balloon while other sectors lag. The result is a skewed options landscape: bullish positions dominate in AI‑heavy tech stocks such as SMH and QQQ, whereas the SPY’s implied volatility remains subdued and its put options are markedly cheaper. For market participants, this creates a classic “risk‑on, risk‑off” paradox—individual equities appear over‑priced on the upside, yet the broader market lacks a priced‑in buffer for a correction. The cheapness of SPY puts, measured against inflated calls on AI stocks, offers a cost‑effective hedge for portfolios exposed to the same concentration risk.

Practically, traders can capitalize on this divergence by buying SPY puts, which now provide low‑cost downside protection, or by selling calls on over‑bought AI stocks, capturing premium while accepting the risk of a rapid rally. Structured strategies that blend cheap SPY puts with selective call spreads can further enhance risk‑adjusted returns. As the market approaches key macro events—such as the Iran conflict and upcoming earnings seasons—monitoring DSPX and COR1M will be essential for timing hedges. SpotGamma’s upcoming June 9 event will dive deeper into these positional analytics, offering actionable frameworks for leveraging the current options environment.

Dispersion & Correlation are Screaming Overbought. Downside Hedging is Cheap.

Comments

Want to join the conversation?