Institutional Investor Attention

A new Journal of Finance paper quantifies institutional investors' online news consumption and shows that attention is a scarce, tradable resource. Funds shift toward macroeconomic news when market volatility rises, and those that do so earn roughly 0.48% per quarter (about 1.9% annualized). Investors also focus disproportionately on stocks they already hold—about five times more reading than on non‑held names—boosting the value‑add of those positions, especially on buy trades. The research links attention patterns directly to superior portfolio performance.

Why Momentum Investing Has Been Struggling—And What Volatility Has to Do With It

Academic research by Haim Mozes links the surge in VIX volatility spikes to the recent underperformance of momentum investing. Over the 1994‑2024 period, spikes became more frequent and reversed twice as fast in the 2014‑2024 decade, reflecting heightened market efficiency....

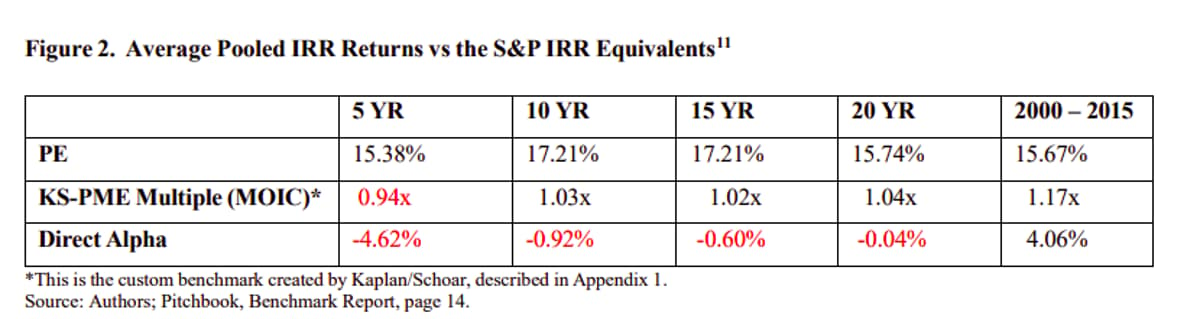

Should Your Mom Have Private Equity in Her 401K?

A new Harvard working paper challenges the push to add private‑equity (PE) to retail retirement accounts such as 401(k)s. Using cash‑flow‑aligned benchmarks, the authors find that over the past 15 years PE generated near‑zero alpha versus the S&P 500, and...

Rethinking Trend Following: Optimal Regime-Dependent Allocation

A new paper separates regime detection from position sizing, deriving Sharpe‑optimal weights for each market state. Applying the framework to two‑ and four‑regime specifications lifts out‑of‑sample Sharpe ratios from 0.208 to 0.506 and from 0.496 to 0.628, respectively, across 18...

Bank Monitoring with On-Site Inspections

A new Journal of Finance paper examines nearly 30,000 construction loans and on‑site inspection reports to reveal how banks monitor borrowers in real time. The study finds that banks focus inspections on riskier borrowers—low credit scores, high loan‑to‑value ratios, and...

