Brazen Scheme Combines Fraud, Visiting Customers' Homes

•January 20, 2026

0

Companies Mentioned

Why It Matters

The scheme exposes a critical gap in consumer awareness and increases banks’ exposure to costly debit‑card disputes, while underscoring the stronger liability protections offered by credit cards.

Key Takeaways

- •Fraudsters use fake ID to dispatch couriers for debit cards

- •Debit‑card liability can rise to $500 after two days

- •“Unauthorized” transfers exclude consumer‑initiated scam payments

- •Card‑cracking targets users under 25 via social media

- •Credit cards offer lower liability and zero‑loss protection

Pulse Analysis

The latest alert from Barnegat Township Police details a hybrid scam that blends phone spoofing with a physical courier pickup. Criminals masquerade as bank fraud agents, claim out‑of‑state activity, and schedule a courier to retrieve the victim’s debit card. Once in hand, the card is used for unauthorized withdrawals or to fund “card‑cracking” operations. This tactic sidesteps the digital‑only fraud vectors that many banks have fortified, exposing a gap in consumer awareness and prompting banks to reinforce education on legitimate communication channels.

Regulation E governs debit‑card transactions, limiting consumer liability to $50 if the loss is reported within two business days, but it can jump to $500 after that and become unlimited after 60 days. In contrast, Regulation Z caps credit‑card liability at $50, with most issuers offering zero‑loss guarantees. Courts have drawn a sharp line between “unauthorized” transfers and consumer‑initiated scam payments, as illustrated by the 2023 Wilkins v. Navy Federal decision. Risk officers must therefore focus on rapid dispute resolution and clear communication to keep liability exposure low.

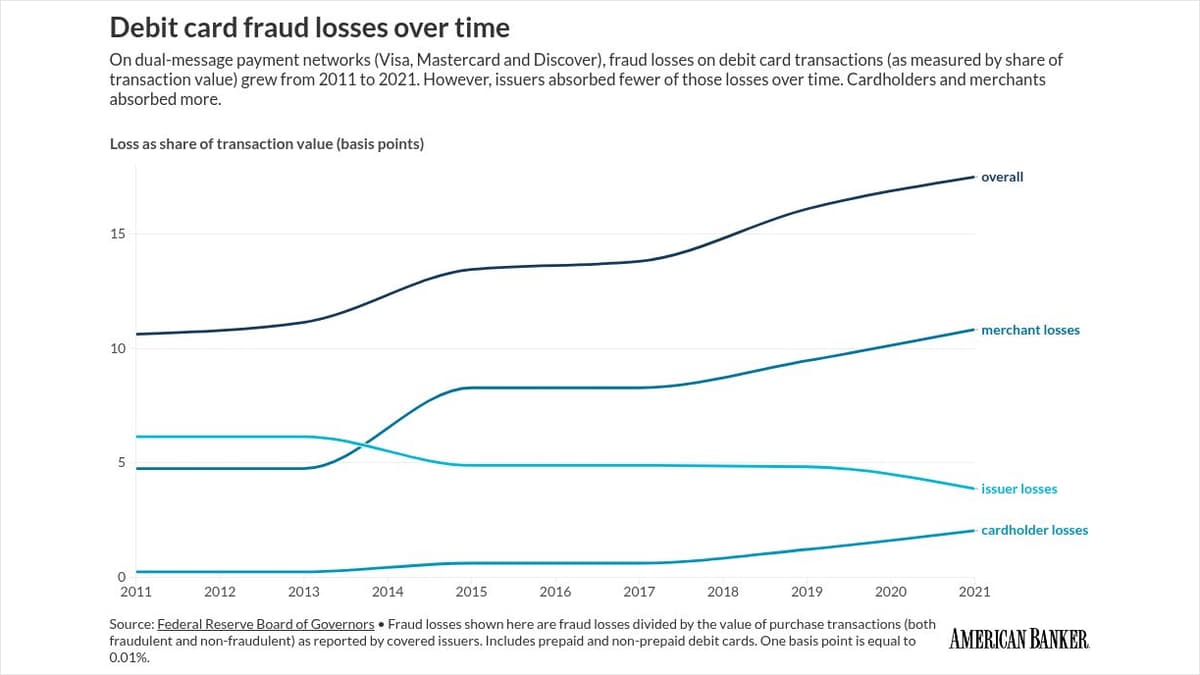

Beyond impersonation, the rise of “card‑cracking” shows how fraudsters exploit social‑media platforms to lure younger account holders into sharing debit credentials for bogus mobile‑deposit schemes. Federal Reserve data indicate that while overall debit‑card fraud rates have risen, network‑level loss percentages are falling, shifting the burden to banks and consumers. Consumer advocates therefore recommend using credit cards for online purchases, where liability protections are stronger. Banks can mitigate risk by deploying real‑time alerts, reinforcing verification steps, and promoting credit‑card usage for e‑commerce, thereby reducing exposure to costly debit‑card disputes.

Brazen scheme combines fraud, visiting customers' homes

0

Comments

Want to join the conversation?

Loading comments...