D.R. Horton, NVR, Taylor Morrison, M/I Homes Earnings Recap for Mortgage Lenders

Companies Mentioned

Why It Matters

The dip in homebuilder mortgage profitability signals tighter financing conditions that could restrain new‑home construction and affect related credit markets, while the persistent demand hints at a nuanced outlook for investors and lenders.

Key Takeaways

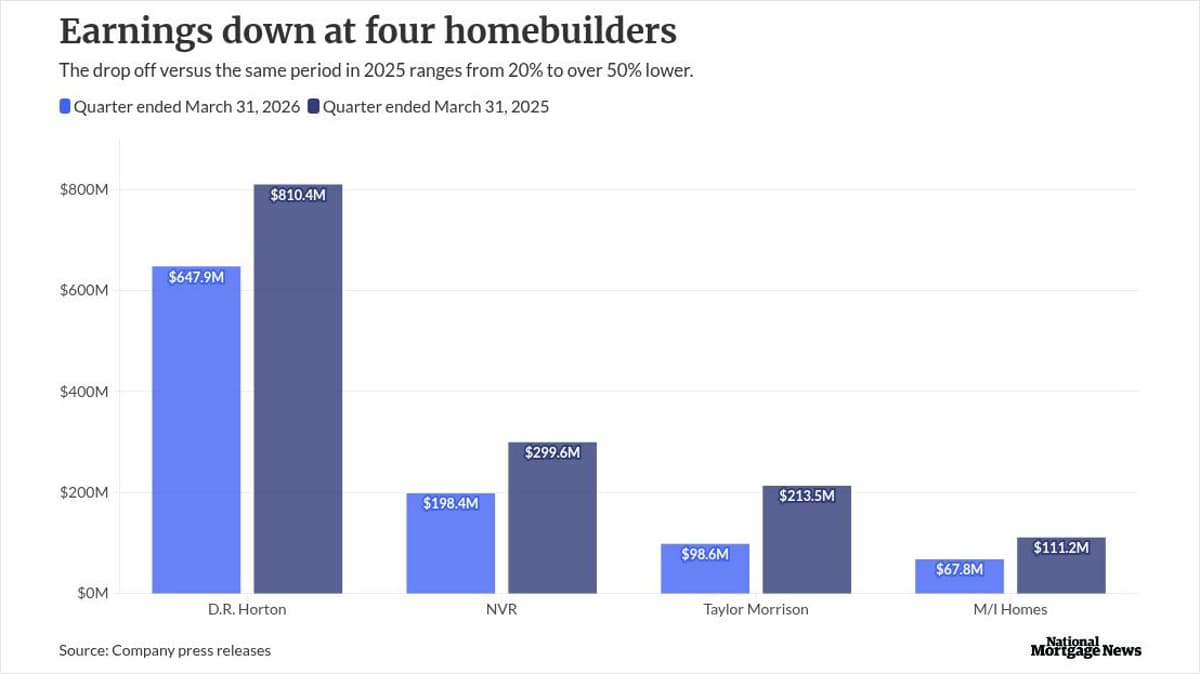

- •DR Horton mortgage pre‑tax margin 26.8% despite 20% net income drop

- •NVR mortgage volume fell 27% YoY, capture rate slipped to 83%

- •Taylor Morrison cut incentives >100 bps, backlog rose 23% sequentially

- •M/I Homes holds $3.2 B equity, $767 M cash, no credit‑facility borrowings

- •PulteGroup mortgage pretax income plunged 64% as volume dropped 7%

Pulse Analysis

The first‑quarter earnings round‑up for DR Horton, NVR, Taylor Morrison, M/I Homes and PulteGroup underscores how rising mortgage rates are compressing homebuilder financing margins. While pre‑tax income from mortgage banking fell across the board, the Mortgage Bankers Association’s Builder Application Survey showed an 11% year‑over‑year rise in loan applications, indicating that buyer appetite remains resilient despite higher borrowing costs. This dichotomy highlights a market in transition, where affordability pressures coexist with a still‑robust pipeline of new‑home demand.

Each builder’s mortgage operation tells a different story. DR Horton managed to sustain a 26.8% pre‑tax margin on $192.8 million of revenue, even as its overall net income slipped 20%. NVR’s mortgage volume plunged 27% to $1.05 billion, dragging its capture rate down to 83%. Taylor Morrison, confronting a 50% net‑income decline, trimmed incentives by more than 100 basis points and leveraged a higher mix of to‑be‑built orders to grow its backlog 23% sequentially. M/I Homes highlighted a solid balance sheet—$3.2 billion in equity and $767 million cash—while PulteGroup’s mortgage pretax income collapsed 64% as originations fell 7%, reflecting broader market softness.

For investors and lenders, the mixed signals suggest caution. The erosion of mortgage profitability could pressure homebuilders to rely more on inventory sales and less on financing revenue, potentially tightening credit conditions for prospective buyers. Yet the surge in loan applications and demographic drivers such as undersupply and household formation point to continued demand. Stakeholders should monitor builder incentives, capture rates, and inventory levels as leading indicators of whether the sector can weather a potentially "lost earnings" season and sustain growth in a higher‑rate environment.

D.R. Horton, NVR, Taylor Morrison, M/I Homes earnings recap for mortgage lenders

Comments

Want to join the conversation?

Loading comments...