Galloway: Market Severely Undervalues WW's Brand and Growth Potential

"We believe the market is dramatically undervaluing WW’s brand, clinical business, member ecosystem, and long-term strategic potential," said Bruce Galloway, Chief Investment Officer of Galloway Capital Partners $WW https://t.co/0PGyApZ7hM

SK Hynix Still Cheap After 9x Surge

SK Hynix is up 9x since my April 2025 writeup. Usually, that means the easy money is gone. But here is the strange part: the forward P/E has barely moved. The market still values SK Hynix at ~5-6x forward earnings, as if this...

WeightWatchers Remains Deeply Mispriced, Management Heeds Advice

New writeup: Weightwatchers' 2026 Q1 earnigns report. IMO still the most mispriced security in the market - by far. And thanks to WW management for acting on my advice. Link in bio $WW https://t.co/4CvTI290mv

SK Hynix Lock‑in Hopes Meet Commodity Reality

SK Hynix customers begging for long term lock ins. But of course this time couldn’t be any different. Just a commodity

Bumble's Q1 Woes Mask 30% Earnings Yield

I wrote an update on Bumble after Q1. Still a messy setup: users are down, the stock is hated, and the new loan is expensive. But bumble remains highly cash generative and I get to a near 30% owner earnings...

Memory Stocks May Finally Merit 20× PE Valuation

What if this time is really different for „cyclical“ memory stocks? What if SK Hynix should trade at a PE of 20x I mean, how arrogant would anyone have to be to seriously claim that this time is no different at all?...

