Servicers Offer Support as Nonagency Gets More Competitive

•February 23, 2026

0

Why It Matters

The shift signals a strategic pivot for banks seeking yield outside agency channels, while heightened risk metrics demand robust servicing infrastructure.

Key Takeaways

- •Non‑agency originations have tripled recently.

- •Securitized non‑QM delinquencies now exceed 5%.

- •Credit enhancements average 26% for AAA tranches.

- •Sub‑servicers offer custom reporting for HELOC and data needs.

- •Traditional lenders weigh higher costs versus diversification benefits.

Pulse Analysis

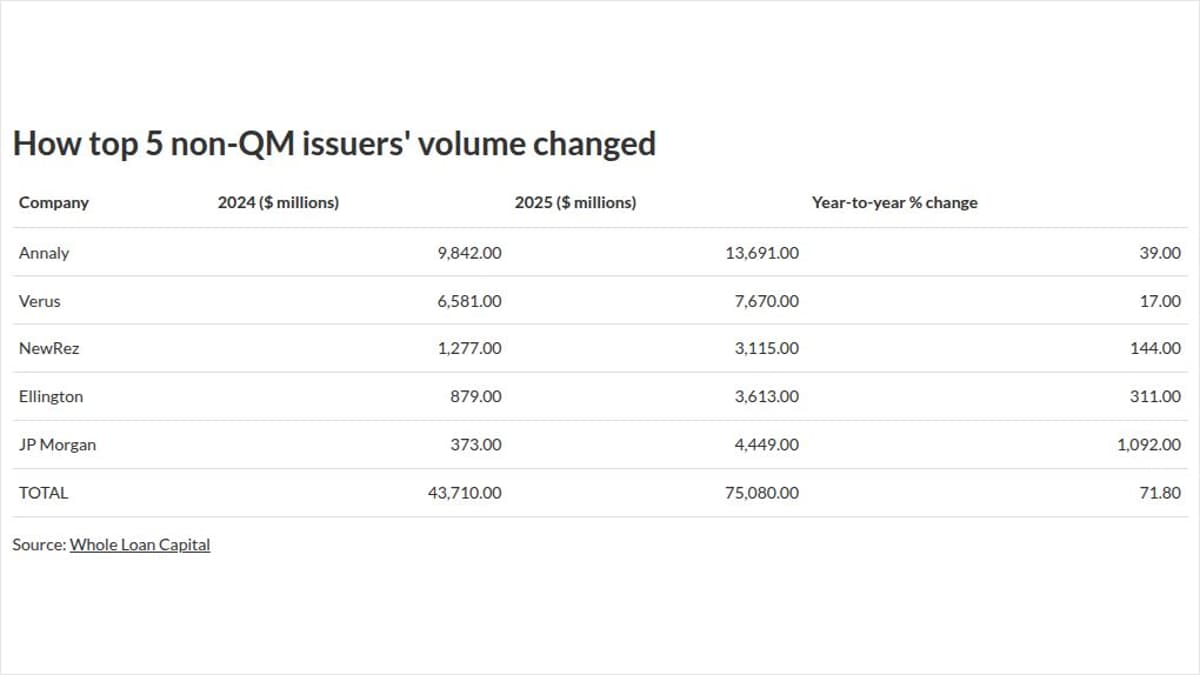

The non‑agency mortgage segment is rapidly shedding its niche status, becoming a mainstream source of volume for banks, insurers, and private securitizers. Originations have more than tripled, buoyed by demand for non‑owner‑occupied and non‑qualified‑mortgage (non‑QM) products that trade at attractive spreads. This surge has pushed securitization issuance up 78% in 2025, creating a competitive marketplace where investors chase higher yields while grappling with data‑intensive loan characteristics that traditional systems often cannot capture.

Performance trends add nuance to the growth narrative. Non‑QM delinquencies have edged above the 5% threshold, a level that, while modest compared with historical agency defaults, has prompted issuers to maintain robust credit‑enhancement cushions—averaging 26% for AAA‑rated tranches. Yet loss experience remains minimal, with Kroll Bond Rating Agency reporting sub‑5‑basis‑point losses on post‑crisis 2.0 deals. This paradox underscores a market still in a benign cycle, where credit‑enhancement levels may be more a legacy of post‑GFC caution than a reflection of current risk.

For traditional lenders, the decision to expand into non‑agency territory hinges on cost versus reward. Sub‑servicers now market bespoke reporting, HELOC draw capabilities, and custom data pipelines, reducing operational friction for newcomers. However, higher servicing fees, warehouse‑financing haircuts, and limited investor breadth compared with agency pipelines temper enthusiasm. Savvy banks will weigh these expenses against diversification benefits and the potential for higher margins on non‑owner‑occupied and cash‑out products, positioning sub‑servicing partnerships as a strategic lever rather than a mere cost center.

Servicers offer support as nonagency gets more competitive

0

Comments

Want to join the conversation?

Loading comments...