Matt Harbaugh

Investor/operator posting about valuation levers (growth, margins, reinvestment, risk) directly relevant to CFO capital strategy and ROI decisions.

Polen Capital Trims Software Holdings Amid AI Overhype

Polen Capital on selling $ADBE, $INTU and $PAYC "The previously discussed price dislocations within the software space have presented opportunities for long-term patient investors and we believe it prudent to consolidate some of the portfolio around businesses where we believe the AI disruption concerns are excessive and are unlikely to materially affect their moat."

Polen Capital Q1 Down

Polen Capital Focus Fund is down -17% in Q1 Buys: $LRCX, $META, $ROL Sold: $ABT, $ADBE, $BSX, $PAYC, $INTU Added to: $CSGP, $SHOP, $NOW Trimmed: $AMZN

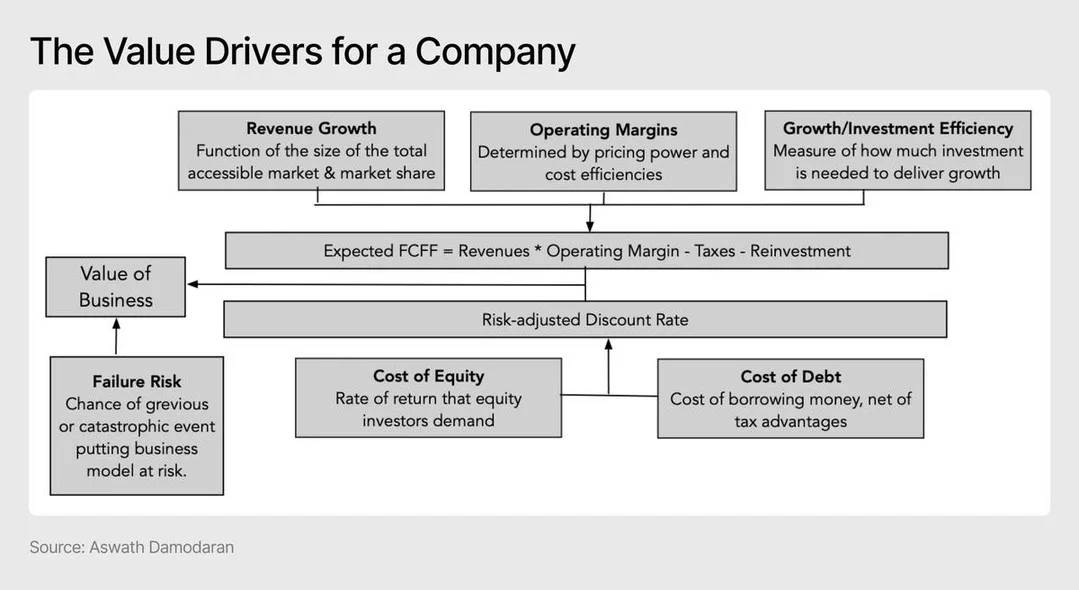

Four Key Levers for Valuation: Growth, Margins, Capital, Risk

Aswath Damodaran on the 4 levers to valuation 1. Revenue Growth 2. Operating Margins 3. Reinvestment (or Investment Capital Turnover) 4. Risk (Continuous and Discrete)

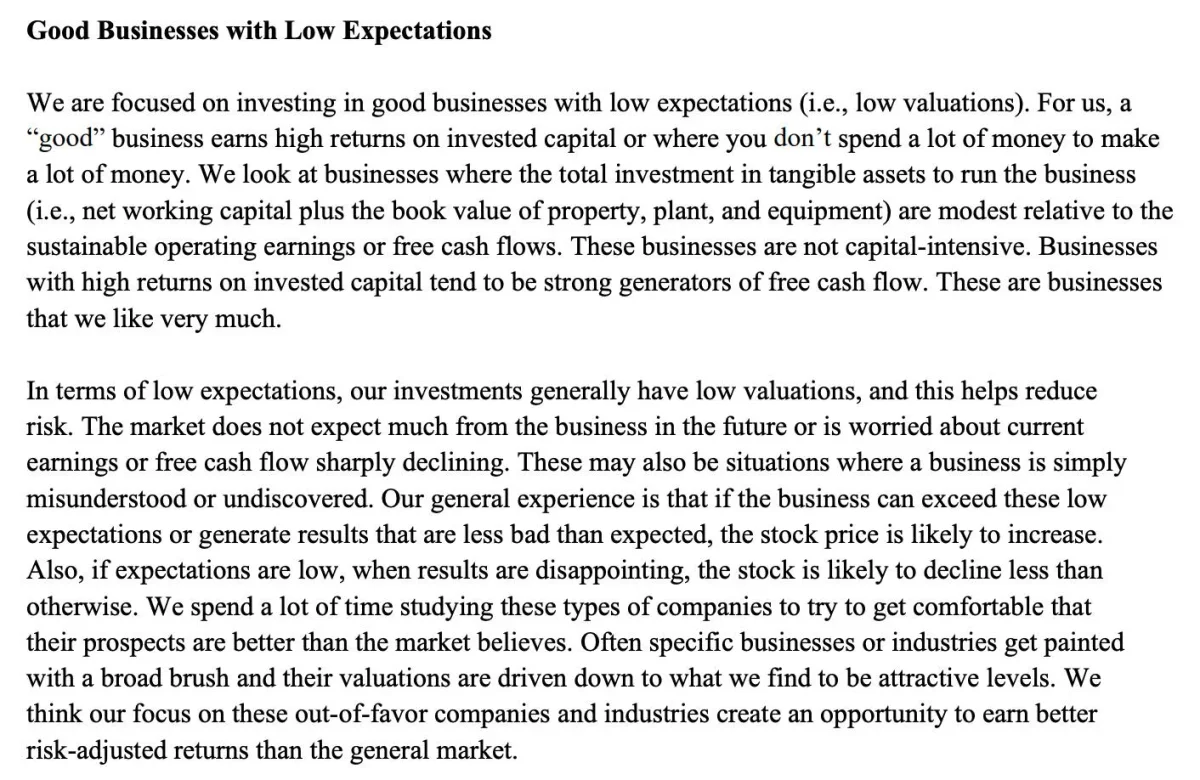

Betting on Undervalued Companies That Beat Low Expectations

Lowell Capital on investing in good businesses with low expectations "Our general experience is that if the business can exceed these low expectations or generate results that are less bad than expected, the stock price is likely to increase. We spend a...

