Affordability Posts Mild Gains in Second Half of 2025 but Crisis Continues

•March 5, 2026

0

Why It Matters

The data signals a slight relief but underscores a persistent affordability crisis that shapes home‑buyer demand, construction pipelines, and policy priorities nationwide.

Key Takeaways

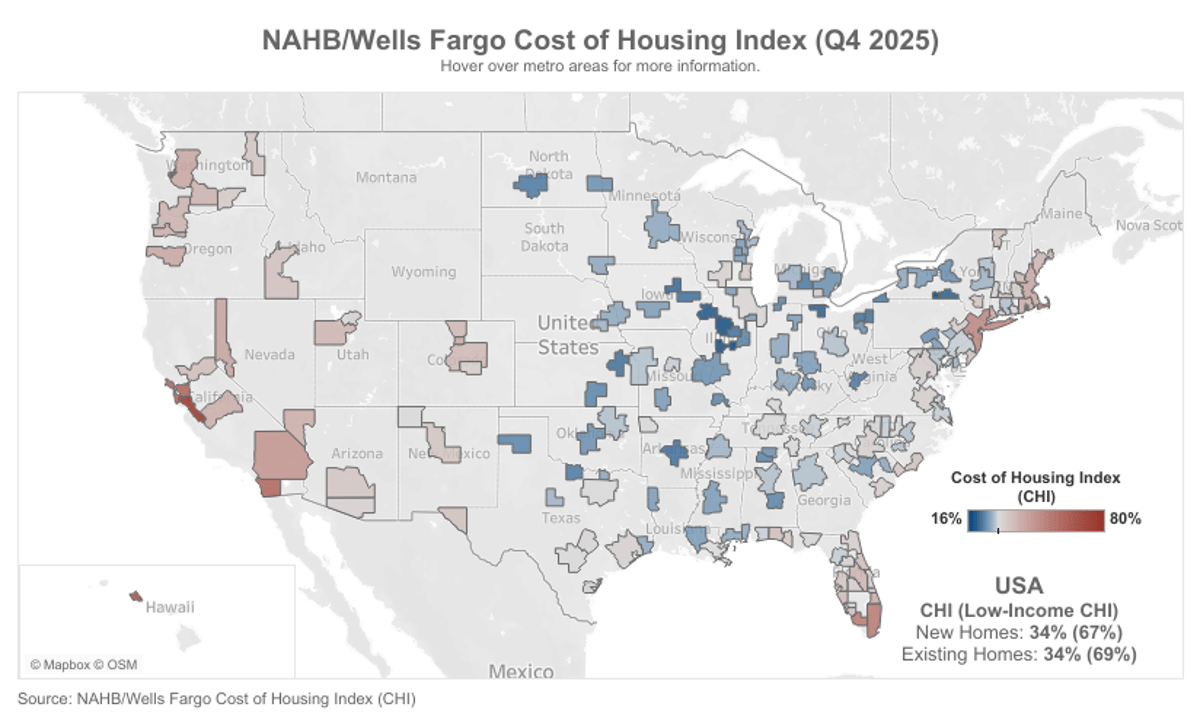

- •Median new home costs 34% of median income.

- •Low‑income families need 67% of earnings for new home.

- •Mortgage rates fell to 6.32% in Q4 2025.

- •San Jose area requires 80% of income for mortgage.

- •Illinois markets need only 16‑18% of income.

Pulse Analysis

The latest Cost of Housing Index highlights how modest price declines and a dip in mortgage rates have nudged affordability metrics northward, yet the overall picture remains bleak. A median new home still consumes roughly a third of a typical family's earnings, and for low‑income households the burden exceeds two‑thirds. This reflects broader macro trends: wage growth has lagged behind housing cost inflation, while the Federal Reserve’s rate cuts have only partially offset financing costs.

Geographic disparity is stark. Coastal tech hubs like San Jose‑Sunnyvale‑Santa Clara demand 80 % of a family's income, pushing many families into severe cost‑burdened territory. Conversely, Mid‑western markets such as Decatur and Springfield sit at the opposite extreme, with mortgage costs under 18 % of income. These gaps influence migration patterns, with price‑sensitive buyers gravitating toward affordable regions, reshaping local labor pools and real‑estate development strategies.

Looking ahead, the modest affordability gains are unlikely to reverse the crisis without targeted interventions. Builders may focus on multifamily and smaller‑footprint homes to lower entry costs, while policymakers could consider expanding affordable‑housing subsidies or adjusting zoning to increase supply. Investors will monitor the CHI closely, as sustained affordability pressure could dampen demand for higher‑priced assets, while affordable markets may present growth opportunities.

Affordability Posts Mild Gains in Second Half of 2025 but Crisis Continues

0

Comments

Want to join the conversation?

Loading comments...