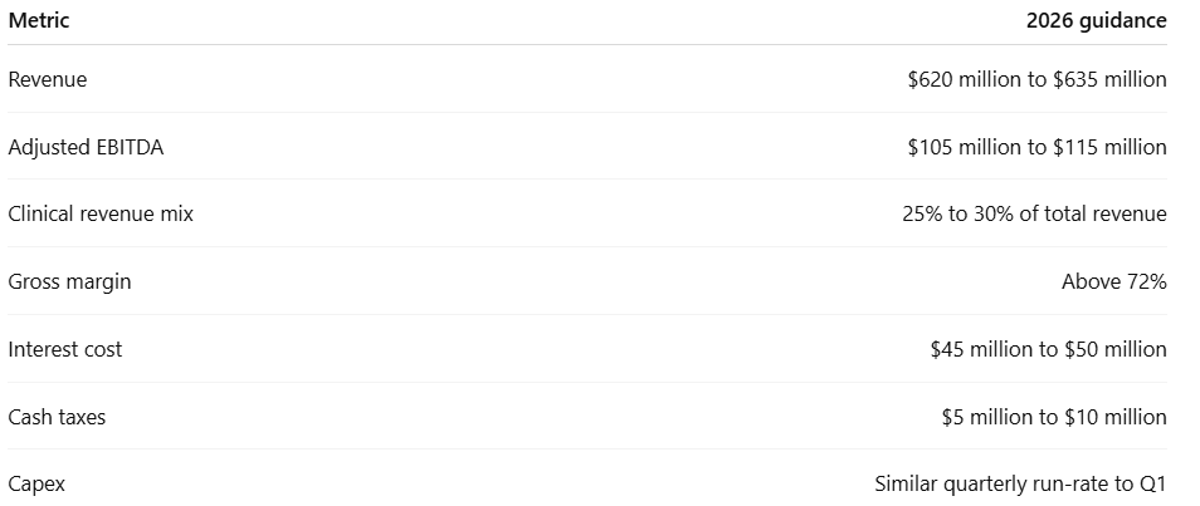

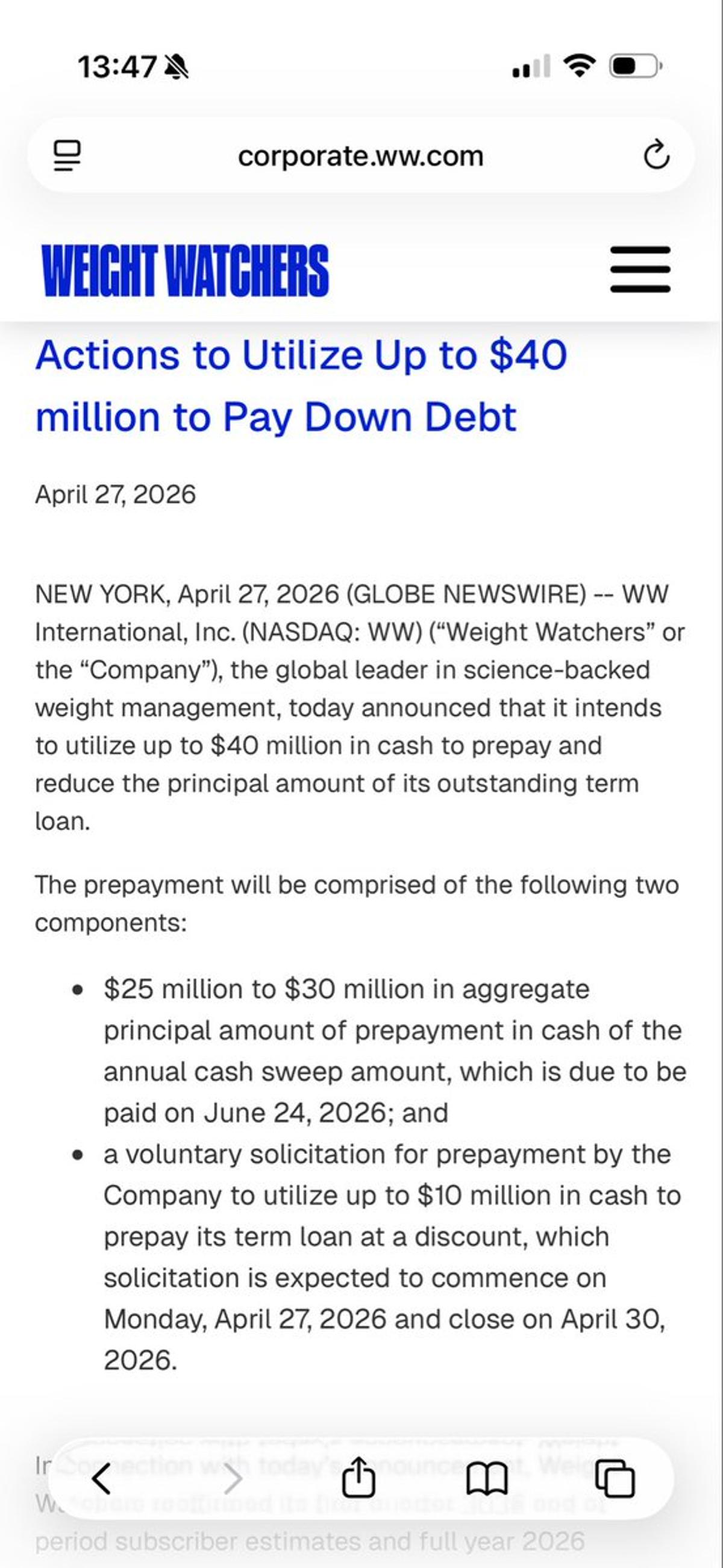

WeightWatchers Cuts $40M Debt, Saves $5M Interest

Weightwatchers to pay down $40m in debt. This is material for owner earnings as it should lead to annual interest expense savings of ~$5 million. $WW https://t.co/QVs2CKLPKy

SK Hynix's 3.8x PE Precedes 2026

SK Hynix with a next 12 month PE of 3.8x and upcoming ADR listing in 2026.

