Global Equity Briefing

Creator covering listed financials and digital banks (e.g., Nubank), including retail banking product sets and economics.

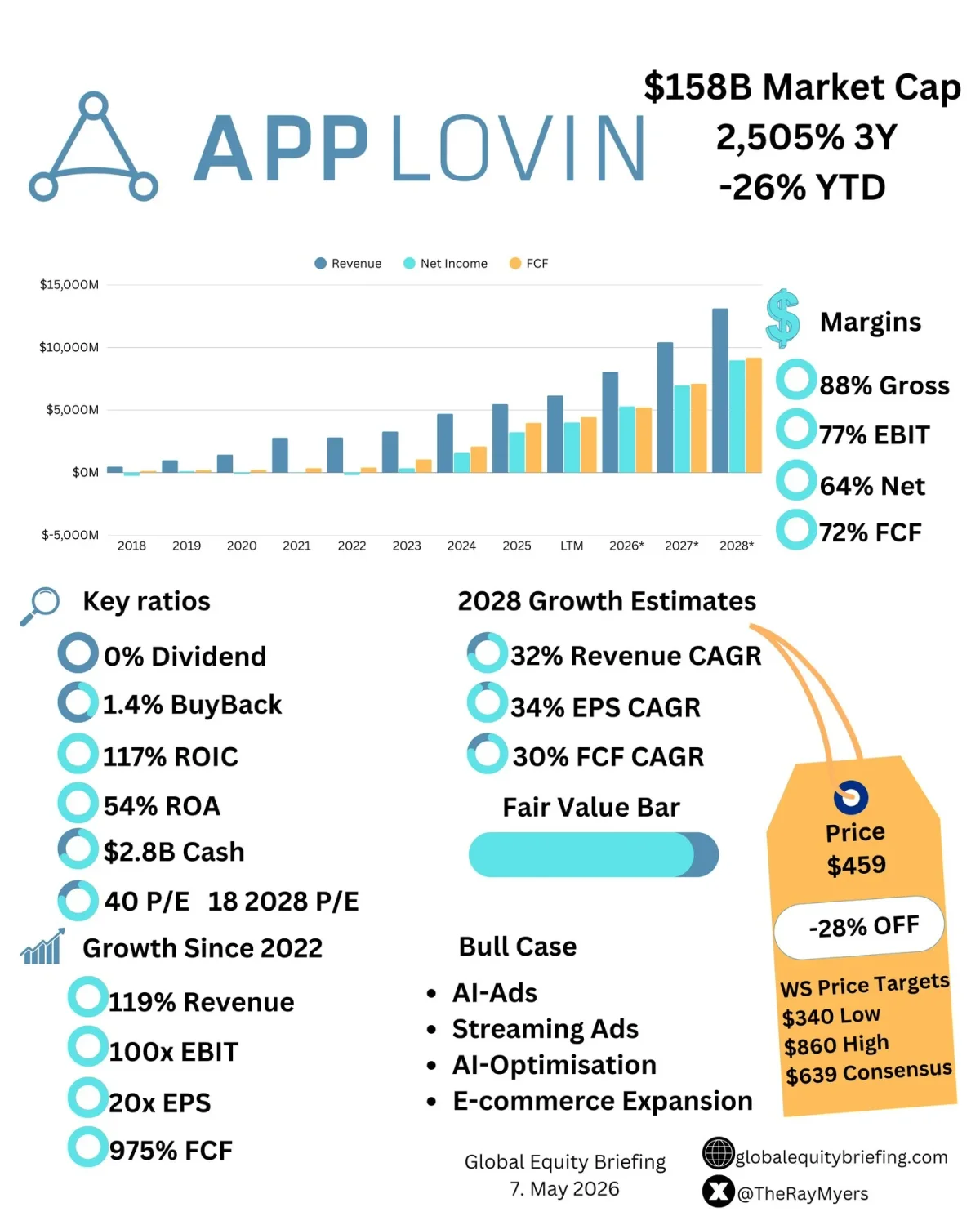

Strong Fundamentals, yet $APP Down 26% YTD

How is $APP down 26% YTD? - 77% EBIT Margin - 117% ROIC - 34% 2028 EPS CAGR - Reasonable Valuation - 28% Below Consensus Price Target

SoFi's Upside Could Range From 35% To

$SOFI Street Targets: Low: $16 Consensus: $22, 35% Upside High: $38, 138% Upside Who is right?

