Real US Housing Wealth Contracts Ninth Month

Key Takeaways

- •Case-Shiller 20‑city index rose only 0.9% in February.

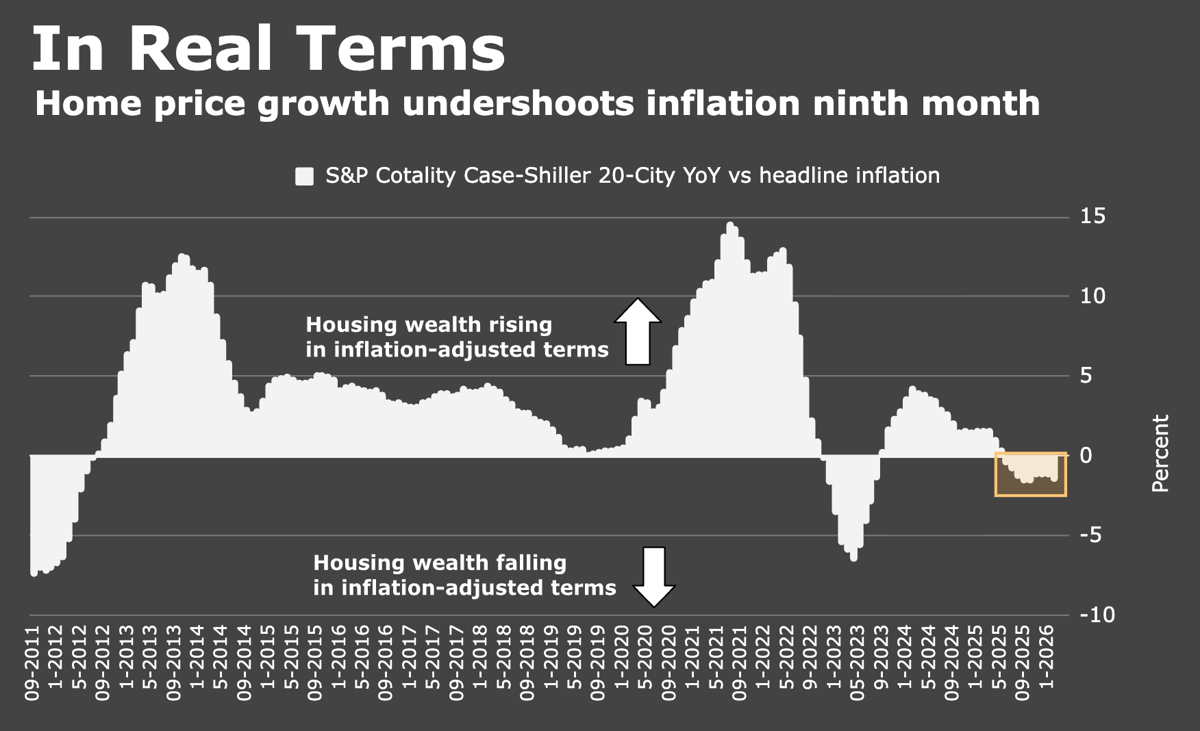

- •Real housing wealth has contracted for nine consecutive months.

- •Home price growth now negative in over half of major metros.

- •Financing costs exceed 6%, dampening buyer activity.

- •Chicago prices rose while Denver fell 2.5%, showing regional split.

Pulse Analysis

The latest Case‑Shiller data highlights a pivotal shift in the U.S. housing market. After years of robust gains, home price growth has slipped below 1% and, for the ninth month in a row, real housing wealth has contracted. This trend reflects a rare alignment where price appreciation fails to keep pace with headline inflation, suggesting that wages may eventually catch up, albeit slowly. For policymakers and investors, the prolonged under‑performance raises questions about the durability of the housing sector’s contribution to GDP growth.

Regional disparities are now the defining feature of the market. While Denver experienced a 2.5% year‑over‑year price decline, Chicago posted gains roughly twice that magnitude, illustrating how localized dynamics have eclipsed the once‑nationwide Sun Belt rally. High financing costs—mortgage rates hovering above 6%—compound the affordability challenge, discouraging prospective buyers and prompting a surge in price‑cut announcements and deal cancellations. Lenders and developers are therefore recalibrating risk models, focusing on markets where price resilience persists despite broader headwinds.

Looking ahead, the spring buying season is poised to test the market’s resilience. If mortgage rates remain elevated, the slowdown could deepen, pressuring homebuilders and real‑estate investment trusts. Conversely, any easing of financing costs or a modest rebound in wage growth could restore some balance, allowing price growth to outpace inflation again. Stakeholders—from mortgage lenders to institutional investors—must monitor both macro‑economic indicators and micro‑level price trends to navigate an increasingly fragmented housing landscape.

Real US Housing Wealth Contracts Ninth Month

Comments

Want to join the conversation?