Monzo and Fair4All Finance Tackle UK Credit Exclusion

Companies Mentioned

Why It Matters

The pilot tackles a growing credit‑exclusion gap, offering a scalable, low‑risk pathway for underserved consumers to build credit histories and for mainstream banks to meet inclusion mandates.

Key Takeaways

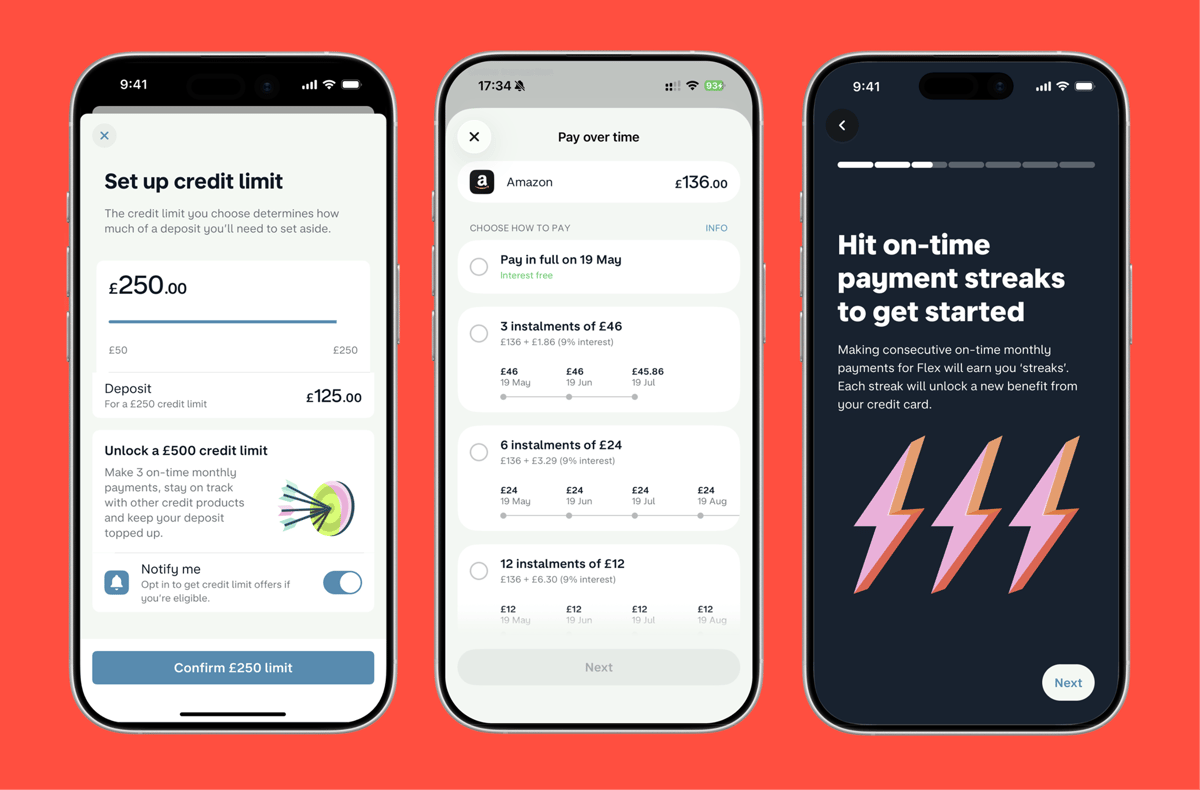

- •Pilot offers up to £250 credit with refundable deposit.

- •Fair4All backs £7 million guarantee, sharing risk with Monzo.

- •Successful borrowers can double limit to £500 and reclaim deposit.

- •0% interest for full‑month payoffs; 39% APR for installments.

- •Program aligns with UK Financial Inclusion Strategy, may influence regulators.

Pulse Analysis

Credit exclusion in the UK has surged, with roughly 30% more adults unable to access mainstream loans since 2018. Monzo’s Flex Build, now enhanced with a deposit‑backed credit line, directly addresses this gap by providing a low‑cost entry point for borrowers who lack traditional credit histories. The partnership with Fair4All Finance adds a £7 million (≈$8.9 million) guarantee, mitigating risk for the bank while expanding the pool of eligible customers. By capping the initial limit at £250 (≈$318) and allowing repayment terms up to two years, the model encourages responsible borrowing and offers a clear pathway to higher limits and mainstream credit.

The risk‑sharing structure dovetails with the UK Government’s Financial Inclusion Strategy, which seeks to broaden access to small‑sum lending. Unlike many high‑interest payday products, the pilot charges 0% interest for full‑month repayments and only applies a 39% APR for extended balances, with no early‑payment penalties. This mirrors practices of several large US banks that have rolled out similar deposit‑backed credit products at scale, suggesting a viable template for the UK market. Moreover, the built‑in grace period before any credit‑score impact provides a safety net that could improve repayment behavior and reduce default rates.

If successful, the pilot could set a precedent for other fintechs and traditional banks to adopt deposit‑secured credit lines, reshaping the landscape of small‑sum lending. The data collected will be shared with regulators, potentially informing new guidelines that balance consumer protection with financial inclusion. For consumers, the ability to build a repayment track record without prohibitive costs could unlock broader financial opportunities, from mortgages to business financing, ultimately strengthening household resilience across the UK economy.

Monzo and Fair4All Finance tackle UK credit exclusion

Comments

Want to join the conversation?

Loading comments...