Sofi's Strong Earnings, 16% Drop Reveal Massive Undervaluation

$SOFI just reported a stellar earnings report, yet the market went mad, and the stock fell 16%. So I created a new 2030 Valuation Model. 👇 In this report, I expand on why I have made Sofi one of my largest holdings...

Meridian Q1 2026 Delivers 26

$MRDN Q1 2026! Small cap trading 4x EV/ADJ EBITDA whilst growing topline at 17% and ADJ EBITDA at 26% - Rebranding to Meridian is completed. - Best revenue growth in 4 quarters. - Strong ADJ EBITDA growth of 26%. - Net leverage ratio down...

Meta Earnings Prompt Widespread Price Target Cuts

Analyst Price Targets after $META Earnings: TD Cowen $820 ➡️ $800 J.P. Morgan $825 ➡️ $725 BMO Capital $730 ➡️ $720 Barclays $800 ➡️ $830 Bank of America $820 ➡️ $835 Piper Sandler $880 ➡️ $800 Truist Financial $900 ➡️ $840 KeyBanc $760 RBC Capital $810 Cantor Fitzgerald $750 Oppenheimer $622.25 Citi...

Roth MKM Sticks to $108 ASTS Target, 40% Upside

Despite recent challenges, Roth MKM Reiterated its $108 Price Target for $ASTS 40% Upside. Are they right?

