Speedwell Research

Independent equity researcher posting concise European earnings recaps and valuation takes on Euronext‑listed names.

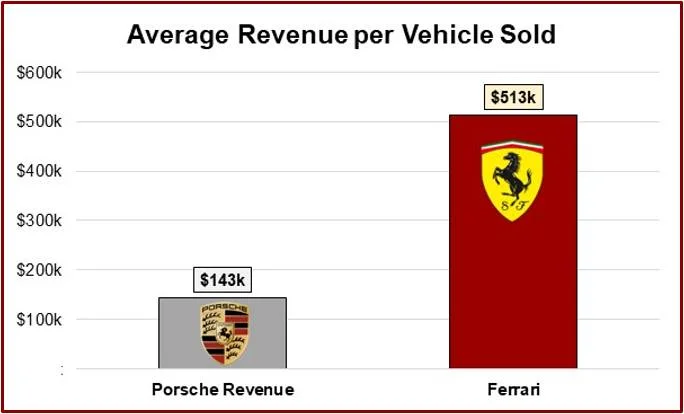

Ferrari's Low Volume Yields 3‑plus× Higher Per‑car Revenue

Ferrari produces ~13k vehicles annually whereas Porsche produces nearly 50k 911 models (their iconic sports car) and another 20k 718s (their lower end sports car). Porsche also produces a lot of SUVs and Sedans, bringing their total annual volume around to 300k—over 20x more than Ferrari’s. The higher volumes mean it is harder for them to charge (relatively) as a high of a price. Ferrari’s average revenue per vehicle sold (including all revenues) is >$500k versus Porsche at ~$140k. $RACE

Ferrari’s 20‑Month Waitlist Keeps Desire High

Ferrari manages desirability by capping availability with a waitlist of about 20-24 months. Ferrari believes that this is the sweet spot between it being too long that clients move on and long enough that they keep desirability high by making...

Industry Insiders Prefer Toast Over SkyTab Despite Higher Cost

Former VP at $FOUR notes that a majority of industry insiders would say that Toast is better than SkyTab for restaurants. He talks about how Toast has older software in a good way, as it means all of the kinks...

Earnings Reflect LVMH’s Focus on Quality Products

Bernard Arnault on how earnings are a consequence of building great products "The figures themselves are nothing, but the consequence of the excellent quality of our products, our excellent strategy, but, of course, it is, they are a direct reflection of...

