Mortgage Applications Retreat in May, with ARMs Gaining Share

Why It Matters

The decline signals that higher rates are throttling refinance demand, but the modest rise in purchase activity and ARM interest suggest borrowers are seeking cost‑effective alternatives, shaping lenders’ product strategies. Understanding these shifts helps banks and investors gauge future mortgage‑backed securities performance and pricing risk.

Key Takeaways

- •Mortgage applications fell 5.5% month‑over‑month in May.

- •Refinance applications dropped 12.3%, purchase apps rose 1.8%.

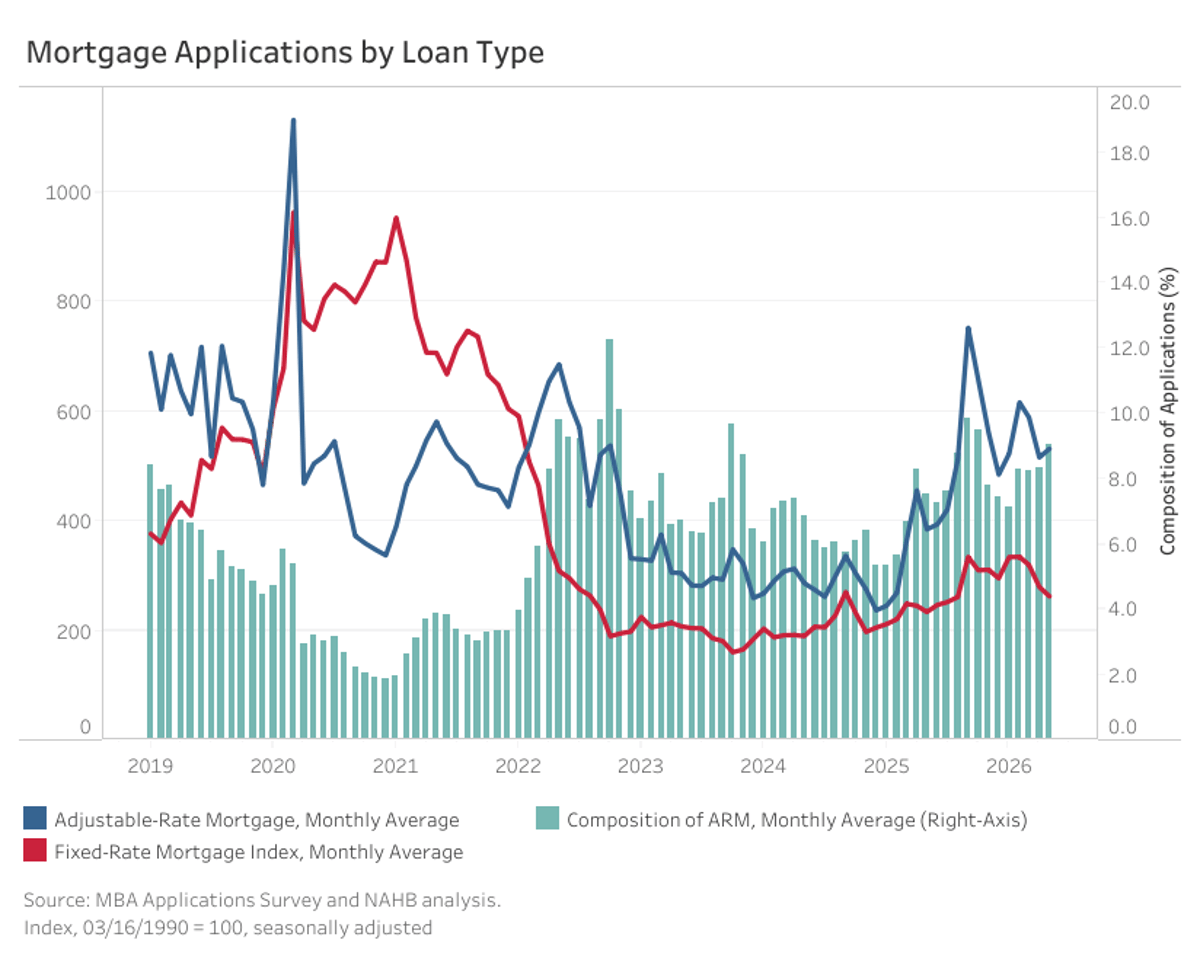

- •ARM share rose to 9.0%, up 0.7 points month‑over‑month.

- •Average loan size increased 2.5% to $407,600.

- •30‑yr fixed rate hit 6.54% in May.

Pulse Analysis

Higher borrowing costs continue to reshape the U.S. mortgage landscape. In May, the Mortgage Bankers Association’s Market Composite Index recorded a 5.5% month‑over‑month dip in total applications, largely reflecting a sharp 12.3% contraction in refinance filings as homeowners balk at rates that have risen to 6.54% for a 30‑year fixed loan. Purchase demand proved more resilient, posting a modest 1.8% gain, which kept year‑over‑year activity 14.2% above the 2025 baseline. Lenders are therefore navigating a market where rate‑sensitive refinance pipelines are drying up while new‑home financing remains cautiously optimistic.

Adjustable‑rate mortgages are emerging as a strategic alternative amid the rate environment. ARM applications rose 3.1% in May, lifting their share of total applications to 9.0%, the highest level in over two years. The appeal lies in lower introductory rates—5.7% for a 5/1 ARM in April—offering borrowers immediate payment relief compared with fixed‑rate offers. This shift hints at a broader recalibration of borrower risk tolerance, as consumers weigh short‑term affordability against long‑term rate certainty. Lenders responding with competitive ARM products could capture a growing niche, especially if Treasury yields remain elevated.

Loan size dynamics add another layer to the outlook. The average loan balance climbed 2.5% to $407,600, driven by larger purchase loans that rose 2.2% to $465,000, while refinance loan sizes slipped 1.5% to $321,000. The divergence underscores a market where new‑home buyers are willing to finance higher‑priced properties, whereas existing homeowners are scaling back refinancing ambitions. For investors in mortgage‑backed securities, these trends suggest a potential tilt toward higher‑principal, fixed‑rate assets with longer maturities, while the growing ARM share may introduce more variable‑rate exposure. Monitoring rate trajectories and borrower behavior will be critical for forecasting credit risk and pricing in the months ahead.

Mortgage Applications Retreat in May, with ARMs Gaining Share

Comments

Want to join the conversation?

Loading comments...