Maritime Vessel Uptake of Alt Fuels Proceeds ... Slowly

•March 2, 2026

0

Companies Mentioned

Why It Matters

The slowdown signals a measured pace in the maritime fuel transition, while continued LNG demand confirms its role as the near‑term bridge to deeper decarbonisation.

Key Takeaways

- •February 2026: 17 alternative‑fuel vessel orders.

- •LNG dominates with 14 container ship orders.

- •Dual‑fuel ethane carriers account for three orders.

- •First‑two‑months orders fell 31% YoY.

- •LNG bunkering orders signal infrastructure growth.

Pulse Analysis

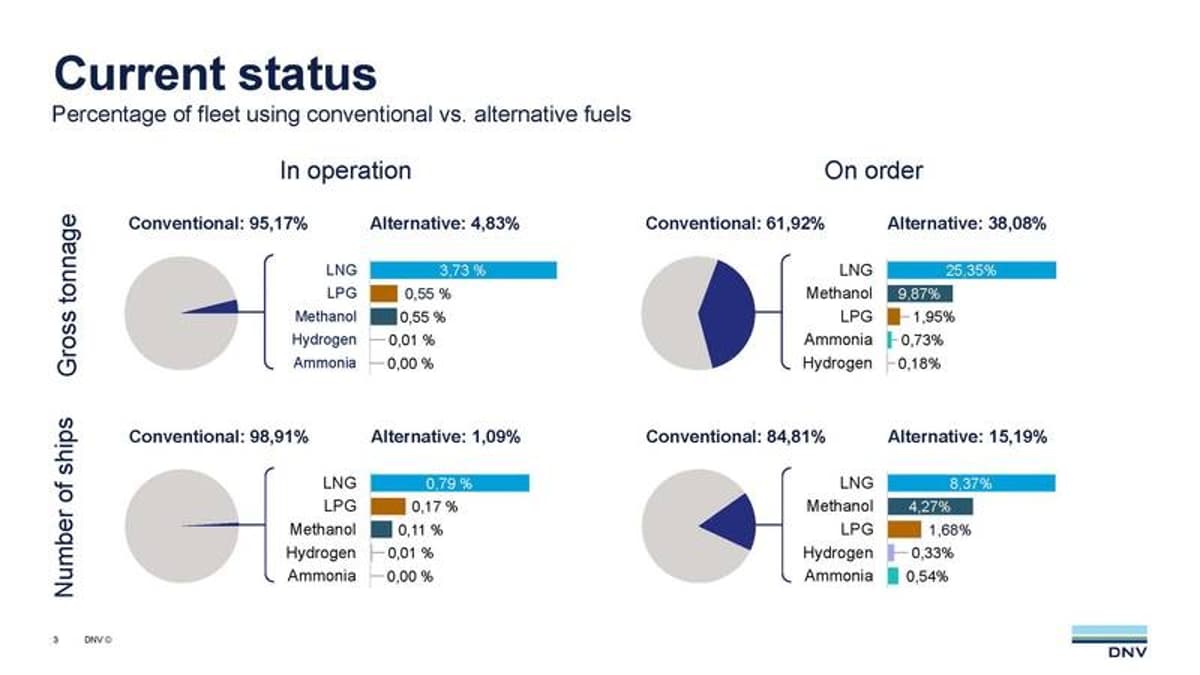

The maritime sector’s shift toward lower‑emission fuels remains a cornerstone of global decarbonisation strategies, yet the latest DNV data reveal a modest dip in ordering activity. February 2026 saw only 17 new alternative‑fuel vessels, a 31% decline compared with the same window in 2025. This slowdown reflects broader market dynamics, including tighter capital allocation and lingering uncertainties around long‑term fuel pricing. Nonetheless, the cumulative 37 orders in the first two months still represent a tangible commitment to cleaner propulsion, indicating that the transition, while slower, is ongoing.

LNG continues to dominate the orderbook, driven largely by container operators responding to cargo‑owner mandates for reduced emissions. Fourteen of the new vessels are LNG‑powered container ships, reinforcing LNG’s status as the pragmatic bridge fuel for high‑volume trade routes. Parallel growth in LNG bunkering vessels highlights the critical need for supporting infrastructure; without a reliable supply chain, even the most advanced fuel conversions would falter. Industry stakeholders are therefore investing heavily in bunkering terminals and retrofitting projects to ensure seamless fuel availability across key ports.

Looking ahead, the modest presence of dual‑fuel ethane carriers hints at diversification beyond LNG, as shipowners explore flexible fuel options to hedge against market volatility. Policy incentives, such as the IMO’s carbon intensity targets, will likely accelerate investment in alternative fuels, but the pace will depend on clear regulatory frameworks and cost‑effective technology roll‑outs. In the near term, LNG is poised to retain its lead, while emerging fuels like methanol, ammonia, and hydrogen will gradually carve out niche markets as the sector matures.

Maritime Vessel Uptake of Alt Fuels Proceeds ... Slowly

0

Comments

Want to join the conversation?

Loading comments...