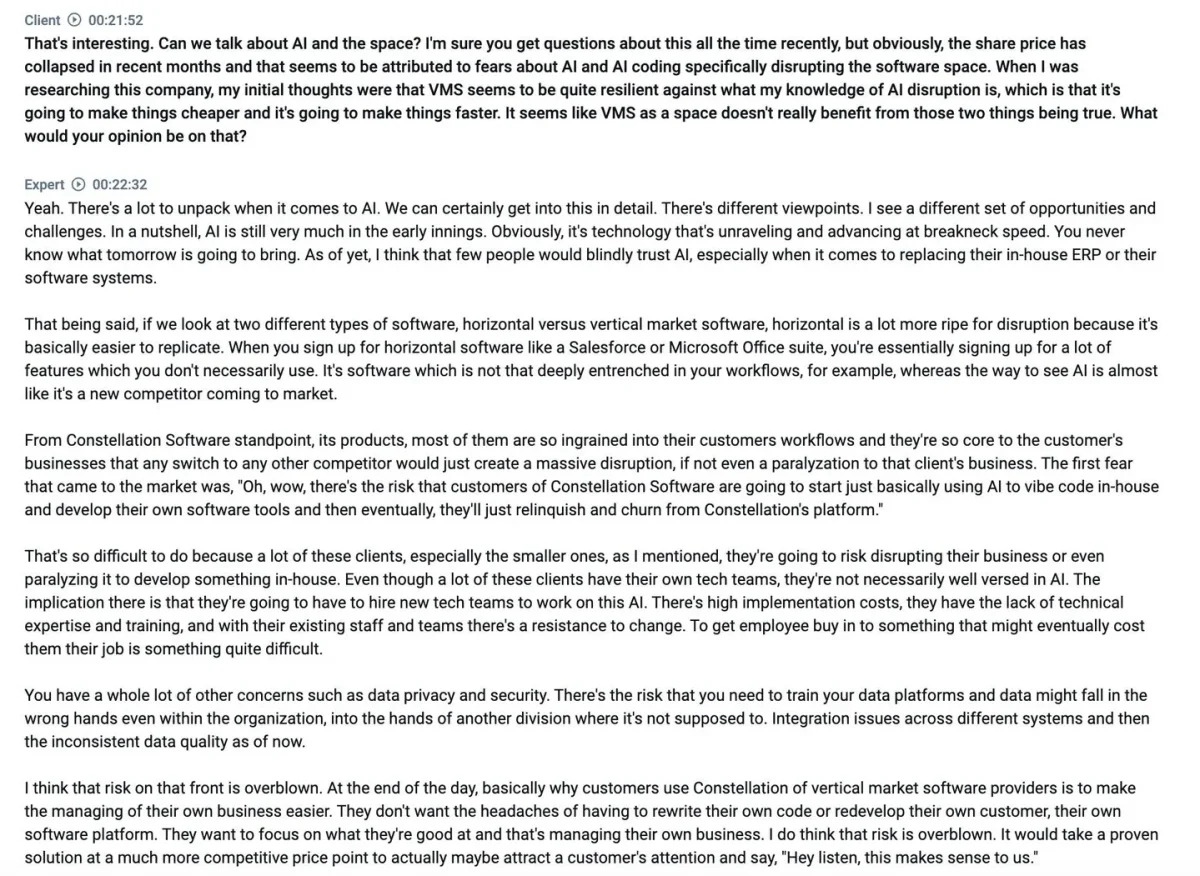

Minimal AI Savings Dampen Municipal Switch Incentive

Former head of M&A at $CSU on how AI affects switching costs "The delta in terms of potential cost saving is minimal and the incentive to switch becomes less. If you're managing whatever it is for a municipality, say in Europe,...

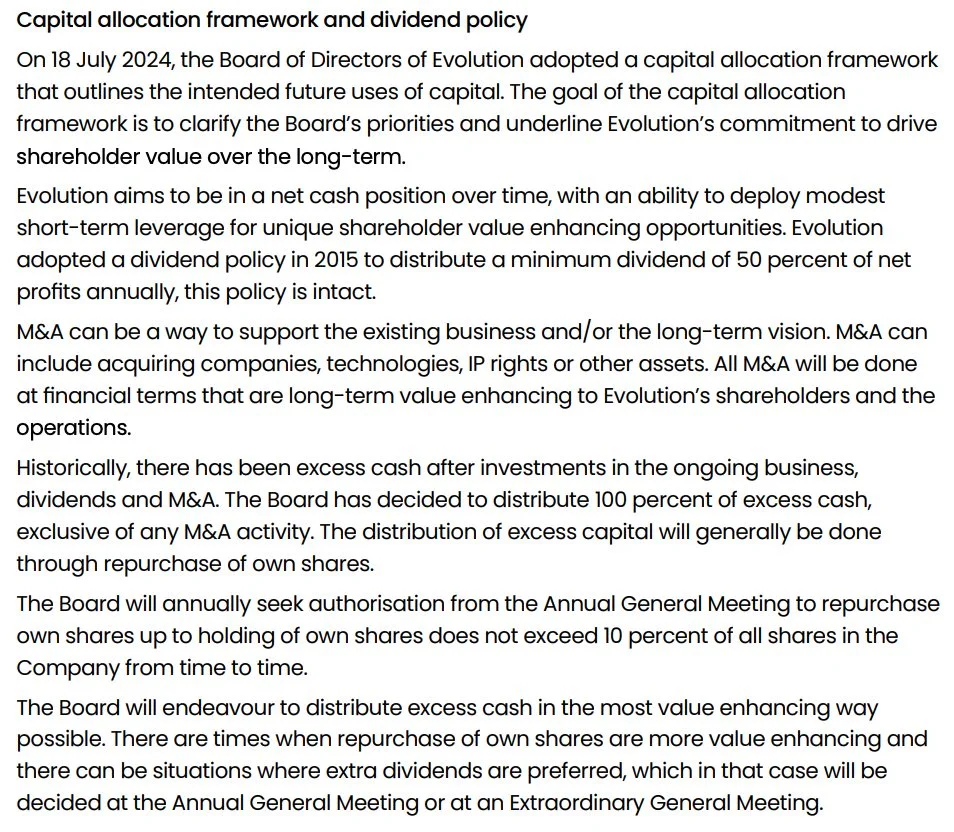

EVO Allocates All Excess Cash to Share Buybacks

$EVO to distribute 100% of excess cash to share repurchases "The board has decided to distribute 100 percent of excess cash, exclusive to any M&A activity. The distribution of excess capital will generally be done through repurchase of own shares." - 2025...

