Foreclosure Starts Surge to Early 2020 Levels

•February 26, 2026

0

Companies Mentioned

Why It Matters

Rising foreclosures signal mounting payment stress for vulnerable borrowers, threatening lender portfolios and broader housing market stability. The divergence between overall delinquency decline and late‑stage distress highlights uneven recovery across borrower segments.

Key Takeaways

- •Foreclosure starts hit 42,000, matching early‑2020 levels.

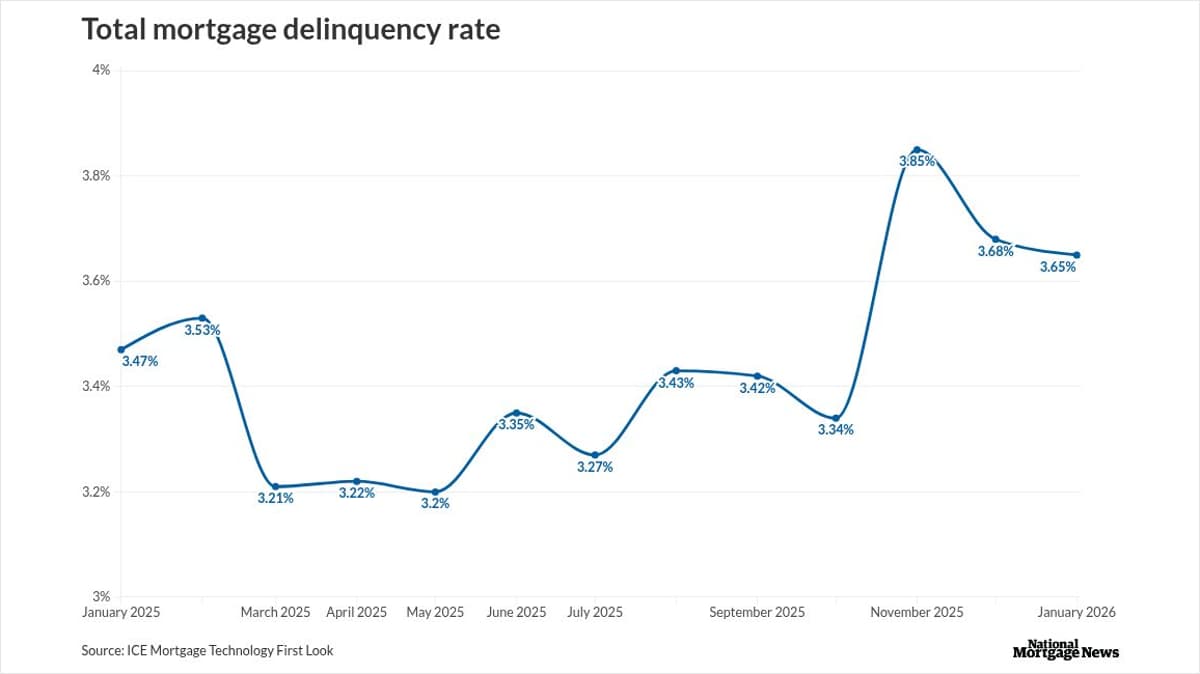

- •National delinquency rate fell to 3.65%, below pre‑pandemic.

- •Late‑stage delinquencies rose 104,000 year‑over‑year.

- •Louisiana and Mississippi lead delinquency rates above 8.5%.

- •Pre‑payment mortality dropped to 0.72% despite lower rates.

Pulse Analysis

The latest ICE First Look report paints a nuanced picture of the U.S. mortgage market. While early‑stage delinquencies have eased, pushing the aggregate delinquency rate below pre‑pandemic levels, the resurgence of foreclosure filings to early‑2020 volumes underscores lingering credit strain. Lenders are seeing a bifurcated borrower base: a majority maintaining payments, yet a growing subset slipping into severe arrears as interest‑rate pressures and cost‑of‑living challenges persist. This dynamic is reshaping risk models, prompting tighter underwriting and heightened monitoring of late‑stage delinquency pipelines.

Geographic disparities further complicate the outlook. The Gulf Coast states of Louisiana and Mississippi now top the delinquency rankings, each exceeding 8.5%, driven by higher unemployment and slower income growth. In contrast, the Mountain West and Pacific Northwest—Idaho, Montana, Washington—report rates near 2%, reflecting more resilient local economies and lower housing cost burdens. For investors, these regional patterns translate into differentiated exposure: mortgage‑backed securities tied to high‑risk states may experience higher loss‑given‑default rates, while assets backed by lower‑risk regions could retain stronger performance.

Looking ahead, the convergence of falling mortgage rates and declining pre‑payment speeds suggests borrowers are less inclined to refinance, limiting the natural amortization of high‑interest loans. VantageScore’s CreditGauge data corroborates the trend, showing a broad rise in early‑stage delinquencies across credit tiers. Continued macroeconomic pressures—sticky inflation, wage stagnation—could push more borrowers toward the 90‑day delinquency threshold, amplifying foreclosure risk. Stakeholders should monitor credit‑originations trends, especially the modest uptick in mortgage and auto loan volumes, as early indicators of shifting borrower behavior and potential policy interventions aimed at stabilizing the housing finance system.

Foreclosure starts surge to early 2020 levels

0

Comments

Want to join the conversation?

Loading comments...