Falling Pull-Throughs Signal Borrowers Closely Watching Rate Moves

Companies Mentioned

Why It Matters

The decline in pull‑throughs signals heightened borrower sensitivity to rate volatility, pressuring lenders’ pipelines and secondary‑market pricing. Understanding these trends helps originators adjust strategies amid tightening affordability.

Key Takeaways

- •Mortgage lock volume fell 5.4% in May amid rising rates

- •Pull‑through rates dropped to 76.7% for purchases, 65.3% for refinances

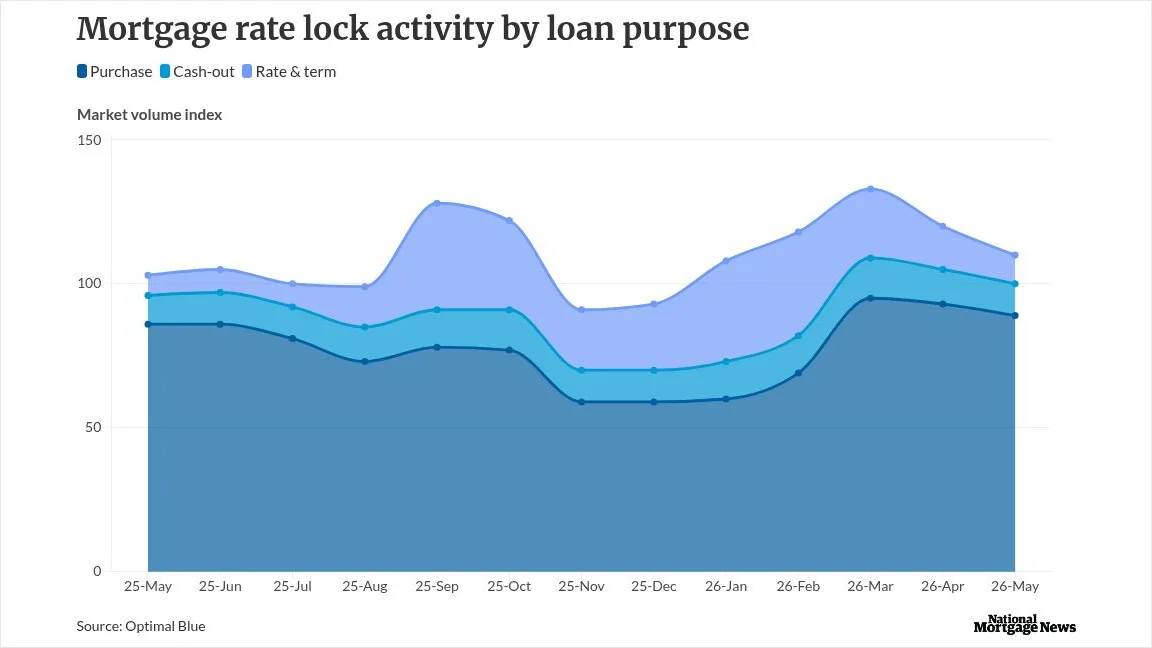

- •Purchases made up 81% of locks, refinances lowest since June 2025

- •Non‑conforming loans rose to 18.7% of lock volume

- •Adjustable‑rate mortgages reached 11% of production, highest since Oct 2022

Pulse Analysis

Rising mortgage rates have reshaped the U.S. home‑financing landscape, with Optimal Blue reporting a 5.4% month‑over‑month dip in lock volume for May. The 30‑year conforming fixed rate climbed 13 basis points to 6.44%, pushing borrowers to reconsider timing. While overall lock activity still outperformed the same month a year ago, the contraction highlights how rate pressure squeezes affordability and slows new loan commitments, especially in a market that remains purchase‑heavy.

A more nuanced signal emerges from pull‑through rates, which measure how many locked loans close. Purchases slipped to 76.7% and refinances to 65.3%, the steepest declines in recent months. This suggests borrowers are locking but then waiting for rates to stabilize before proceeding, a behavior that can strain lender pipelines and alter secondary‑market execution strategies. Agency MBS executions fell to 41% while cash executions rose, reflecting dealers’ hedging adjustments amid uncertain pricing.

The loan‑type composition also points to evolving borrower preferences. Non‑conforming mortgages climbed to 18.7% of May locks, and adjustable‑rate mortgages accounted for 11% of production—the highest share since October 2022. These shifts indicate a search for flexibility and alternative pricing as conventional conforming options become less affordable. Lenders that can efficiently service non‑qualified and ARM products may capture a larger slice of the market, while continued rate volatility will likely keep pull‑throughs under close watch.

Falling pull-throughs signal borrowers closely watching rate moves

Comments

Want to join the conversation?

Loading comments...