COVID Loan Program Leaves some Borrowers in a Bind

•February 9, 2026

0

Why It Matters

The fallout reveals how inflexible emergency credit can exacerbate business distress, prompting calls for more adaptable relief mechanisms and congressional oversight.

Key Takeaways

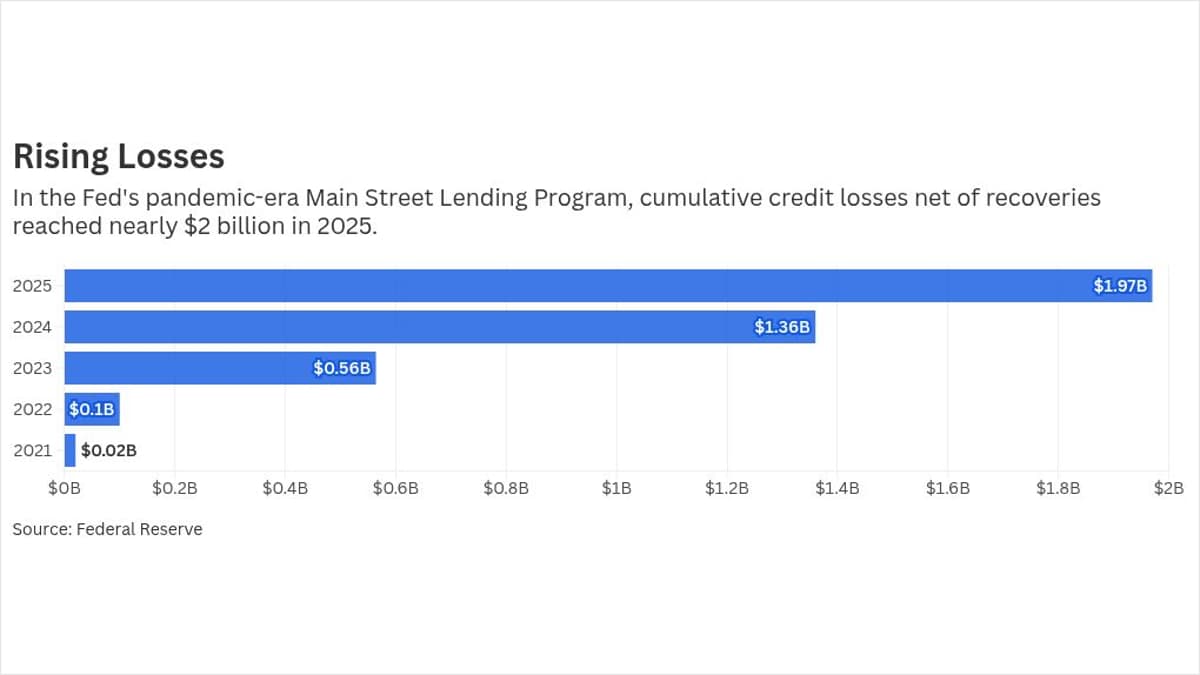

- •$43.9M remains from $17.5B loaned

- •Net losses hit $1.97B by 2023

- •70% balloon payment triggers bankruptcies

- •Fed cannot broadly modify loan terms

- •Borrowers forced to liquidate assets

Pulse Analysis

The Main Street Loan Program was the Federal Reserve’s flagship response to the pandemic’s credit crunch for firms too large for the Paycheck Protection Program. With a $600 billion lending capacity, it ultimately originated just 1,830 loans before halting new issuances in early 2021. While most borrowers repaid, the program’s design—95 % Fed‑backed loans, a five‑year term, and a mandatory 70 % balloon payment—created a high‑stakes payoff structure that many mid‑market companies could not meet once the economy shifted.

For borrowers like Paw.com and unnamed firms, the inability to secure extensions or restructure debt proved catastrophic. The Fed’s statutory prohibition on principal forgiveness and its limited case‑by‑case modifications left companies with no viable path to refinance, forcing asset sales, workforce cuts, or outright bankruptcy. These outcomes underscore a broader tension: emergency credit can stabilize firms in the short term but, without flexible terms, may later accelerate failures when economic conditions evolve.

The program’s demise raises policy questions about future crisis lending. Legislators and regulators must balance fiscal prudence with mechanisms that allow loan terms to adapt to borrowers’ changing cash flows. Introducing conditional forgiveness clauses, staggered balloon payments, or clearer pathways for private‑sector refinancing could mitigate the adverse side effects witnessed in Main Street. As the Fed winds down the portfolio, the experience serves as a cautionary tale for designing resilient, borrower‑friendly support structures in any future economic shock.

COVID loan program leaves some borrowers in a bind

0

Comments

Want to join the conversation?

Loading comments...