Supply-Chain Stress That Peaked in Covid Heads Higher Again

Companies Mentioned

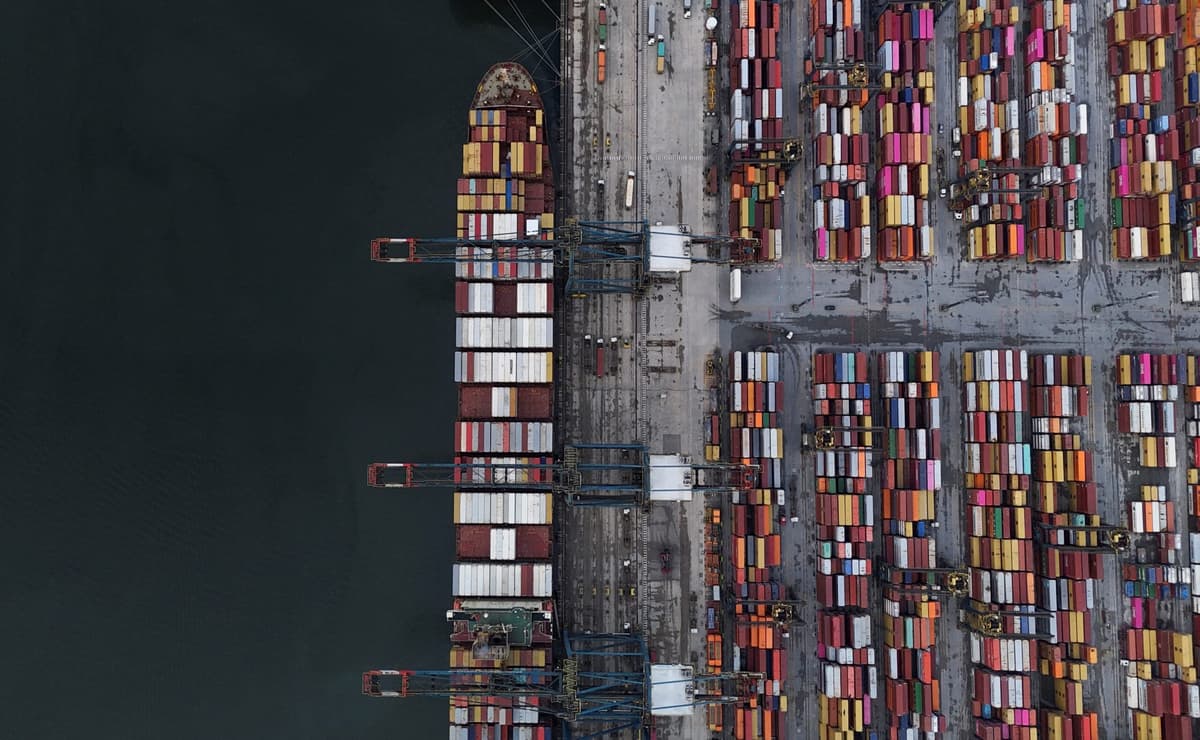

Why It Matters

Elevated logistics pressures threaten to reignite inflation and could force central banks to tighten policy, while higher freight rates squeeze manufacturers and consumers worldwide.

Key Takeaways

- •Global supply‑chain pressure index hits four‑year high in April

- •Maersk expects $500 million extra monthly costs through Q2 2024

- •Red Sea detours add fuel use, lengthen container transit times

- •US Logistics Managers’ Index shows transport costs near 2018 record

- •German manufacturers cite material shortages, but demand remains primary constraint

Pulse Analysis

The resurgence of supply‑chain stress is rooted in two intertwined forces: soaring energy prices and geopolitical disruption in the Red Sea. As carriers reroute vessels around southern Africa to avoid conflict, transit times lengthen and fuel consumption spikes, feeding into the World Bank’s Global Supply Chain Stress Index, which now skirts the pandemic peak. This logistical drag reverberates through freight markets, inflating shipping rates and eroding margins for import‑dependent firms, while also nudging broader price pressures higher.

Container giant A.P. Moller‑Maersk illustrates the cost cascade. The Copenhagen‑based line projects an additional $500 million in monthly expenses through the second quarter, prompting a dual strategy of passing costs to shippers and throttling vessel speeds to conserve fuel. Such measures underscore a delicate balancing act: higher freight charges risk dampening demand for global trade, yet insufficient price adjustments could erode carrier profitability. Analysts warn that persistent energy‑driven freight inflation could feed into consumer prices, prompting central banks to stay vigilant.

On the demand side, U.S. logistics surveys reveal transport costs at their highest since 2018 and warehousing capacity tightening at a rapid pace. Coupled with modest wage growth and rising consumer‑price inputs, these dynamics heighten the risk of a secondary inflationary bout. European manufacturers, especially in Germany, report material shortages, though demand constraints remain dominant. Policymakers therefore face a complex trade‑off: supporting supply‑chain resilience without stoking inflation, a challenge that will shape monetary and trade policy throughout 2024.

Supply-Chain Stress That Peaked in Covid Heads Higher Again

Comments

Want to join the conversation?

Loading comments...