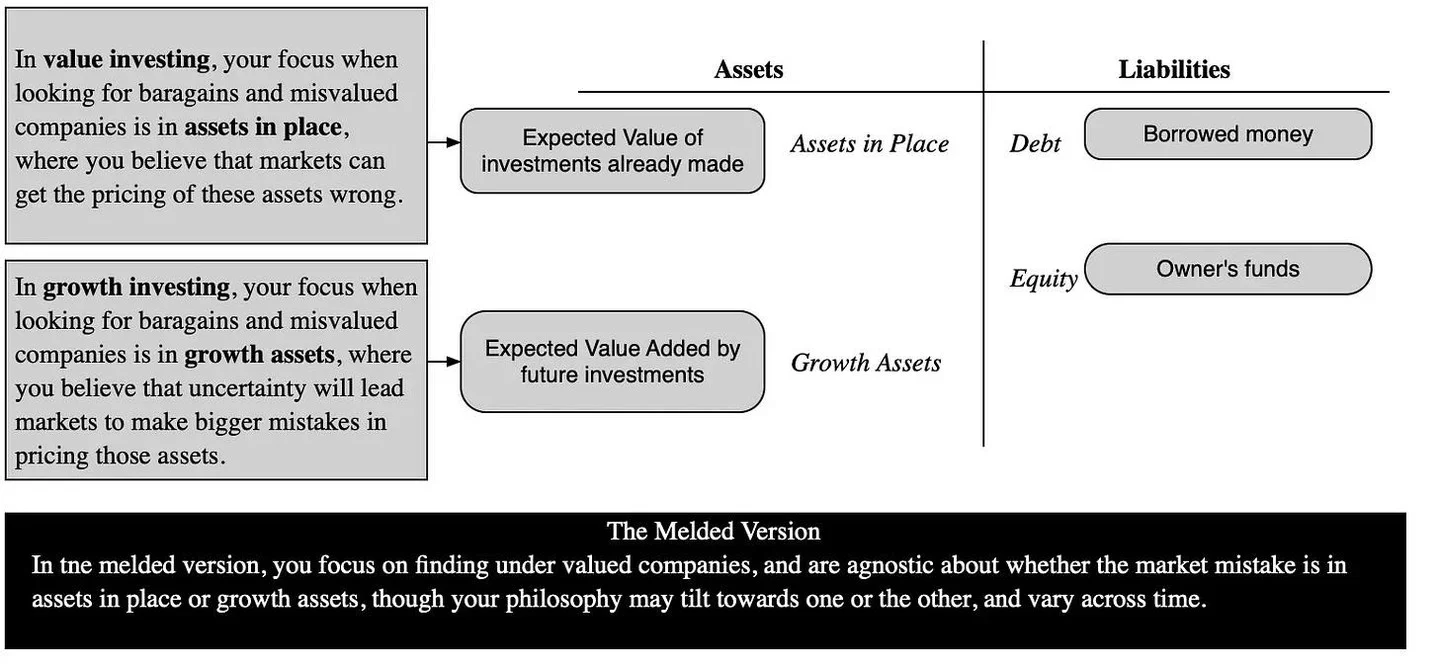

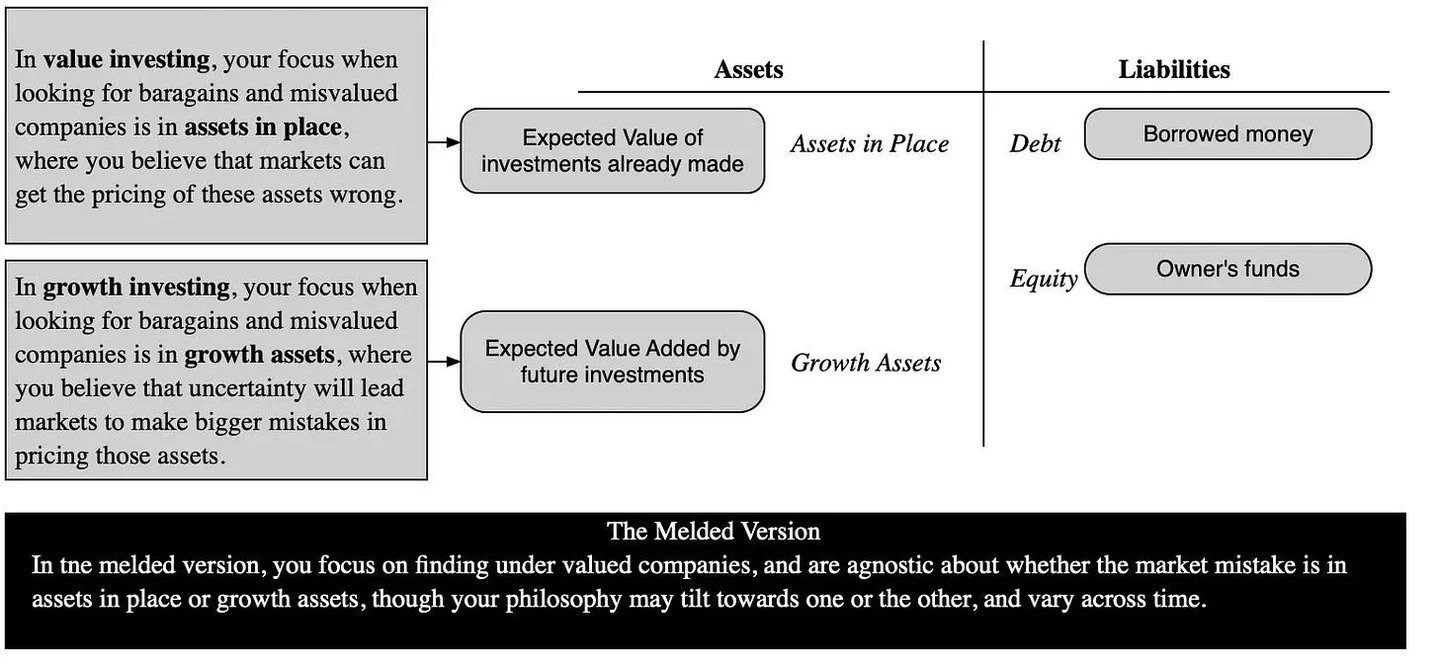

Value Hunts Existing Mispricings; Growth Seeks Future Misvaluations

Aswath Damodaran on value investors vs growth investors "Value investors view their odds of finding market mistakes to be greater with assets-on-place, whereas growth investors feel that their odds are better in finding misvalued growth assets."

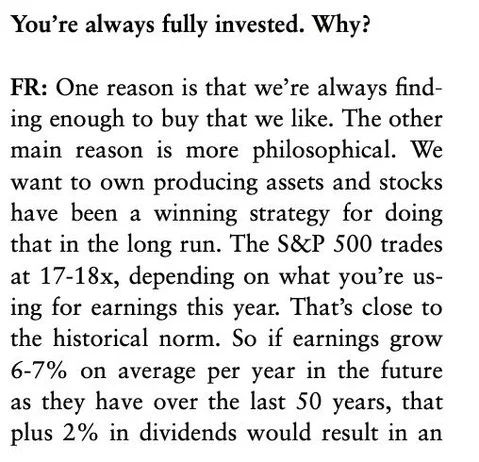

Invest Fully, Skip Cash When Companies Outperform 5%

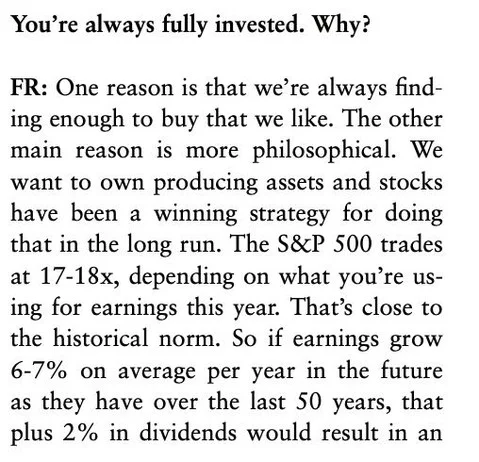

Francois Rochon on being fully invested "If we continue to find companies that we believe can do five percentage points better than that on an annualized basis over many years, why would we hold cash?"

Sustained High ROIC Defies Mean Reversion, Needs Complex Valuation

Michael Mauboussin on fade rates "ROICs regress toward the mean as the result of competition, changing market conditions, and luck. But there is a substantial body of research that shows some companies produce high ROICs for sustained periods, often measured in decades. This...

Only 18% of US Public Firms Survive Long‑term.

Michael Mauboussin on survival rates for U.S. public companies "For every 100 companies, 18 survived and 82 died. Of those that died, 43 were the result of mergers and acquisitions (M&A). The other 39 were delisted for reasons other than M&A, with...