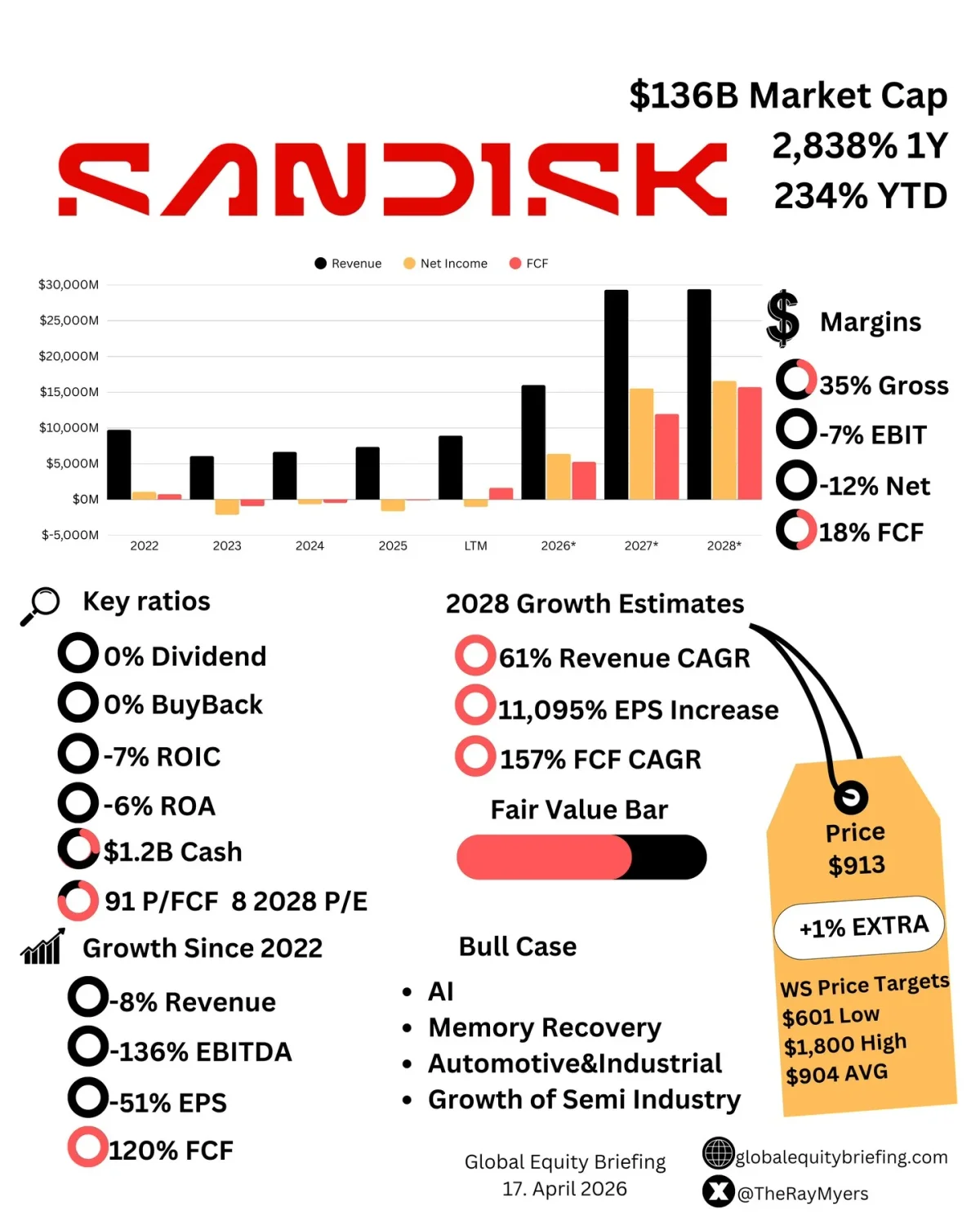

AI Could Transform SNDK Into High‑Growth Memory Leader

Is $SNDK a cyclical memory stock, or will AI make memory a stable grower? $SNDK +2,838% 1Y 🚀 +234% YTD 🟢 - Weak Margins - Weak Growth since 2022 - INSANE Outlook from AI - 157% 2028 FCF CAGR - Reasonable Valuation - 1% Above Consensus Price...

Tech Stocks Cheap, S&P 7300 Target Signals Safe Haven

"In 5 years, you won't believe Tech stocks could be bought so cheaply ". Tom Lee Lee says the market is better positioned now than in November 2025 because it has now demonstrated it can handle surging oil prices and War. Furthermore,...

