Gains for Student Housing Construction in the Last Quarter of 2025

•February 27, 2026

0

Why It Matters

The rebound signals renewed builder confidence but underscores that future sector growth hinges on a demographically constrained enrollment outlook, affecting investors and campus planners alike.

Key Takeaways

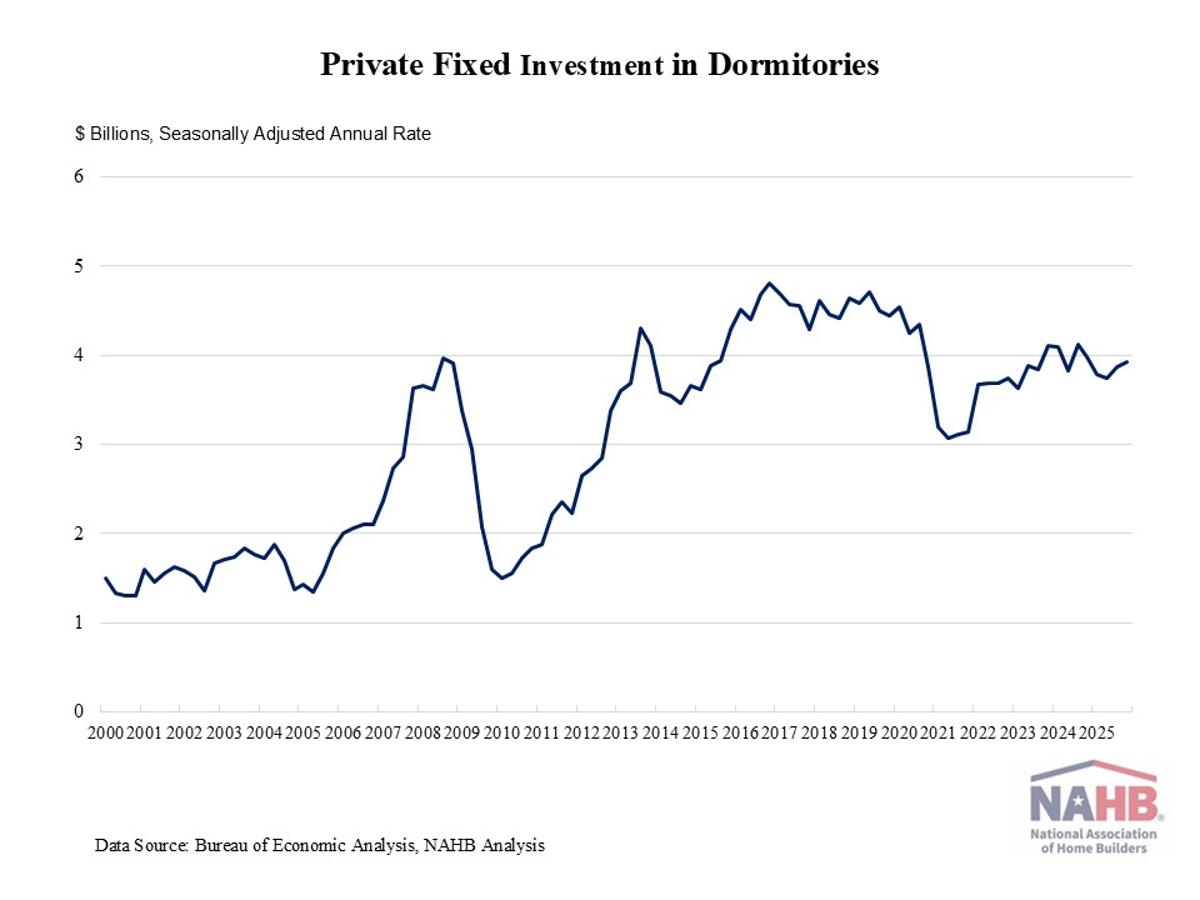

- •Q4 2025 dorm investment rose 1.5% to $3.9 B.

- •Investment remains 1.3% below 2024 levels.

- •Pandemic cut dorm spending from $4.4 B to $3 B.

- •Enrollment projected to grow only 9% through 2031.

- •Slower demographic growth caps long‑term housing demand.

Pulse Analysis

The modest uptick in private fixed investment for student housing during the last quarter of 2025 reflects a broader stabilization after the pandemic shock. After a steep fall to a $3 billion SAAR in 2021, developers have gradually rebuilt pipelines as campuses reopened and in‑person instruction resumed. Yet, the sector still trails its pre‑pandemic peak of $4.4 billion, indicating that higher borrowing costs and lingering uncertainty continue to temper capital deployment.

Underlying this investment pattern is a shifting enrollment landscape. While post‑pandemic enrollment has recovered from the 3‑plus percent declines of 2020‑21, the National Center for Education Statistics projects only a 9% increase in total postsecondary enrollment between 2021 and 2031. This slowdown stems from lower birth rates after the Great Recession, curbing the traditional pipeline of college‑age students. Consequently, the demand for new dormitory capacity is expected to grow at a more measured pace, prompting developers to prioritize renovation, mixed‑use projects, and higher‑density models over large, stand‑alone constructions.

For investors and university operators, the key takeaway is risk‑adjusted opportunity. Short‑term construction activity may benefit from the current enrollment rebound, but long‑term returns will depend on strategic asset positioning—such as integrating affordable housing, leveraging public‑private partnerships, and adopting flexible lease structures. Policymakers can also influence outcomes by supporting financing mechanisms that mitigate interest‑rate pressures, ensuring the student‑housing market remains a viable component of higher‑education infrastructure.

Gains for Student Housing Construction in the Last Quarter of 2025

0

Comments

Want to join the conversation?

Loading comments...