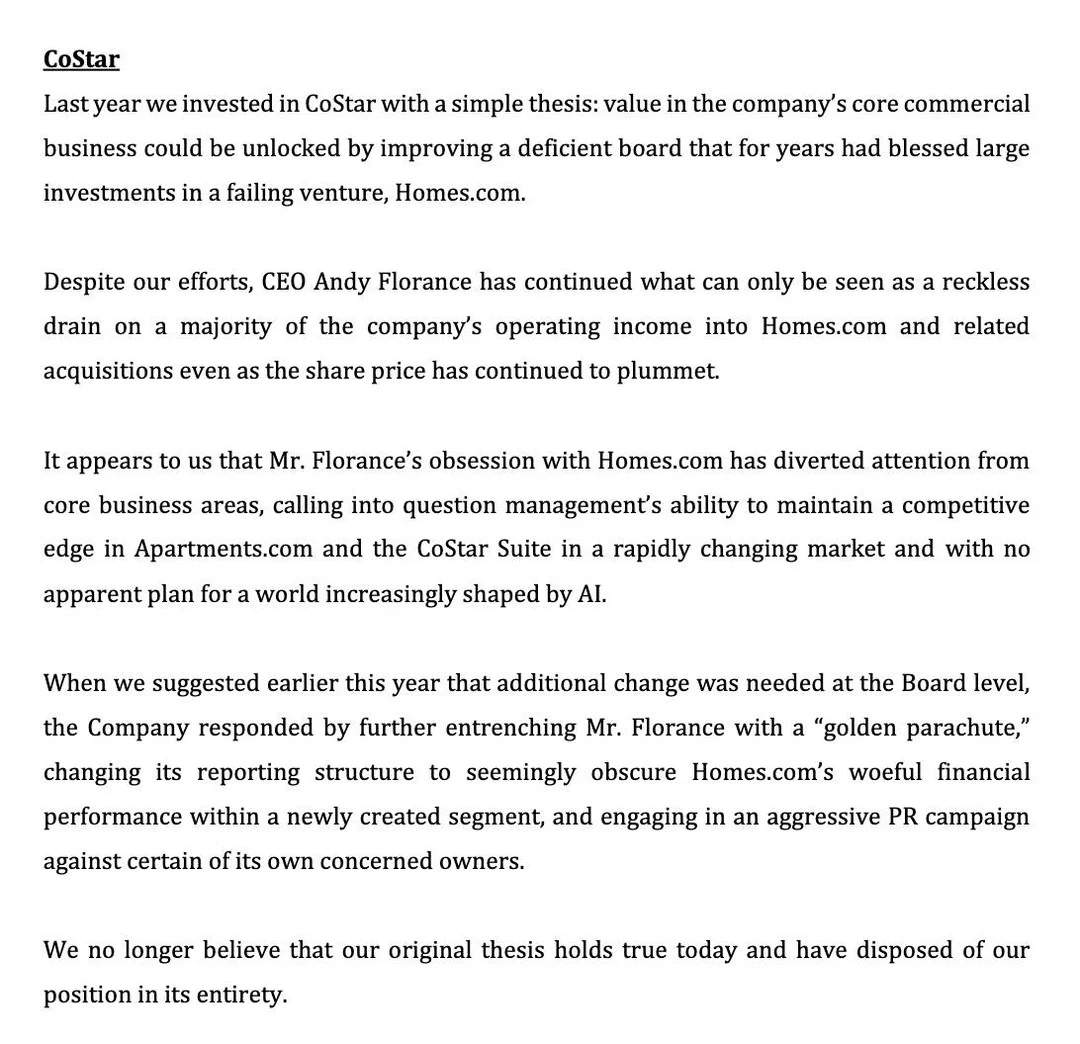

Dan Loeb Dumps CSGP, Citing Reckless CEO Spending

Dan Loeb sells out of $CSGP "CEO Andy Florance has continued what can only be seen as a reckless drain on a majority of the company's operating income into Homes,com and related acquisitions even as the share price has continued to...

Consistent Outperformance by Active Managers Is Rare

Very few active investors win consistently over time "While there some active money managers who “beat the market” over a year, two years or even five, very few are able to hold on to these excess returns as you lengthen...

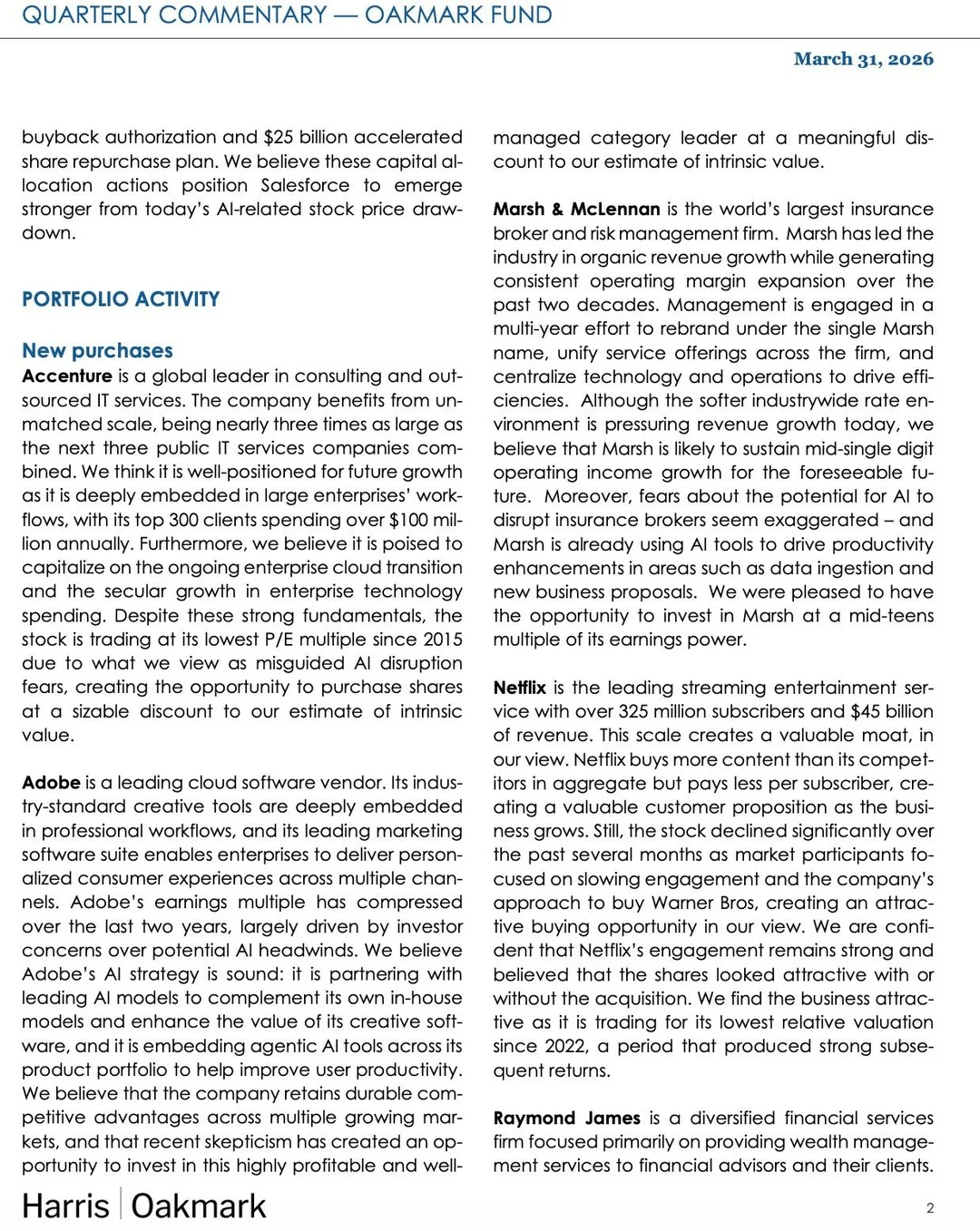

Nygren Sees Adobe Undervalued, Buys at Discount

Bill Nygren buys $ADBE in Q1 "We believe that the company retains durable competitive advantages across multiple growing markets, and that recent skepticism has created an opportunity to invest in this highly profitable and well-managed category leader at a meaningful...