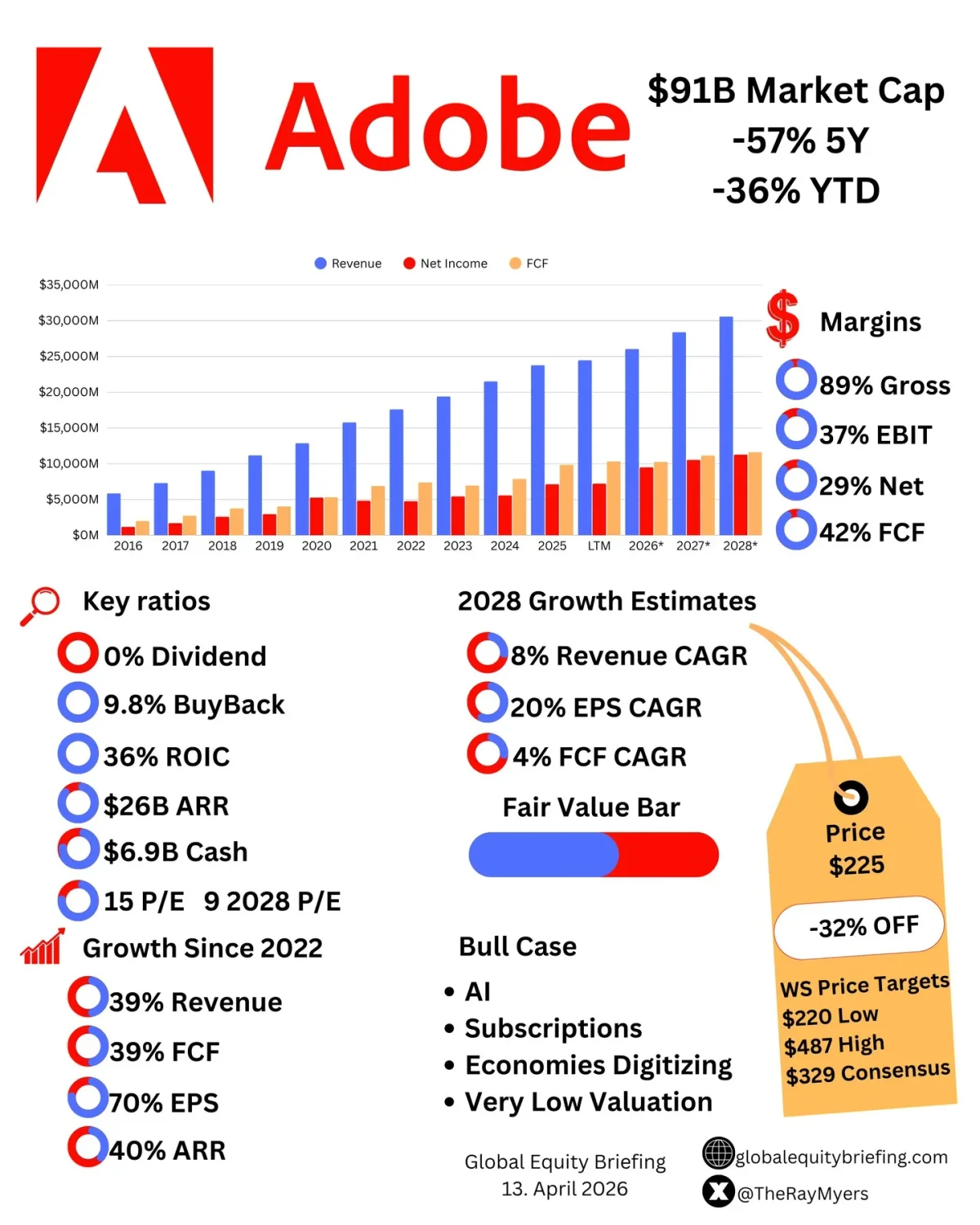

Adobe's Stock Slump Masks Strong Fundamentals and Value

Is $ADBE a falling knife, as AI is disrupting them? Or a misunderstood opportunity? $ADBE -57% 5Y 🔴 -36% YTD 🔴 - Really Strong Margins - Incredible 9.8% BuyBack - $26B ARR - Cheap Valuation - 32% Below Consensus Price Target

