War Revives Stagflation Dangers for Global Economy

Why It Matters

Stagflation forces policymakers to choose between tightening monetary policy and risking recession, reshaping investment strategies worldwide. The conflict’s ripple effects could strain emerging markets and alter global supply‑chain dynamics.

Key Takeaways

- •Seven weeks of Middle East war depresses global growth forecasts

- •Inflation pressures rise as supply chains face energy disruptions

- •PMI surveys show simultaneous slowdown and price hikes in month two

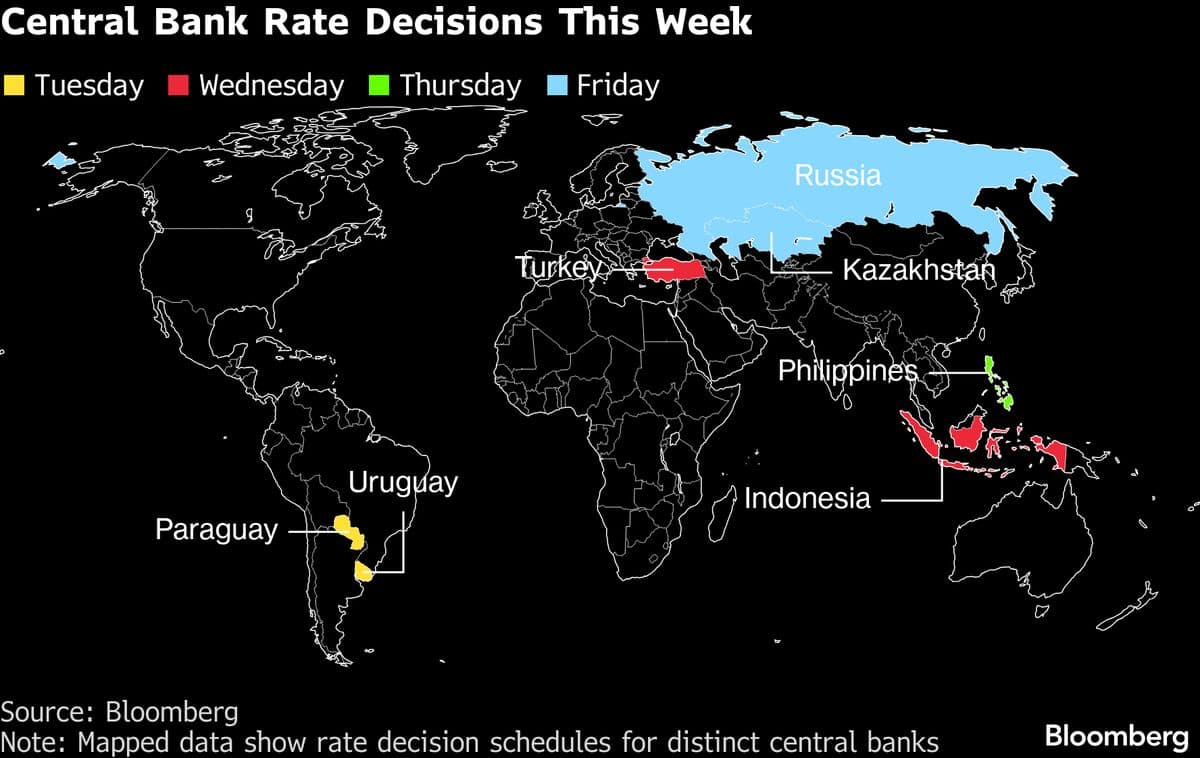

- •Central banks face dilemma balancing rate hikes against recession risks

- •Emerging markets most vulnerable to stagflation from conflict fallout

Pulse Analysis

Stagflation—simultaneous stagnation and inflation—has been a rare economic nightmare, last seen in the 1970s. The current Middle East conflict revives those fears by choking energy supplies, driving up commodity prices, and dampening consumer confidence. While the war’s direct damage is localized, its indirect effects ripple through global trade routes, pushing input costs higher for manufacturers and retailers alike. This environment mirrors past periods when central banks struggled to calibrate policy, as tightening rates risked deepening a slowdown, while easing could cement inflation expectations.

Early purchasing‑manager index (PMI) readings from the first two months of the conflict reveal a clear pattern: production indices are slipping while price‑new‑order components climb. Such a divergence signals that firms are grappling with tighter margins, passing higher costs onto customers even as demand wanes. Energy‑intensive sectors—transport, chemicals, and heavy industry—are especially exposed, given the region’s pivotal role in oil and gas markets. The upcoming wave of business surveys across Europe, Asia, and the Americas will likely confirm a broad-based drag on GDP growth, compounding the inflationary shock.

Policymakers now face a classic stagflation dilemma. Major central banks, including the Fed and ECB, must decide whether to raise rates to curb price pressures, risking a sharper recession, or to pause tightening and risk entrenching inflation. Emerging markets, already burdened by debt and weaker fiscal buffers, are particularly susceptible to capital outflows and currency depreciation. Investors should monitor sovereign bond spreads, commodity price trends, and real‑time PMI data to gauge the trajectory of this renewed stagflation risk. The war’s duration and any escalation will be decisive factors in shaping the global economic outlook for the next 12‑18 months.

War Revives Stagflation Dangers for Global Economy

Comments

Want to join the conversation?

Loading comments...