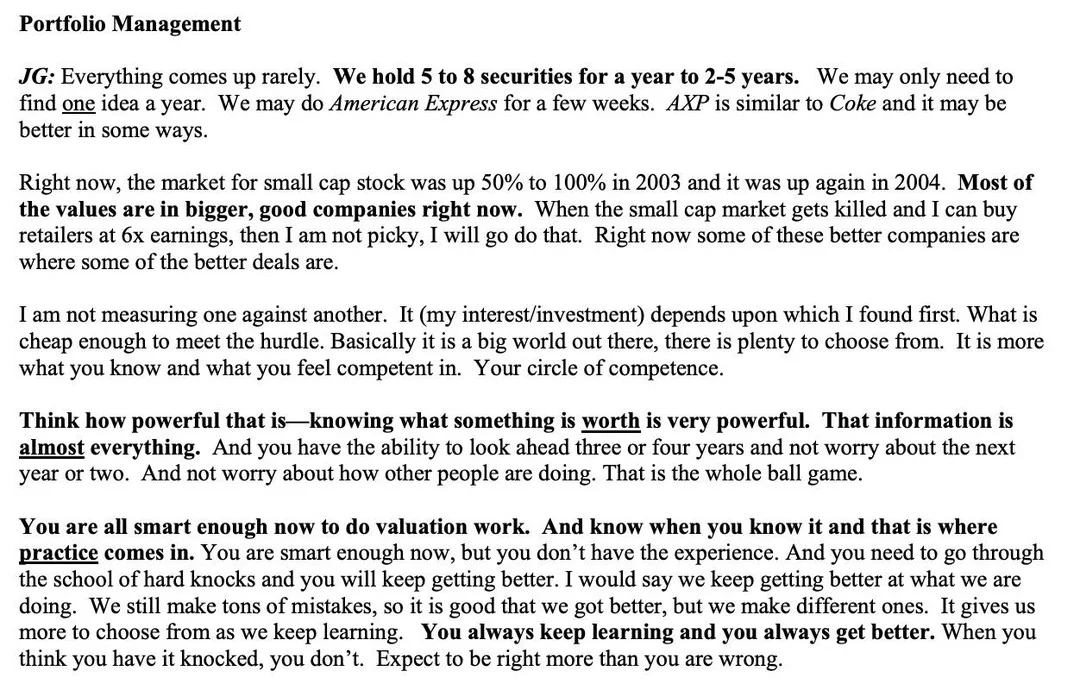

Focus on a Few Long‑term Holdings, One Idea Yearly

Joel Greenblatt on portfolio management "We hold 5 to 8 securities for a year to 2-5 years. We may only need to find one idea a year."

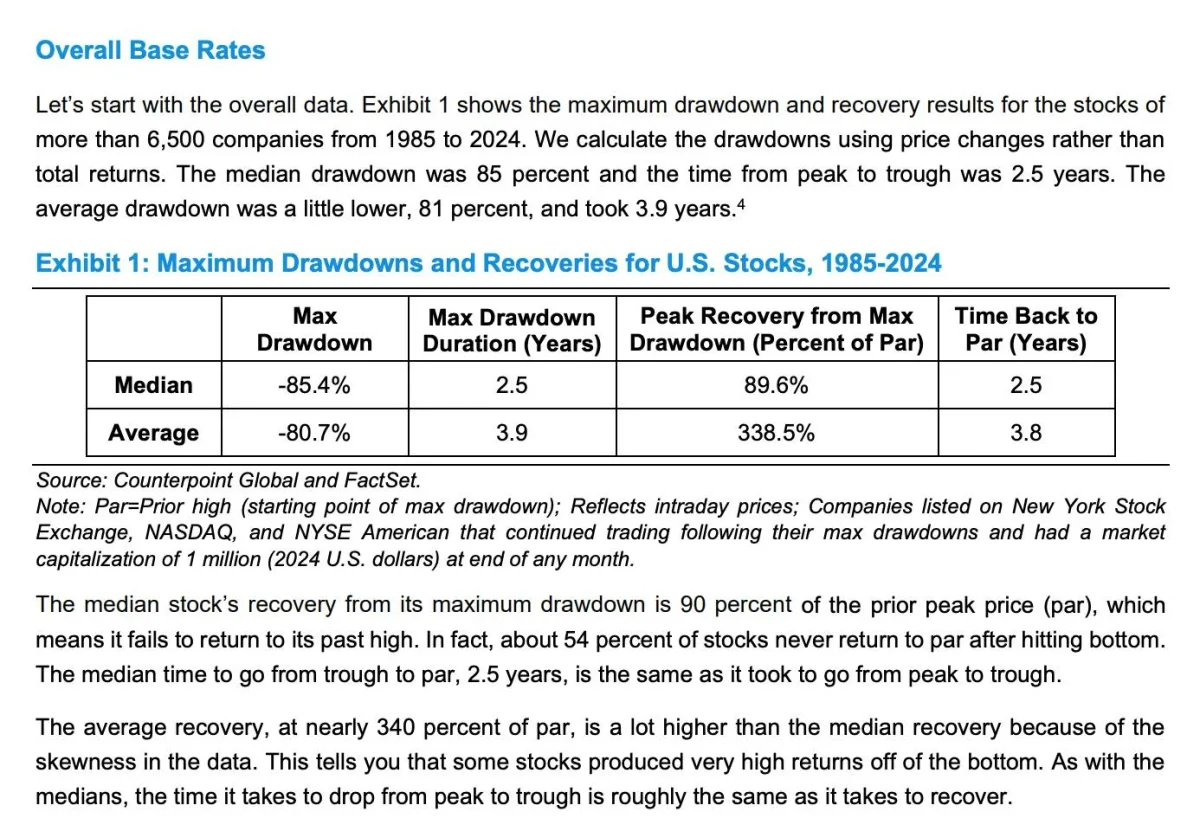

Most Stocks Lose 85% and Half Never Recover

Michael Mauboussin on drawdowns "The median drawdown for the 6,500 stocks in our sample from 1985-2024 was 85 percent and took 2.5 years from peak to trough. More than one-half of all stocks never recover to their prior highs."

Let Winners Run, Trim Losers: Long‑Term Position Sizing

Francois Rochon on position sizing and activity "We typically hold 20 to 25 positions and our average holding period is close to seven years. While we'll cut back on a position that gets over 10% , for the most part our...

