Which Markets Had the Highest Demand for Renovation Loans?

•March 3, 2026

0

Why It Matters

Lenders can tap untapped, high‑per‑capita demand in smaller regions, improving portfolio diversification and profitability. The trend signals broader economic shifts as equity‑rich homeowners prioritize aging‑in‑place upgrades.

Key Takeaways

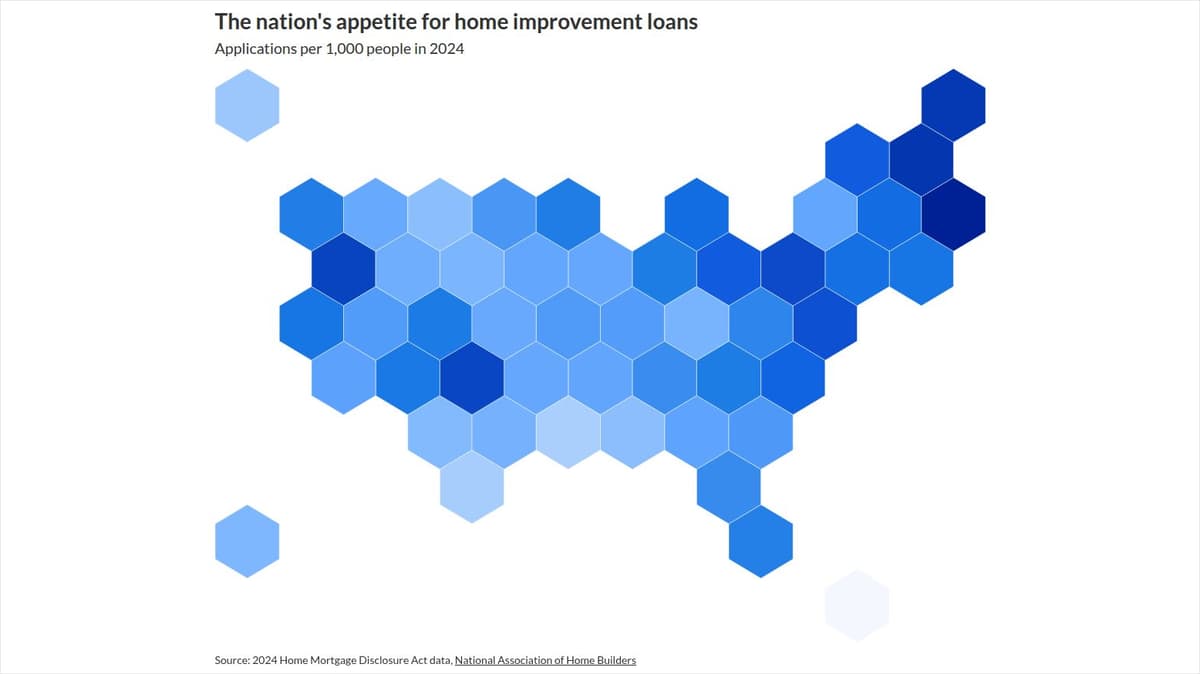

- •Rhode Island leads per‑capita renovation loan applications

- •Mountain and New England states show strong per‑capita demand

- •Top five counties have double national average loan rate

- •Home equity surge fuels homeowners' remodeling financing appetite

- •Large states dominate volume but lag per‑capita metrics

Pulse Analysis

The surge in renovation financing reflects deeper macro‑economic forces. An aging housing inventory combined with record‑high homeowner equity creates a compelling incentive for borrowers to invest in upgrades, especially for aging‑in‑place adaptations. Demographic trends, such as the growing senior population, amplify this need, turning home equity into a strategic source of low‑cost credit for remodeling projects.

Geographically, the data reveals a pronounced per‑capita concentration in smaller, often overlooked markets. States like Rhode Island and New Hampshire, and counties such as Rich County, Utah, exhibit demand rates that dwarf those of megacities. For lenders, this signals an opportunity to expand beyond traditional high‑volume states, tailoring products to local credit profiles and leveraging community banking relationships to capture niche demand.

Looking ahead, the renovation loan segment is poised for continued growth as equity levels remain elevated and regulatory environments stay supportive of consumer credit. Fintech platforms can accelerate access by streamlining underwriting for micro‑markets, while traditional banks may enhance risk models to account for regional price variations. Stakeholders that align product innovation with these demographic and geographic dynamics will likely secure a competitive edge in the evolving home‑improvement financing landscape.

Which markets had the highest demand for renovation loans?

0

Comments

Want to join the conversation?

Loading comments...