Home Building Shows Signs of Stabilization with Monthly Gain in Starts

Companies Mentioned

Why It Matters

The rise signals renewed builder confidence, yet the drop in permits and under‑construction inventory suggests an uneven recovery that could temper housing supply and influence price dynamics across the market.

Key Takeaways

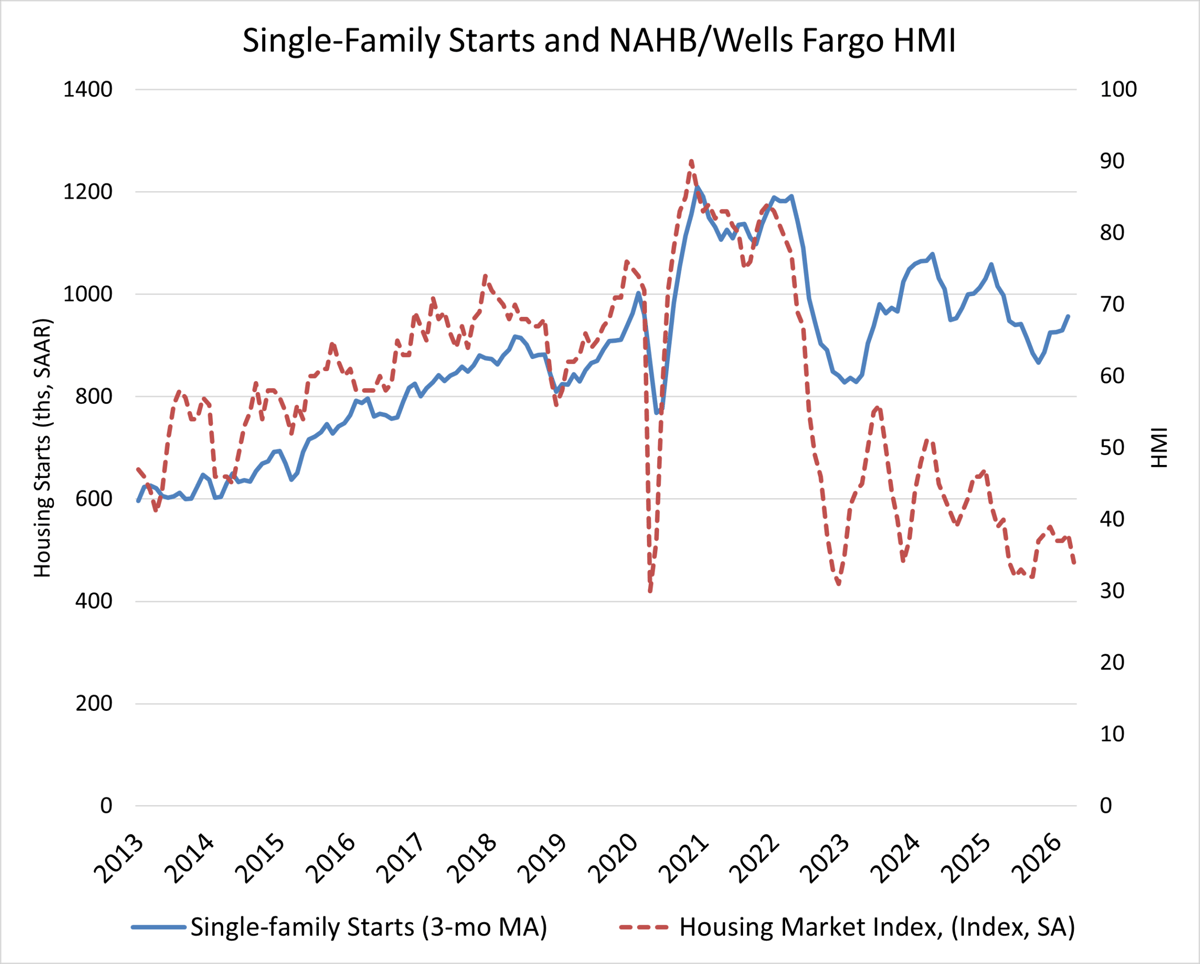

- •March housing starts rose 10.8% to 1.5 million units.

- •Single‑family starts up 9.7%; multifamily up 13.3% year‑over‑year.

- •Units under construction down 9.8% YoY, highlighting inventory lag.

- •Permits fell 10.8%, signaling continued builder caution.

- •Northeast leads regional growth; West lags with 15.5% decline.

Pulse Analysis

Housing starts are a bellwether for the broader economy because they reflect builder sentiment, labor demand, and future home‑buyer activity. March’s 10.8% jump to a 1.5 million‑unit annualized rate marks the first monthly gain since late 2023, suggesting that lower mortgage rates earlier in the year may have temporarily eased financing constraints. However, the underlying softness in permits—down 10.8%—indicates that many developers remain wary of lingering affordability challenges, especially as construction costs stay elevated.

Regional disparities add nuance to the headline numbers. The Northeast posted a 36% year‑to‑date increase in starts, buoyed by strong demand for both single‑family and multifamily units, while the West experienced a 15.5% decline, reflecting tighter credit conditions and slower population inflows. These gaps affect local labor markets, material supply chains, and pricing pressure; areas with robust starts often see tighter inventory, pushing home prices upward, whereas lagging regions may face excess supply and slower price appreciation.

Looking ahead, the trajectory of permits will be the critical gauge of sustained momentum. If the Federal Reserve’s policy stance keeps rates elevated, builders may scale back new projects, reinforcing the current inventory shortfall. Conversely, any easing of financing costs could reignite permit activity, translating the March start surge into a more durable recovery. Stakeholders—from lenders to material suppliers—should monitor permit trends and regional start differentials to anticipate shifts in construction demand and related market dynamics.

Home Building Shows Signs of Stabilization with Monthly Gain in Starts

Comments

Want to join the conversation?

Loading comments...