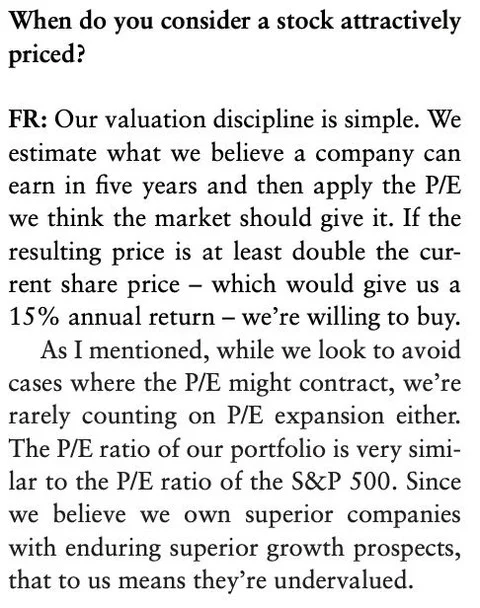

Buy When Five‑Year Earnings Valuation Doubles Current Price

François Rochon on valuation "Our valuation discipline is simple. We estimate what we believe a company can earn in five years and then apply the P/E we think the market should give it. If the resulting price is at least double...

Stick to Quality: 27 Years of Market‑Beating Returns

Francois Rochon has beaten the market over the past 27 years He built his edge by staying within his circle, focusing on quality businesses that grow above the rate of the market, and avoiding terrible businesses with poor economics Learn more about...

Fewer Investment Decisions, Better Business Quality Focus

Chuck Akre on decision-making "The fewer investment decisions we make, the less exposure we have to making mistakes. Obviously, these decisions that are made must be correct, which is why we spend so much time trying to understand the quality of...

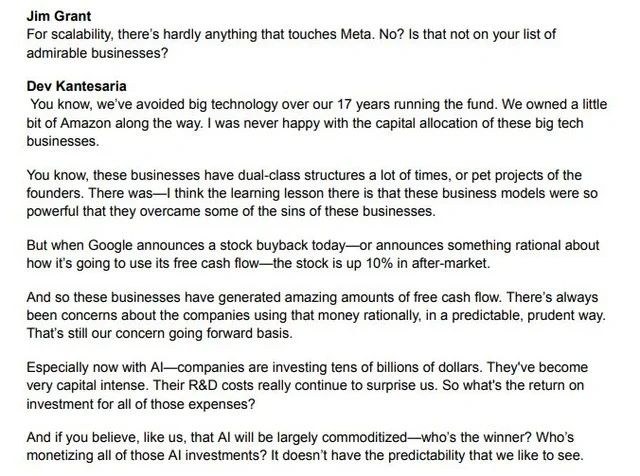

Dev Kantesaria Doubts Big Tech's Capital Allocation Predictability

Dev Kantesaria on not investing in $META and Big Tech "I was never happy with the capital allocation of these big tech businesses... it doesn't have the predictability that we like to see."

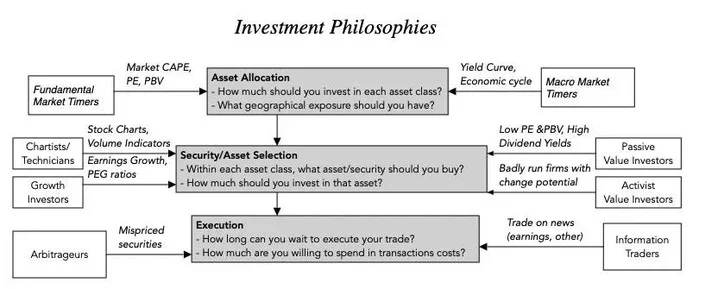

Blend Investment Philosophies to Sharpen Your Edge

Aswath Damodaran on where your investment philosophy fits in the investment process "Even if you feel that you have an investment philosophy in place, I think being aware of how others approach markets and keeping an open mind, where you borrow...

Value Hunts Assets‑in‑place; Growth Hunts Misvalued Growth

Aswath Damodaran on the difference between value investors vs growth investors "Value investors view their odds of finding market mistakes to be greater with assets-in-place, whereas growth investors feel that their odds are better in finding misvalued growth assets.""

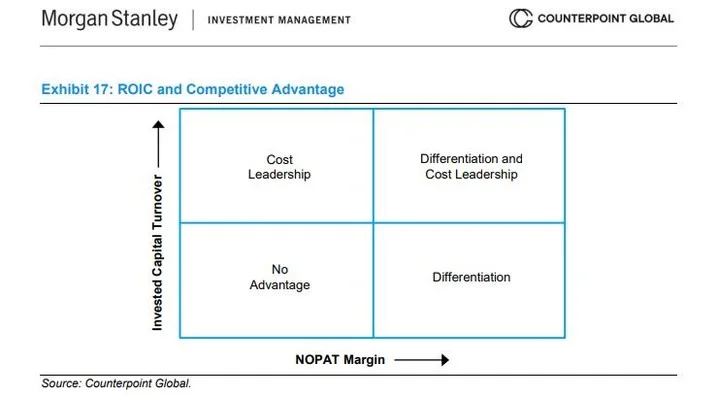

ROIC Sources Dictate: Differentiate or Lead Costs

Michael Mauboussin on ROIC and Competitive Advantage If a business has a high ROIC from a high NOPAT margin, focus on differentiation If a business has a high ROIC from a high invested capital turnover, focus on cost leadership Very few businesses...

Misanalysis Is Investing’s Biggest Risk, Mitigated by Rigorous Research

Nick Sleep on the biggest risk in investing "In our opinion, the biggest risk in investing is the risk of misanalysis. We seek to control this risk through the quality of our research, especially through applying what we have learnt."

Master One Business Inside Out to Invest Wisely

Li Lu on how to become a great investor "Start learning from the best - listening, studying, and reading. The best way to do it is to study one business inside and out for the purpose of making the investment."

Good Research Drives Long‑term Success, Not Immediate Timing

Nick Sleep on focusing on what you can control "The quality of our research-based decisions overwhelmingly determines whether we will do well in the long run. But it has almost no influence over the timing of these results."