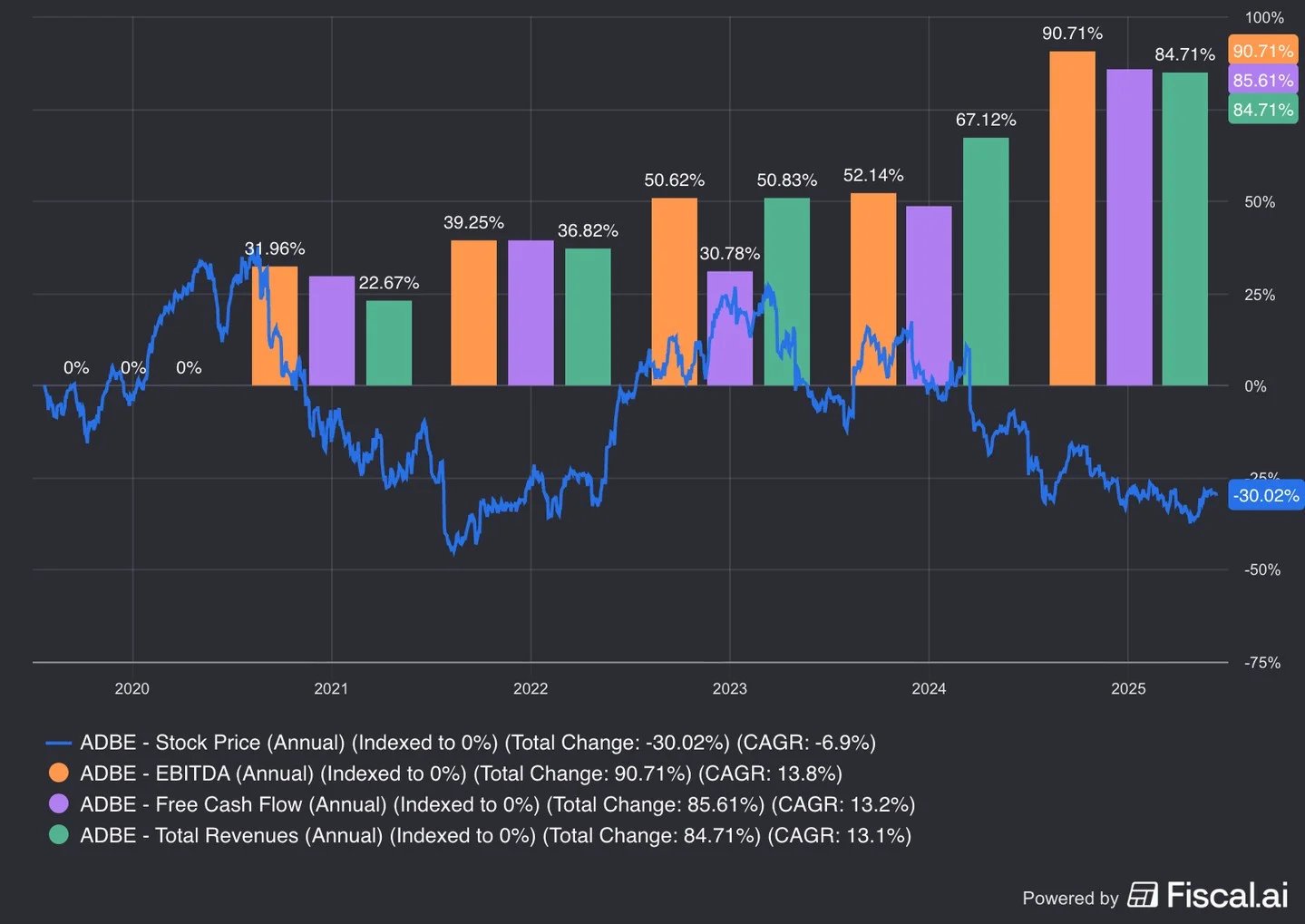

Strong Fundamentals, Weak Stock: Valuation Drives Returns

$ADBE Since 2020: 🔴 Stock Price -30% 🟢 Revenues +85% 🟢 EBITDA +91% 🟢 FCF +86% This is a clear example that valuation is everything. You might be right on the business fundamentals, but be wrong on the stock performance. Was $ADBE incredibly overvalued then, or is...

