The Skip-Month Mystery: What Last Month’s Returns Are Really Telling You

Key Takeaways

- •Prior month returns boost momentum when they are above average

- •High prior-month volatility suppresses momentum performance across strategies

- •12‑1 outperforms in stable, low‑volatility uptrends

- •12‑0 delivers steadier returns during turbulent market conditions

- •Adaptive skip‑month use improves risk‑adjusted outcomes

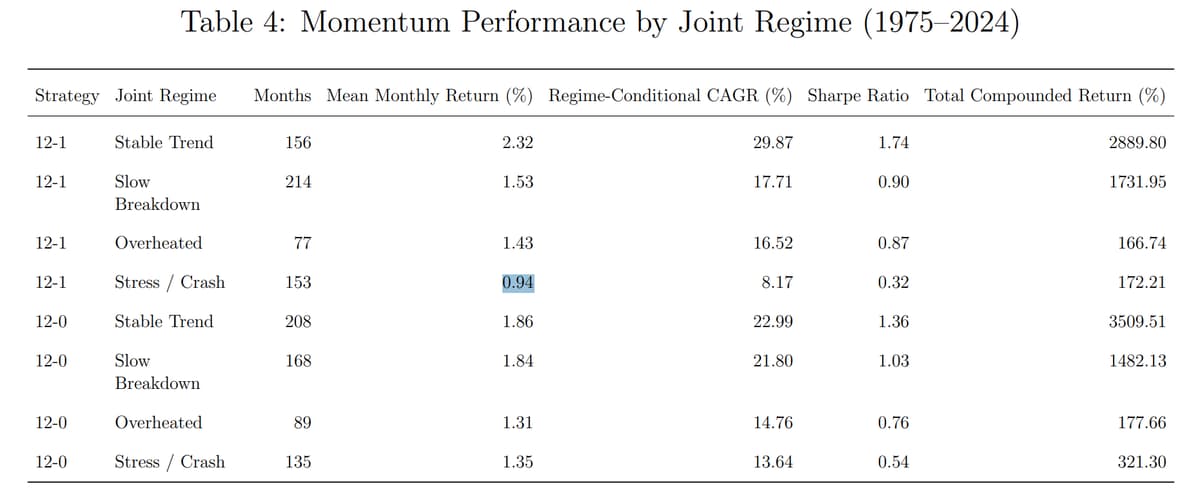

Pulse Analysis

Momentum investing has long relied on a simple heuristic: ignore the most recent month’s return to avoid short‑term reversals. Originating in the early 1990s, the “skip‑month” convention became a default filter for both academic models and practitioner tools. However, the rule was never rigorously tested against changing market dynamics. The recent Alpha Architect paper revisits this assumption with a half‑century data set, contrasting two industry‑level momentum constructions—12‑1 (skip) and 12‑0 (include). By doing so, it opens a fresh dialogue about whether habit or evidence should drive strategy design.

The analysis uncovers two powerful signals hidden in the last month: return magnitude and volatility level. When the prior month posts above‑average gains and low volatility, the 12‑1 strategy spikes to roughly 2.3% monthly, confirming that momentum thrives in stable uptrends. Conversely, a volatile prior month drags the same strategy down to about 1.1%, while the 12‑0 version holds steadier at 1.3‑1.4%. This regime‑sensitivity demonstrates that the skip‑month rule amplifies upside in favorable conditions but also magnifies downside when markets are turbulent. By integrating the most recent month, the 12‑0 approach smooths performance, delivering a narrower return band across four identified market states.

For investors, the practical takeaway is clear: the skip‑month rule should be treated as a conditional lever, not a blanket setting. Portfolio managers can monitor the latest month’s return‑volatility profile and dynamically toggle between 12‑1 and 12‑0 constructions, aligning exposure with their risk appetite. Such adaptive frameworks promise higher Sharpe ratios and lower drawdowns without adding complexity. Moreover, the study hints at broader applications—any factor‑based strategy that discards recent data may benefit from a nuanced, regime‑aware reassessment as markets evolve.

The Skip-Month Mystery: What Last Month’s Returns Are Really Telling You

Comments

Want to join the conversation?