Customers Choose Vertical SaaS to Avoid AI Overhype

Former head of M&A at $CSU on why the AI risk is overblown "At the end of the day, basically why customers use Constellation of vertical market software providers is to make the managing of their own business easier. They don't...

Trust Your Research, Not Borrowed Judgement

Don’t borrow judgement. The reason why we spend hundreds of hours analyzing a business is to thoroughly understand it. The purpose of the research is to build confidence in our assumptions. The valuation then dictates what the return those assumptions will...

Pricing Is Integral to Brand Identity, Says Former LVMH CFO

Former $LVMH CFO on obsession with brand and pricing: "They are really obsessed about the brands, how the brands look, how the brands react, the ability of the brands, the aspirational brands in order to create a really aspirational brand, highly...

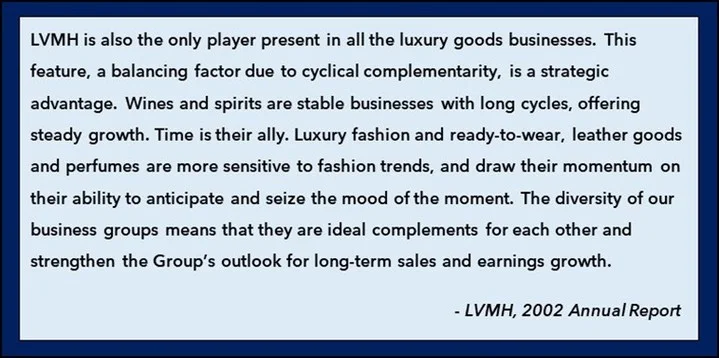

LVMH Balances Cycles by Pairing Stable Spirits with Fashion

$LVMH laid out the strategy driving their acquisitions in 2002 Holding so many different luxury goods businesses would help to balance the cyclicality of each category. “Wines and spirits are stable businesses with long cycles” versus luxury fashion and ready-to-wear...

Luxury Endures, Tech Fades: Dom Pérignon Outlasts iPhone

$LVMH CEO Bernard Arnault on the difference between iPhones and Dom Pérignon: "In 50 years' time, will the iPhone still be used? Or the people who are making it today, will they have found what will be at the cutting...

Taiwan's E‑commerce Lag Stems From Cultural and Logistical Barriers

Former Head of Retail at $CPNG on why e-commerce penetration in Taiwan is smaller compared to the U.S. and China

Great Returns Can Hide Dangerous Stock Concentration

François Rochon is a well known investment manager who has compounded at ~15% annualized for 30 years (!) In 2002 though he was much more obscure. A single stock was 20% of his portfolio. Below he shares his thoughts on...

Buffett & Munger Reveal True Cost of Equity

Most investors misunderstand the cost of equity. Below is the most explicit Buffett has ever been on his cost of equity... BUT the real insights come from Charlie Munger's push back and Buffett's Punch Card Idea ⬇️Link⬇️

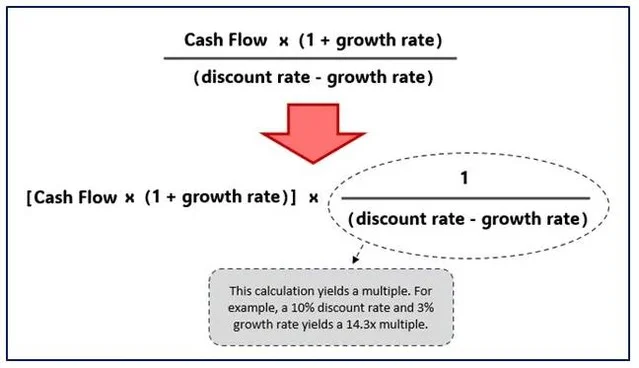

Terminal Values Are Just DCF Shortcuts via Multiples

Terminal values are themselves short-hands for DCFs. This is because a terminal value is essentially a multiple. And a multiple is a short-cut for a DCF. More in the memo below 👇

PRM Restructures Contracts to Stabilize Fire Safety Business

$PRM on how they have transitioned the fire safety business to be less cyclical by restructuring their fire retardant contracts

Diversification Fuels LVMH’s Broad Luxury Consumer Reach

Former VP at $LVMH on their competitive advantage "LVMH benefits from its level of diversification. They cover so much ground in their understanding of an ability to reach a consumer interested in luxury products from so many different angles."