Diesel Supply, Pricing Prospects Outshine Those of Urea: Whitelaw

Why It Matters

Rising fuel and fertilizer costs erode farm profit margins, and any relief in diesel pricing could improve cash flow, but persistent urea scarcity threatens crop yields and profitability.

Key Takeaways

- •Diesel prices doubled to about $3.20 AUD/L (~$2.12 USD) since Feb.

- •Urea spot price now near $1,500 AUD/t (~$990 USD).

- •Iran‑US cease‑fire may ease diesel imports but urea supply stays tight.

- •Australian diesel imports rose 22% YoY in Q1 2026.

- •Growers urged to secure written fertilizer contracts amid price volatility.

Pulse Analysis

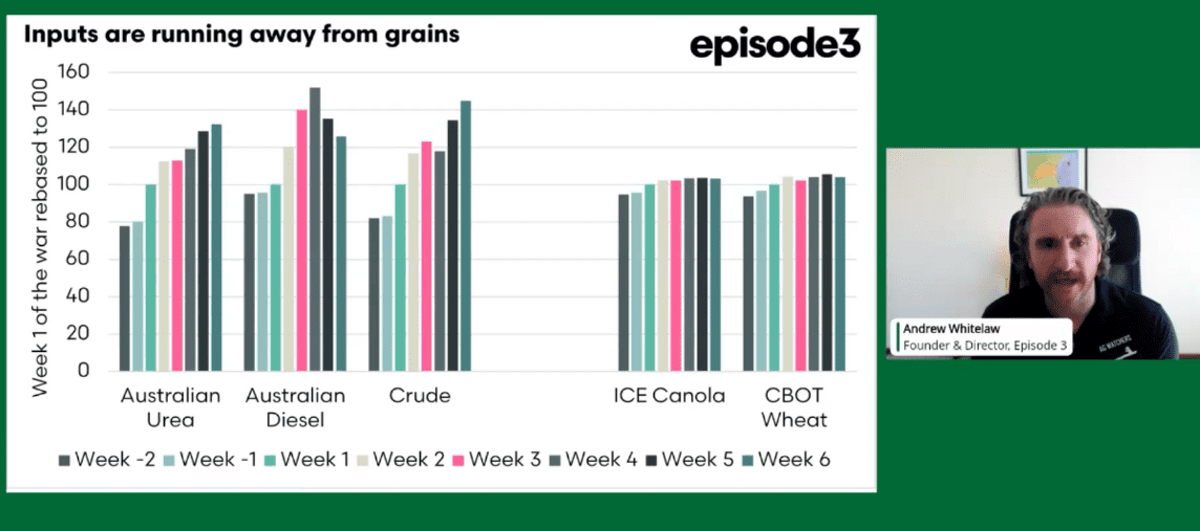

The recent Iran‑U.S. cease‑fire has immediate macro‑economic implications for commodity markets. While crude oil futures fell roughly 20% within hours, the ripple effect on downstream products is uneven. Australian diesel, already at record highs of $3.20 AUD per litre, benefits from a narrowing spread with crude, yet the market remains volatile due to the country’s reliance on a dwindling refinery base. In contrast, urea—a critical nitrogen fertilizer—has not seen price relief; landed costs hover near $1,500 AUD per tonne, outpacing even the early‑war spikes seen during the Ukraine conflict. This divergence creates a classic input‑output mismatch for grain growers, who face flat grain prices despite soaring production costs.

Australia’s diesel supply chain shows signs of adaptation. Q1 2026 diesel imports jumped 22% year‑over‑year, driven by increased shipments from traditional Asian sources and atypical carriers from the United States and the United Kingdom. The influx of vessels, many arriving from the reopened Hormuz corridor, has helped temper the previously record‑wide diesel‑to‑crude spread, which had ballooned beyond $2 per litre. Nevertheless, analysts caution that any sustained price moderation depends on continued geopolitical stability and the ability of Australian refineries to resume operations without further shutdowns.

For the farming sector, the stakes are high. With the peak top‑dressing window looming in June, a shortfall in urea imports could force growers to delay or reduce fertilizer applications, directly impacting yields. Whitelaw’s recommendation to secure written contracts reflects a broader industry shift toward risk mitigation amid price spikes. As input costs remain elevated while commodity prices stay stagnant, farm profitability hinges on supply chain certainty and the ability to pass higher costs onto buyers, a challenge that will shape Australian agriculture throughout 2026.

Diesel supply, pricing prospects outshine those of urea: Whitelaw

Comments

Want to join the conversation?

Loading comments...