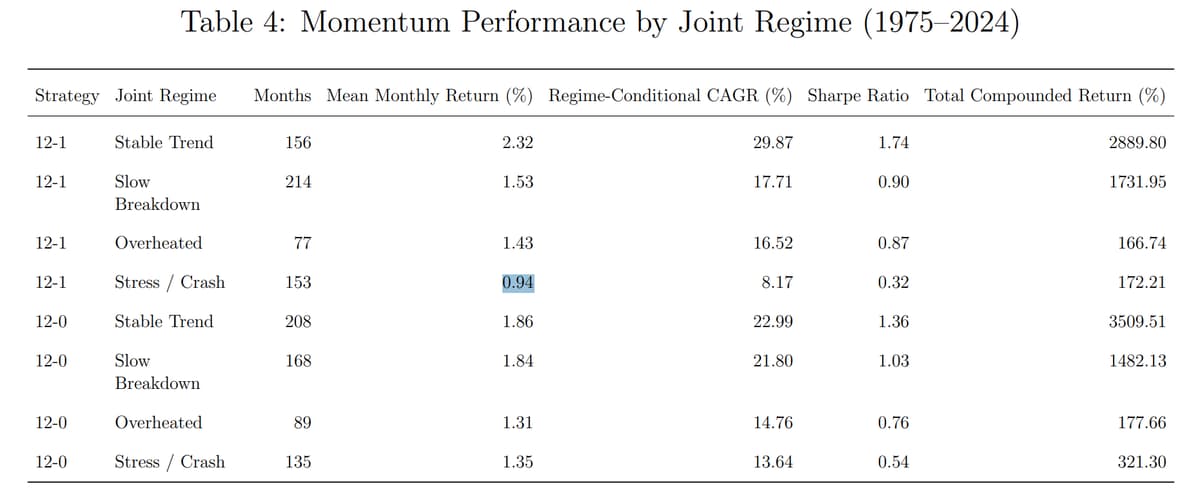

The Skip-Month Mystery: What Last Month’s Returns Are Really Telling You

A new study of 48 industry portfolios from 1975‑2024 questions the long‑standing “skip‑month” rule in momentum investing. By comparing a 12‑1 strategy that excludes the most recent month with a 12‑0 strategy that includes it, the research finds that the...

Asset Pricing and Risk-Sharing Implications of Alternative Pension Plan Systems

The Journal of Finance paper by Coimbra, Gomes, Michaelides, and Shen demonstrates that defined‑benefit (DB) pension funds are a powerful force in asset pricing, lowering risk‑free rates and boosting equity premia through their demand for safe assets. Their institutional constraints...

The Many Facets of Stock Momentum: Distinguishing Factor and Stock Components

The paper by Gerard and Jehl demonstrates a durable, stock‑specific momentum component that stems from price reactions around earnings announcements, distinct from traditional factor‑driven momentum. By isolating returns in short windows surrounding each firm’s earnings over the prior year, the...

The Performance of Small Business Investment Companies

The Small Business Investment Company (SBIC) program, created in 1958, lets private funds invest in U.S. small firms with SBA‑backed leverage. A 2026 Financial Analyst Journal study finds SBIC funds from 2000‑2020 generated an average net IRR of 15.9% and...

Unlocking Hidden Patterns: How Daily Returns Predict Future Stock Performance

Researchers Cakici, Fieberg, Neszveda, Bianchi and Zaremba introduced the Daily Return Information (DRI) signal, extracting chronological and rank information from a month’s daily returns using elastic‑net regression. The resulting Daily Return Information Factor (DRIF) delivers about 1.57% monthly (≈19% annualized)...

Increases CAPE Ratio Predictability with a Simple Adjustment

A new working paper demonstrates that a simple adjustment to the cyclically adjusted price‑earnings (CAPE) ratio—aligning index constituents and applying market‑cap weights—significantly sharpens its ability to forecast ten‑year equity returns. The revised Component CAPE delivers an out‑of‑sample R² of 0.575,...

Unlocking Hidden Value: How Corporate Language Reveals the Future of Intangible Investment

A new study introduces an "intangible intensity" metric that gauges how much corporate language in 10‑K filings focuses on knowledge, customer, and organization capital. By applying large‑language‑model text analysis to over 10,000 public firms from 2002‑2023, the researchers link higher...

The Best Defensive Strategies: Two Centuries of Evidence

The paper extends defensive‑strategy testing back to 1800, revealing that systematic trend‑following and a revised defensive‑absolute‑return overlay (DAR4020) consistently protect a 60/40 portfolio during its worst months. Traditional safe‑haven assets such as gold and continuously‑bought equity puts underperform or erode...

The Long Volatility Premium: Short the Market, Get Paid?

Patrick Kazley’s new paper argues that the apparent drag from buying put options is largely a hidden short‑beta exposure, not an inherent cost of long volatility. By neutralizing this beta, a pure long‑volatility factor delivers positive returns over time. The...