Banks Need to Choose Carefully Between Public and Private Blockchains

•February 27, 2026

0

Why It Matters

The decision determines cost structures, interoperability, and systemic risk, directly affecting banks’ competitive advantage and regulatory compliance. Selecting open networks can lower transaction fees and reduce concentration risk, while private chains may entrench vendor lock‑in.

Key Takeaways

- •Public blockchains enable permissionless interoperability across banks

- •Private chains create vendor lock‑in and concentration risk

- •Open networks improve auditability and regulatory transparency

- •Tokenized asset market estimated at $33 billion

- •Banks should assess control, incentives, and future changes

Pulse Analysis

The financial sector has moved past the rhetorical question of whether blockchain belongs in banking and is now grappling with how to embed the technology into core operations. Deutsche Bank Research estimates the tokenized real‑world‑asset market at roughly $33 billion, while institutions such as the New York Stock Exchange experiment with 24/7 trading and asset managers tokenise multi‑billion‑dollar funds. This rapid commercialization forces banks to choose a blockchain rail that will underpin settlement, custody and compliance processes for years to come, making the architecture decision a strategic inflection point.

Private consortia offer familiar vendor‑managed environments, but they also introduce lock‑in, concentration risk and slower innovation cycles. Public, permissionless networks, by contrast, deliver native interoperability—any bank can transact with any other without bilateral middleware—cutting the average 6.49 % cross‑border payment cost highlighted by the World Bank. Distributed validator models spread operational risk, addressing the Dallas Fed’s warning about single‑point technology vulnerabilities. Moreover, open ledgers provide regulators with real‑time auditability, a feature praised by the BIS for enhancing compliance oversight. The open‑source ethos further accelerates upgrades, allowing banks to adapt at business speed rather than waiting for vendor roadmaps.

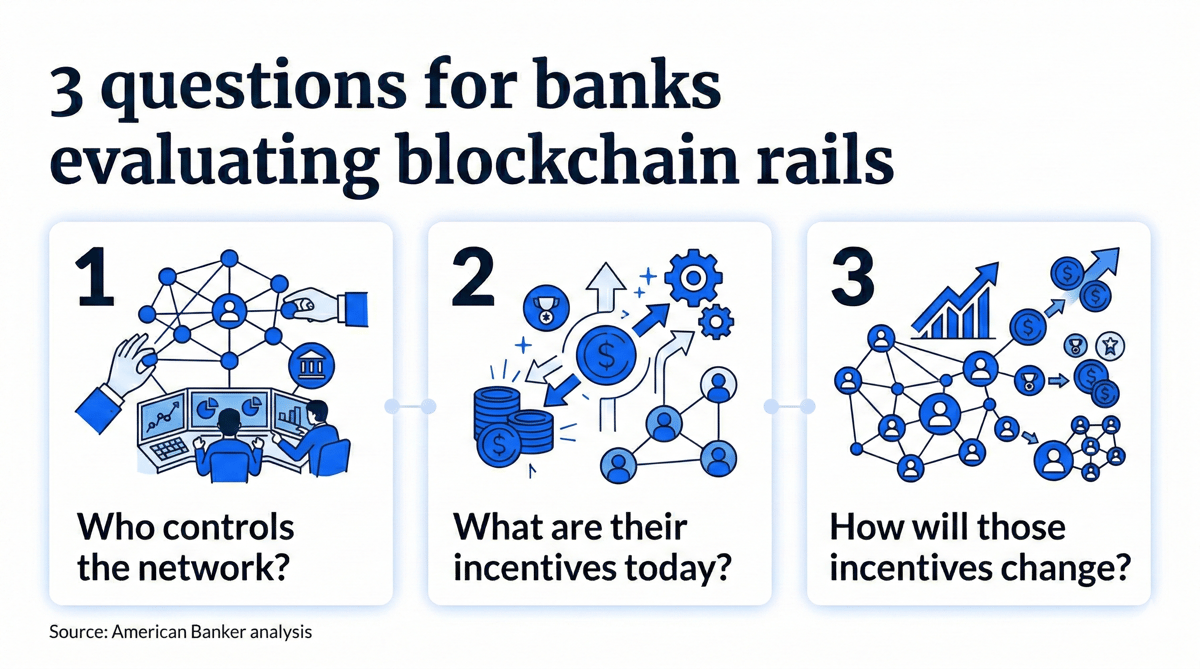

The article distills the evaluation into three questions: who controls the network, what incentives drive that controller today, and how those incentives will evolve as adoption scales. Answers that favor open, decentralized governance signal lower fees, reduced systemic risk and a more agile compliance framework. Conversely, proprietary rails may appear attractive for short‑term control but embed costly migration hurdles. Banks that align their blockchain strategy with these criteria can capture the efficiency gains of tokenized assets while safeguarding against the lock‑in dynamics that have historically eroded margins in core banking technology.

Banks need to choose carefully between public and private blockchains

0

Comments

Want to join the conversation?

Loading comments...