Overdraft Fee Income Is on the Rise at These Big Banks

•January 6, 2026

0

Companies Mentioned

Why It Matters

Rising overdraft fees signal renewed profit streams for banks but also raise consumer‑protection concerns as vulnerable households face higher costs. The trend underscores how regulatory shifts can quickly reshape non‑interest income strategies.

Key Takeaways

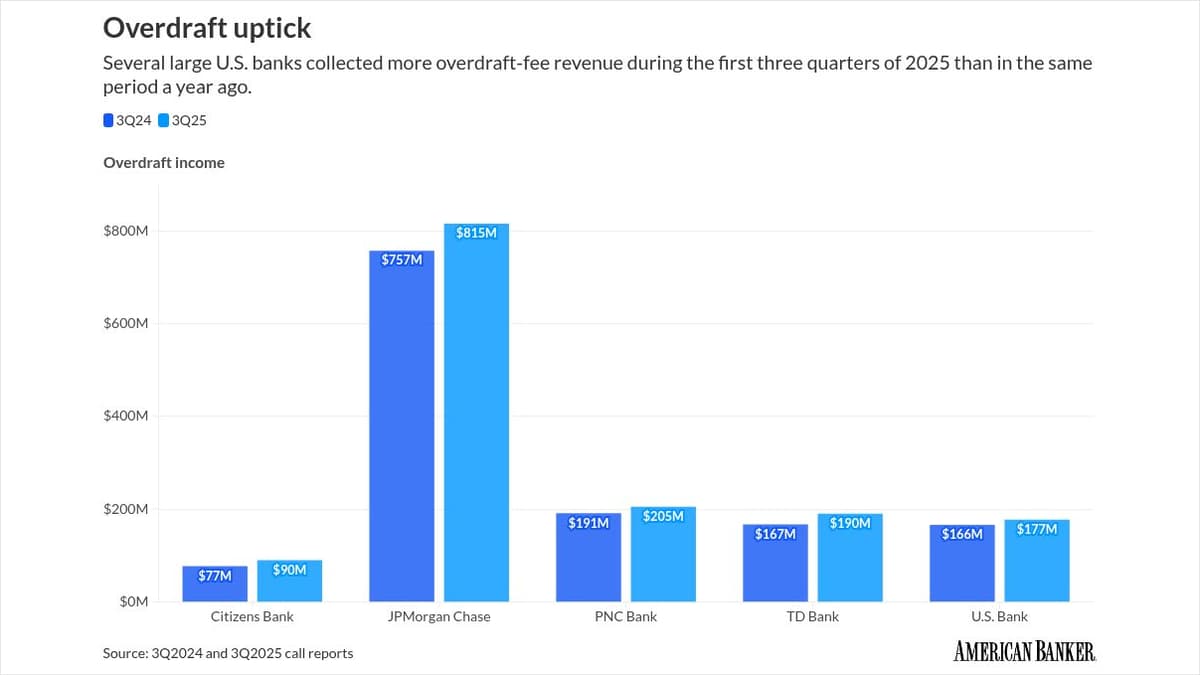

- •JPMorgan overdraft revenue up 7.66% YoY Q3 2025.

- •Citizens Bank overdraft revenue up 16.9% YoY.

- •Overdraft income still far below 2019 levels.

- •Deregulation may enable banks to adjust overdraft practices.

- •Advocates warn vulnerable customers of rising fees.

Pulse Analysis

The resurgence of overdraft‑related income reflects a broader rollback of the consumer‑focused reforms introduced after 2022. When the Biden administration pushed the CFPB to cap fees at $5, banks prepared for a steep revenue decline. Although Congress overturned that rule, the regulatory vacuum has allowed institutions to revert to legacy pricing models, albeit modestly, as they test the market’s tolerance for higher non‑interest earnings.

Data from call reports show that JPMorgan Chase generated $815 million in overdraft revenue through September 2025, a $58 million increase from the prior year, while Citizens Financial posted a 16.9% jump. These gains are not solely policy‑driven; inflation‑pressured consumers are more likely to overdraw accounts, and banks report expanding customer bases. Yet the absolute figures remain a fraction of the pre‑reform peaks of 2019, indicating that the industry’s fee‑reduction legacy still tempers overall earnings.

For policymakers and consumer advocates, the uptick raises red flags about the durability of recent protections. Without an active CFPB, banks could incrementally raise fees or reintroduce structures that trap low‑income users. Stakeholders are watching for signs of systematic fee escalation, which could prompt renewed legislative action or state‑level interventions. Meanwhile, banks that have eliminated overdraft charges entirely, such as Capital One, illustrate a divergent strategy that may become a competitive differentiator in a market increasingly sensitive to fee transparency.

Overdraft fee income is on the rise at these big banks

0

Comments

Want to join the conversation?

Loading comments...