Single-Family AD&C Lending Edges Higher in Q1

Why It Matters

The modest rise signals lingering demand for single‑family building despite tighter credit, while the growing share of delinquent loans highlights rising credit risk for lenders and investors in the housing sector.

Key Takeaways

- •Single‑family AD&C loans rose 0.8% QoQ in Q1 2026.

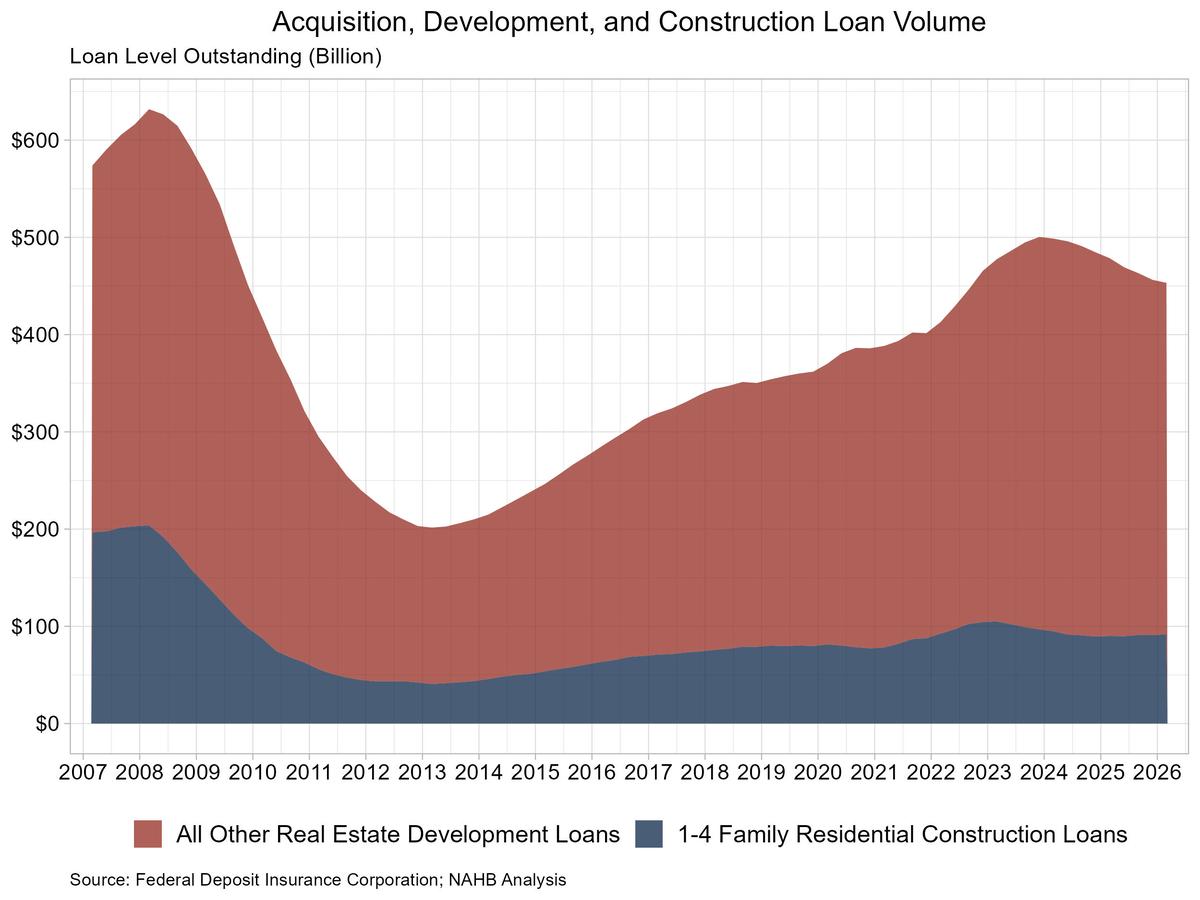

- •Total AD&C loan stock fell to $453.3 bn, down 0.6% QoQ.

- •1‑4 family residential loans up 1.9% YoY, third straight rise.

- •Past‑due and non‑accrual construction loans equal 1.1% of portfolio.

- •Outstanding residential construction debt 56% below 2008 peak.

Pulse Analysis

The Federal Deposit Insurance Corporation’s latest loan‑level data shows a nuanced picture for the construction finance market. While the overall AD&C loan balance contracted to $453.3 billion, single‑family construction lending nudged higher, reflecting builders’ continued appetite for new homes amid a modest easing of credit conditions. This incremental growth contrasts with a broader nine‑quarter decline in total AD&C exposure, underscoring the sector’s long‑term contraction since the post‑2008 credit crunch.

Builders are navigating a tighter financing environment, as highlighted by the NAHB AD&C Financing Survey, which notes a slight tightening of credit terms. To bridge the gap, many developers have turned to equity partners and alternative capital sources, diluting reliance on traditional bank loans. Yet, the rise in past‑due and non‑accrual construction loans—now 1.1% of the residential construction portfolio—signals that lenders are encountering higher stress levels, potentially prompting stricter underwriting standards and higher risk premiums.

Looking ahead, the lingering gap between current loan volumes and the 2008 peak suggests ample room for growth if macroeconomic conditions improve. Policymakers and regulators will watch the delinquency trends closely, as a sustained increase could pressure banks’ balance sheets and influence monetary policy decisions. For investors, the mixed signals—steady loan growth against a backdrop of elevated credit risk—call for careful assessment of exposure to construction‑related securities and mortgage‑backed instruments.

Single-Family AD&C Lending Edges Higher in Q1

Comments

Want to join the conversation?

Loading comments...