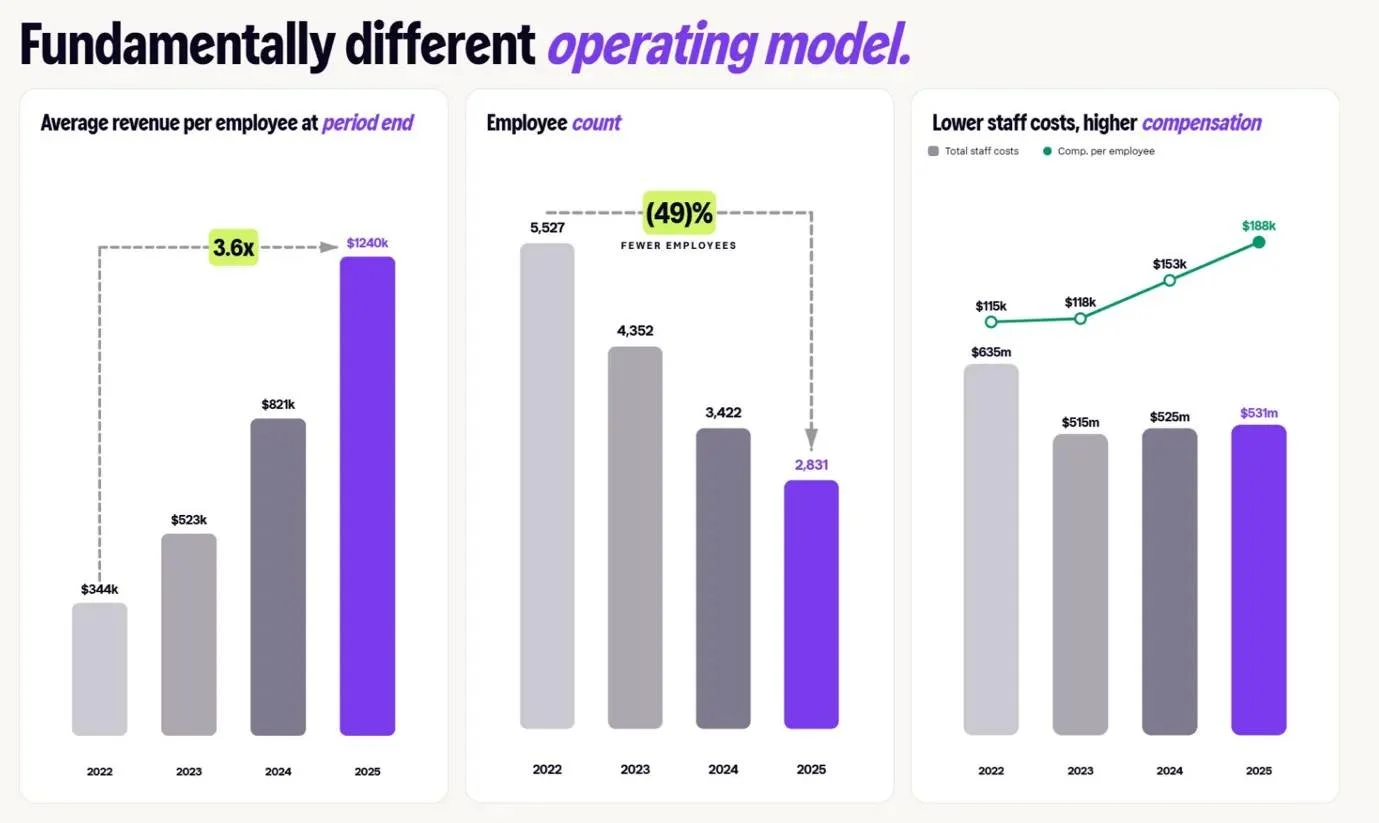

KLAR's Efficiency Gains Outshine Loan Loss Concerns

Investors focus too much on $KLAR loan losses provisions because of strong loan volume growth. They should focus more on $KLAR becoming a more efficient business by improving operating leverage. - Revenue per employee 3.6x from $344K to $1.24M. - The number of...

KLAR's Fundamentals Shine Despite 70% Drop

$KLAR -70% since the IPO It's starting to look interesting: - $128B GMV - 118M Total Customers +28% Y/Y - 15.8M Banking Customers +101% Y/Y - FWD Growth of 26% Yes, credit losses are a growing, but that is natural when non-BNPL loans grow 165% Y/Y....

