Banks Gain Amid Software Stock Rout, Despite Credit Questions

•February 6, 2026

0

Why It Matters

With software volatility rising on AI concerns, banks’ limited credit risk makes them a safe haven, supporting share price gains and attracting capital away from riskier sectors. This dynamic could shape portfolio allocations and influence future regulatory scrutiny of tech‑related lending.

Key Takeaways

- •Banks' software loan exposure under 3% of total

- •Bank stocks rose >2% while software index fell 22%

- •Regulators limited leveraged lending, reducing tech risk for banks

- •Investors favor “boring” banks amid AI‑driven tech sell‑off

- •Regional banks up nearly 11% despite tech turmoil

Pulse Analysis

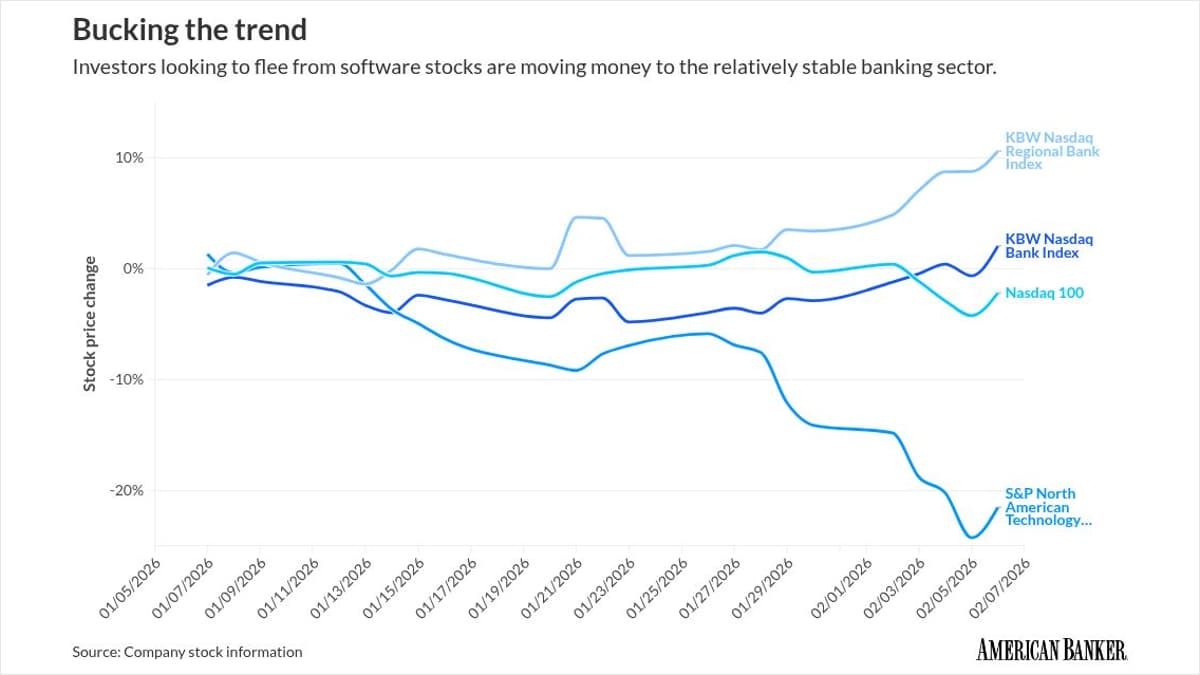

The rapid decline in software equities this month has been driven by mounting anxiety over artificial‑intelligence disruptions, which threaten the profitability of coding firms and, by extension, the borrowers that fund them. As the S&P North American Technology Software Index slid close to 22%, investors scrambled for shelter, turning their attention to sectors perceived as insulated from the tech turbulence. Banking stocks responded positively, with the KBW Nasdaq Bank Index climbing more than 2% and regional bank indices up nearly 11%, underscoring a clear flight‑to‑quality amid the sell‑off.

Behind the rally lies a structural shield: banks’ direct loan exposure to software companies is modest. Bank of America disclosed roughly $14.6 billion in software‑related loans, representing just 1.8% of its commercial credit portfolio, and industry analysts estimate the aggregate exposure across all banks remains below 3%. This limited risk profile is a legacy of post‑2008 reforms that curtailed leveraged lending to high‑growth, asset‑light sectors. Consequently, many tech borrowers now rely on business‑development companies and private‑equity funds, where exposure can reach 25‑35% of loan books.

The market’s tilt toward “boring” banks mirrors the defensive shift observed during the early‑2000s dot‑com bust, when financial institutions weathered tech‑related credit losses with relative ease. Today, fresh capital is flowing into banks, boosting valuations and compressing spreads, while the tech sector grapples with valuation corrections. Should a broader software downturn materialize, the limited bank exposure suggests only a modest impact on earnings, but heightened scrutiny of indirect links—such as BDC holdings—could prompt tighter risk monitoring. For investors, the current environment reinforces banks as a low‑volatility anchor in a volatile equity landscape.

Banks gain amid software stock rout, despite credit questions

0

Comments

Want to join the conversation?

Loading comments...