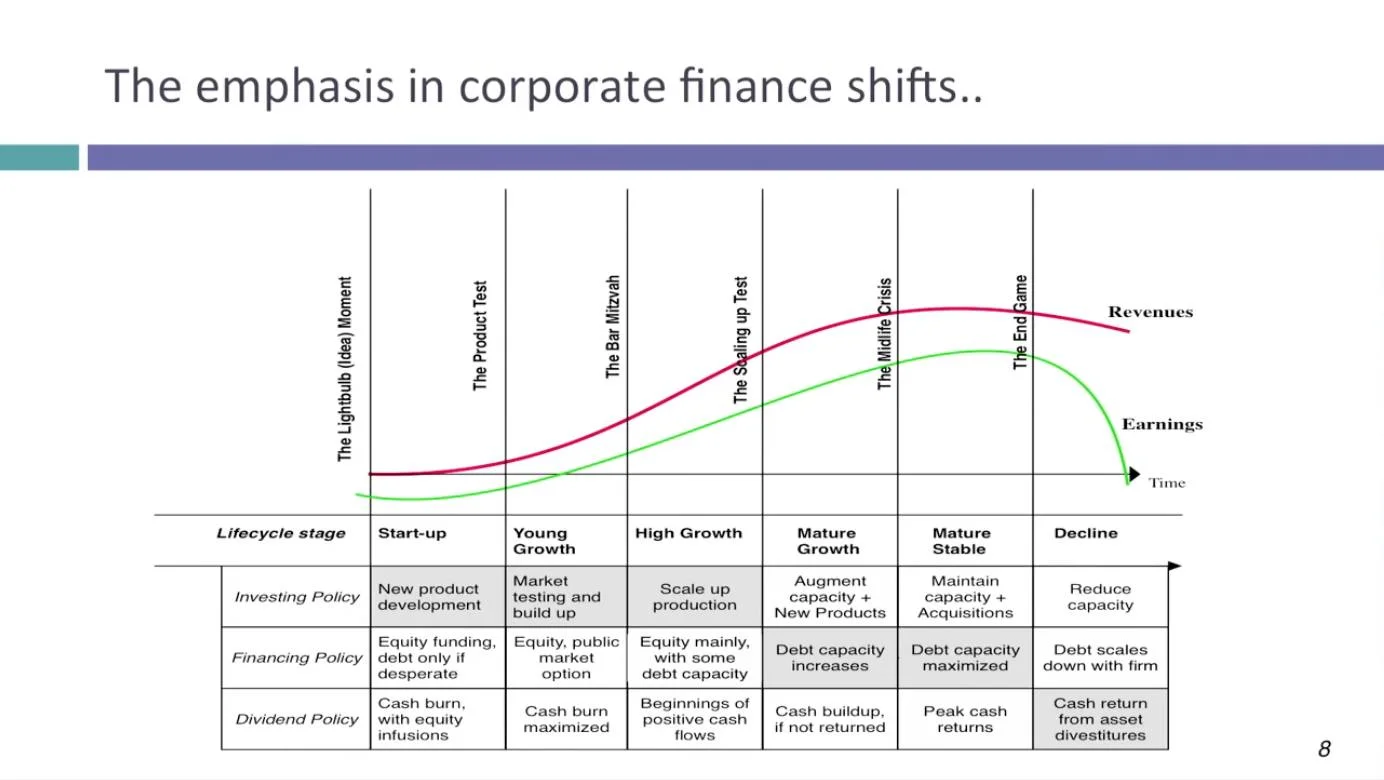

Act Your Age: Align Business Focus with Lifecycle

Aswath Damodaran on how the focus of a business changes depending on the company's lifecycle Companies that don't act their age will destroy value