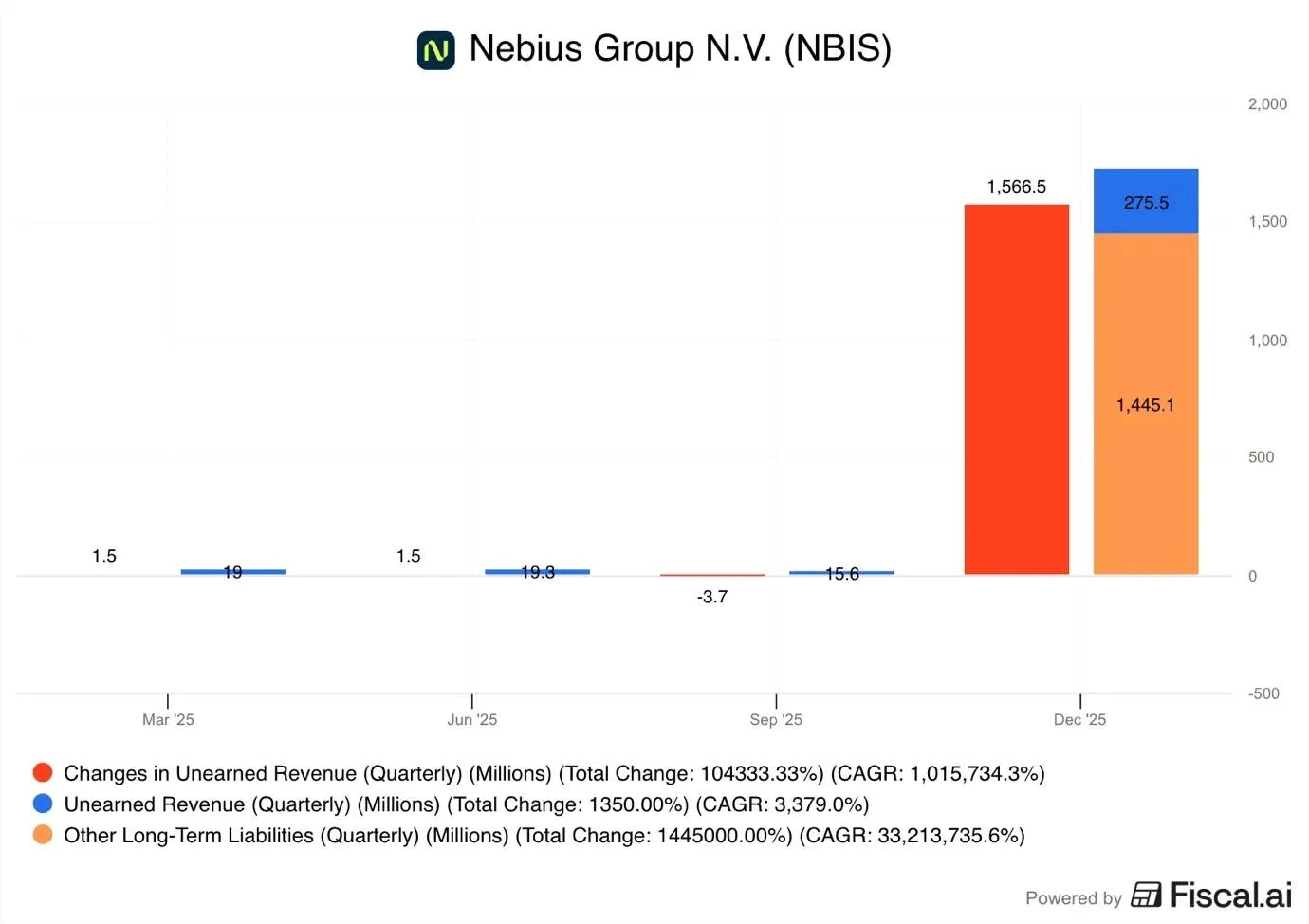

NBIS Holds $1.3B in Future Customer Pre‑Payments

"$NBIS is not getting customer Pre-Payments." Just because they didn't announce it doesn't mean they aren't. Clues are in the balance sheet. $1.6B in deferred revenues. $1.3B of that is non-current, revenues that won't be recognised in the next 12 months. Customers paid $NBIS $1.3B...

Klarna: Potential 5x Upside Amid Subprime Risks

Klarna: 5x Opportunity or a Subprime Lender? $KLAR offers a uniquely asymmetrical profile: - Beat Down Stock - Expanding into Banking - Strong Growth - Potential for improving profits https://www.globalequitybriefing.com/p/klarna-5x-opportunity-or-a-subprime?r=39awso&utm_campaign=post&utm_medium=web

Early Rubin GPU Access Confirms Nebius as True Partner

$NBIS priority allocation from Vera Rubin clearly signals that Nebius is being treated as a real partner That matters because in AI infrastructure, getting the newest GPUs early directly translates into attracting top customers and higher-margin workloads. This validates $NBIS strategy...