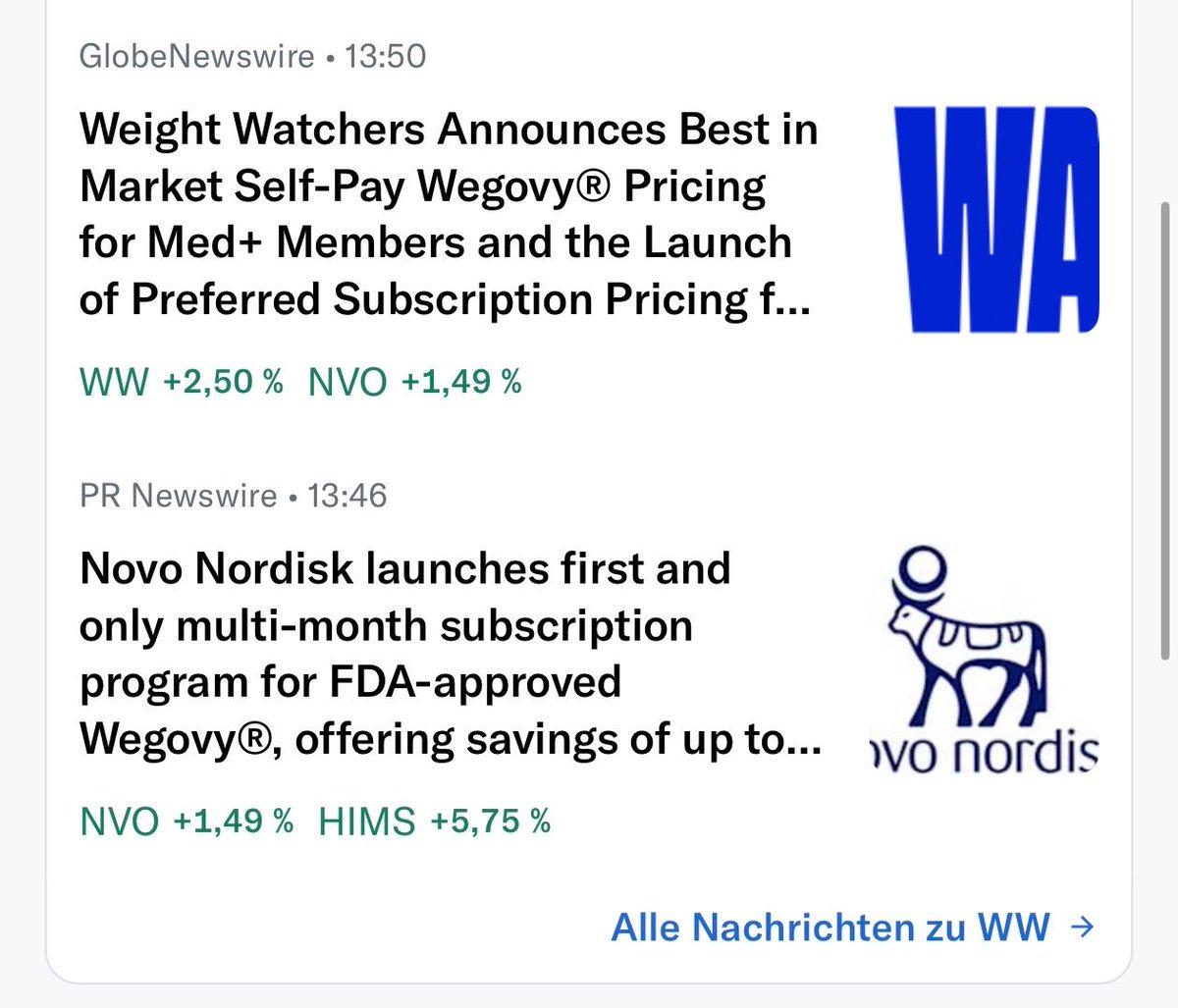

Novo Nordisk's Breakthrough Launch at Attractive 11x PE

Watch the launch of the holy grail of pharma. Beautiful And still at a PE of ~11x. $NVO

Low Multiples Offer Expansion; High Multiples Invite Compression

Guess what, when your portfolio trades at 37x cash flow, multiple compression is a major risk. That’s why my portfolio trades at 3.7x cash flow, so multiple expansion is a major opportunity.

Bumble Rebounds 50% to Rational 30% FCF Yield

Bumble up 50% from the lows. Turns out Mr. Market got a little extreme dumping $BMBL at a >40% free cash flow yield. Now priced at a fully rational ~30% FCF yield.

Weightwatchers Leverages GLP‑1

Weightwatchers now at a market cap of $120m, with: • $160m cash • $110m adj. EBITDA guidance for 2026 • some 80% growth in its GLP-1 business GLP-1 transition couldn’t be any better as Novo Nordisk is going all in on telehealth distribution, with...

Telehealth Gets Discounted GLP‑1 Service, Outsmarts Weightwatchers

GLP-1 as a service and at a massive discount. Entire distribution now massively and exclusively advantaging telehealth providers. Of course Mr efficient thinks that’s a nothing burger for Weightwatchers. Can’t make this up https://t.co/62IYen2o3b

Fewer People, Less Housing; Global Compute Limits Remain Unclear

Obviously, a country with a declining population doesn’t need unlimited residential construction. Much less clear what are the limits to compute needed by the entire world.

Market's Ultra‑Low PE Ratios Signal Doom Forecast

Some next 12 month PE ratios: Bumble: 3.6x Shift4: 7.3x Novo Nordisk: 10.8x HelloFresh: 9.5x Prosus: 9.3x SK Hynix: 5.2x Is Mr Market pricing the end of the world already? $BMBL $FOUR $NVO $HFG $PRX