Credit Diverges: Jumbo Rises, FHA Slips

•March 10, 2026

0

Why It Matters

The divergence shows expanding flexibility for high‑balance borrowers while government‑backed financing tightens, reshaping affordability and risk across the mortgage landscape.

Key Takeaways

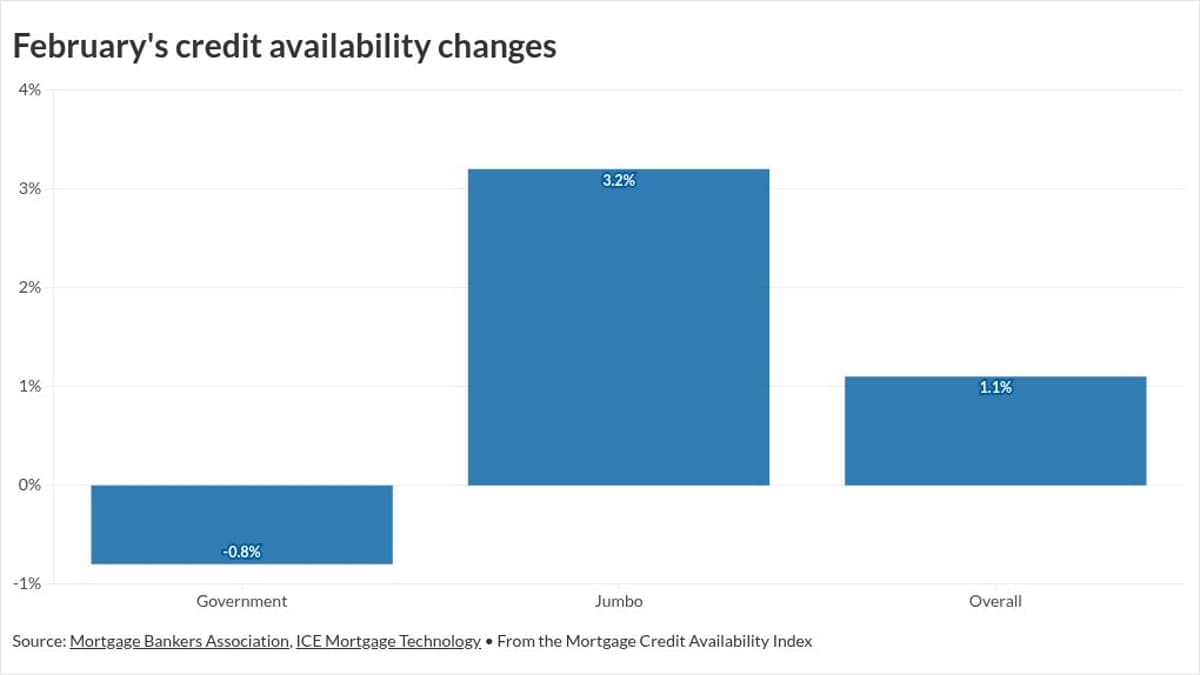

- •Jumbo credit availability up 2.9%, driven by non‑QM growth.

- •Government‑loan availability fell 0.8% amid rising FHA delinquencies.

- •Overall credit index rose 1.1% to 107.1, near historic low.

- •FHA delinquencies exceed 11%, prompting stricter LTV limits.

- •Conforming GSE market expanded 2% despite cautious underwriting.

Pulse Analysis

The latest Mortgage Credit Availability Index underscores a growing split between the jumbo and government‑loan segments. Jumbo lenders are loosening constraints, buoyed by strong home‑equity gains and a willingness to fund non‑qualified‑mortgage (non‑QM) products. This expansion reflects confidence that rising property values can absorb higher loan‑to‑value ratios, even as overall credit remains historically tight. By contrast, FHA and other government‑backed programs are pulling back, with delinquencies climbing above 11% and tighter LTV caps aimed at protecting the insurance fund.

For borrowers, the trend translates into more options for high‑balance loans but tighter pathways for low‑down‑payment or cash‑out refinance scenarios. Lenders are calibrating risk by raising credit‑score thresholds in the non‑QM space while maintaining prime standards for conventional loans. The heightened scrutiny on FHA loans, especially cash‑out refinances, could push marginal borrowers toward private‑label solutions or delay home purchases, influencing overall housing demand. Simultaneously, the surge in home‑equity buffers offers a cushion that may mitigate default risk for those who locked in favorable rates during the pandemic.

Looking ahead, policymakers and GSEs face a balancing act. The Trump administration’s push to limit GSE competition with FHA while supporting affordability adds uncertainty to the conforming market’s trajectory. If home‑price appreciation moderates, the reliance on equity buffers could weaken, prompting a reassessment of underwriting standards across all segments. Monitoring delinquency trends and LTV adjustments will be critical for investors and lenders aiming to navigate this divergent credit environment.

Credit diverges: Jumbo rises, FHA slips

0

Comments

Want to join the conversation?

Loading comments...