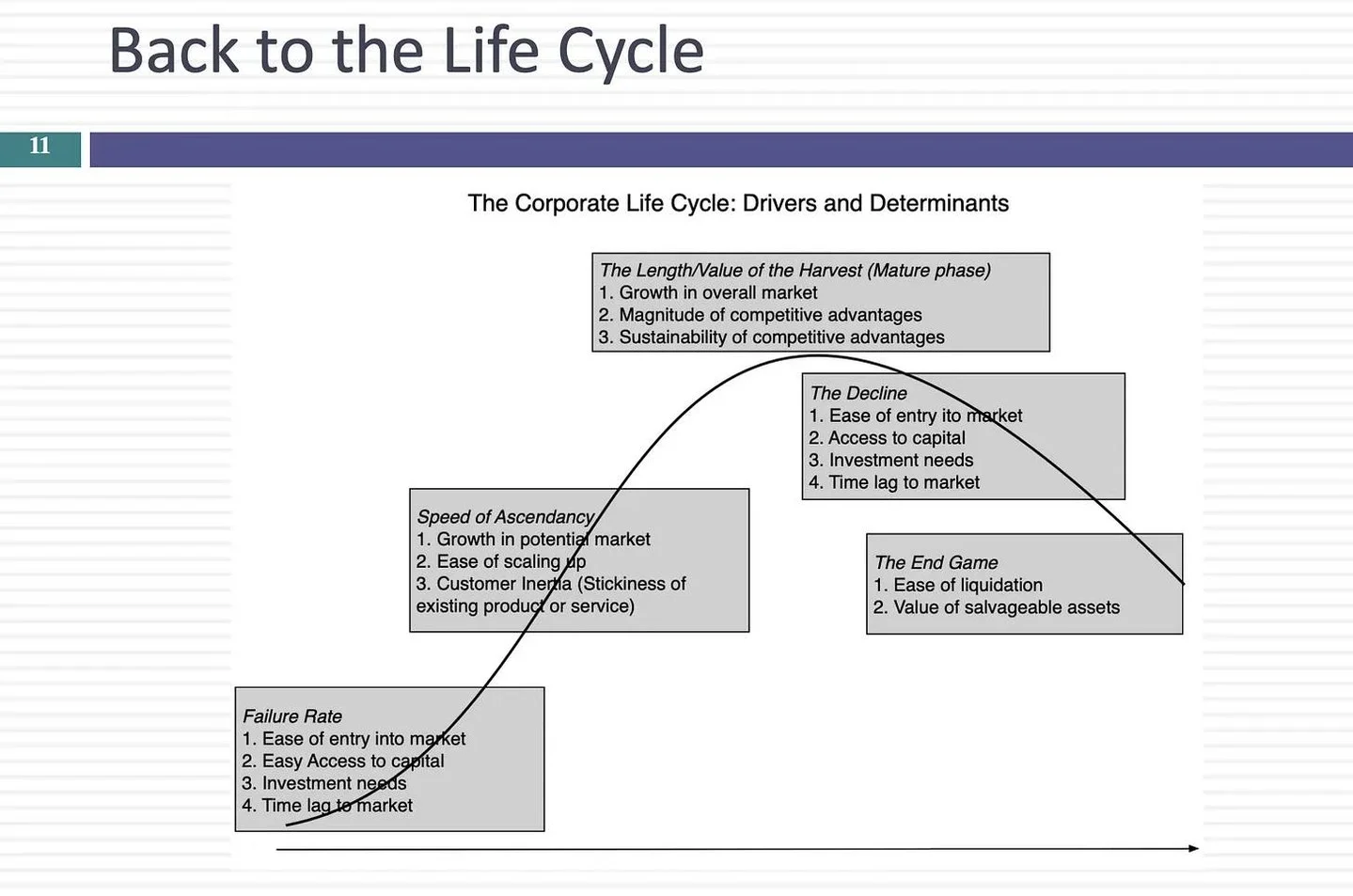

Same Levers Fuel Growth and Trigger Decline

Aswath Damodaran on the determinants of a company's lifecycle "What allows companies to grow quickly are: ease of scaling up, how quickly you can enter businesses, and how little capital you need to grow. But what causes companies to decline are...

Seek 5% Annual Edge, Keep Cash Out

Francois Rochon on being fully invested "If we continue to find companies that we believe can do five percentage points better than that on an annualized basis over many years, why would we hold cash?"

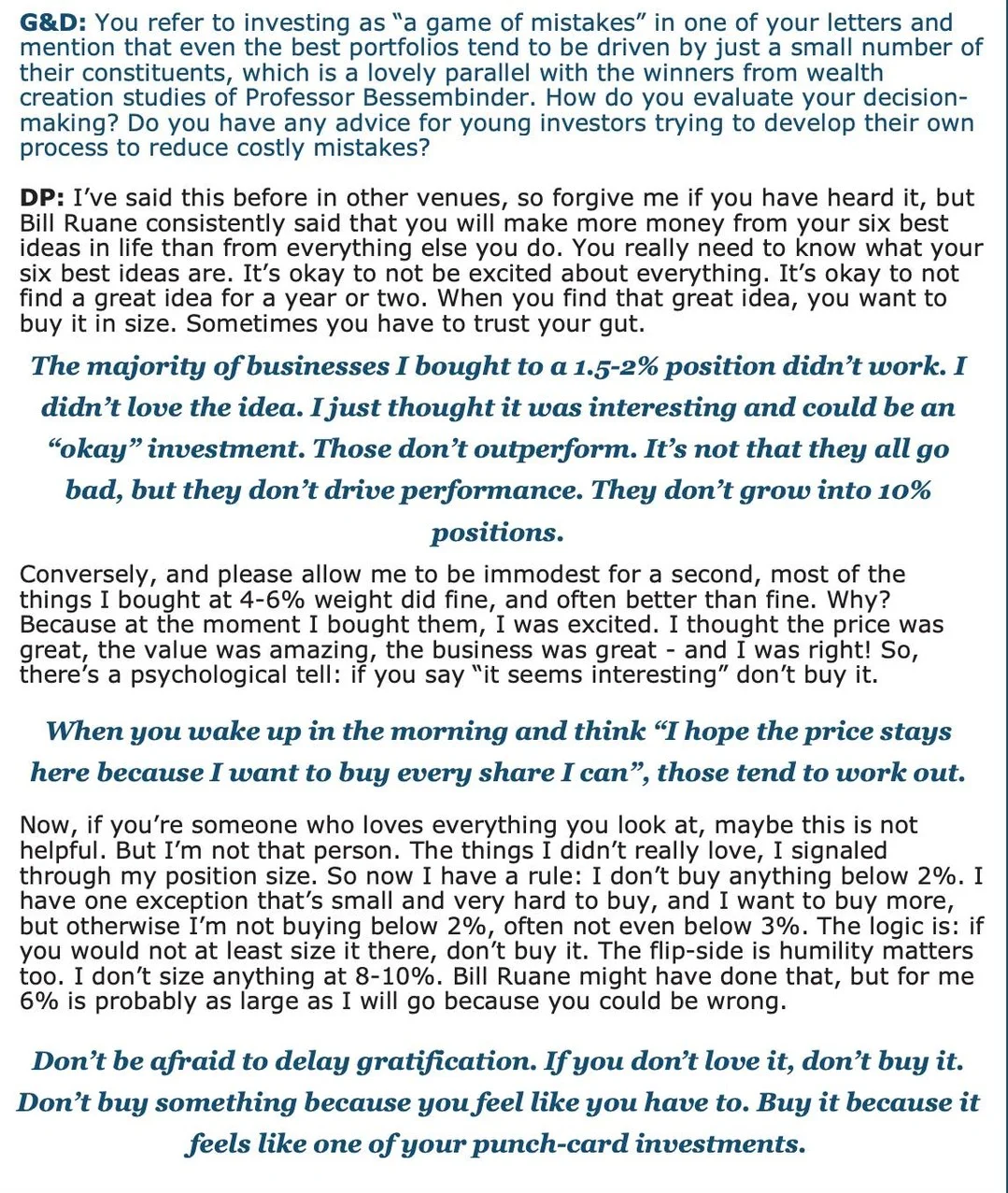

Bet Big on Your Six Best Ideas

David Poppe on capital allocation "You will make more money from your six best ideas in life than from everything else you do. When you find that great idea, you want to buy it in size."