Hedge Funds Are Bearish on Natural Gas for First Time Since 2024

Why It Matters

A bearish stance could depress natural‑gas prices, tightening margins for producers and utilities while reshaping investment strategies. It also signals a market reassessment of U.S. gas demand amid a transitioning energy mix.

Key Takeaways

- •Hedge funds net‑short 11,316 Henry Hub contracts

- •First bearish position on U.S. gas since 2024

- •Shift driven by abundant domestic supply expectations

- •Anticipated decline in export demand pressures prices

- •Potential ripple effect on energy stocks and utilities

Pulse Analysis

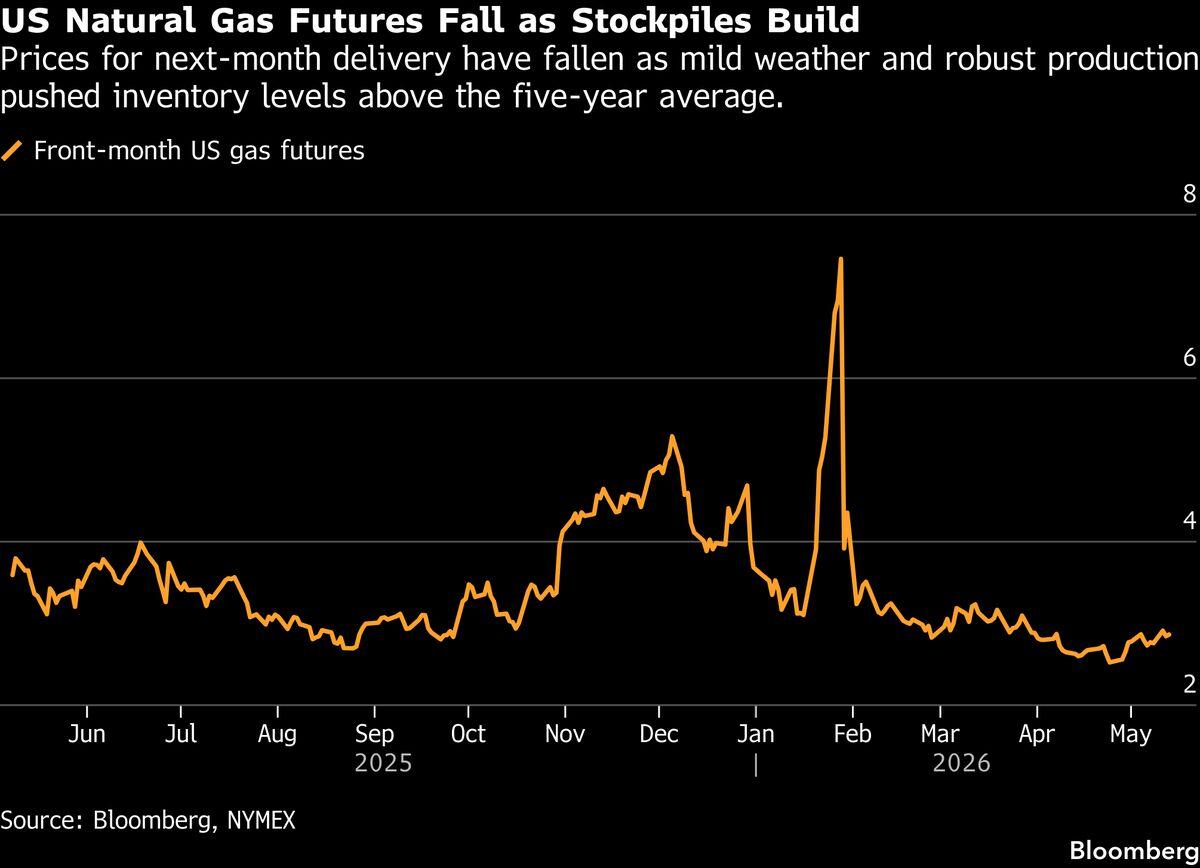

The U.S. natural‑gas market has entered a period of surplus, driven by record‑high production from shale plays and robust storage levels that exceed seasonal averages. Domestic output has outpaced demand growth, while the anticipated slowdown in liquefied natural‑gas (LNG) exports—due to slower global economic activity and competition from alternative fuels—has further eased upward pressure on prices. This backdrop creates a classic supply‑glut scenario, prompting market participants to reevaluate forward curves and inventory strategies.

Against this macro environment, hedge funds have signaled a decisive shift in sentiment. CFTC data shows a net‑short of 11,316 contracts across the Henry Hub benchmark, a reversal from a net‑long of 15,270 just a week earlier. Such a swing is rare; the last comparable bearish positioning occurred in 2024. Traders are likely pricing in a near‑term price decline, betting that the market will correct as storage fills and export pipelines operate below capacity. The net‑short also reflects a broader risk‑off posture, as investors diversify into equities and other commodities perceived as offering better returns amid volatile energy prices.

The implications extend beyond futures desks. Lower natural‑gas prices can compress profit margins for upstream producers, potentially delaying new drilling projects and affecting capital‑intensive infrastructure investments. Utilities may benefit from cheaper fuel costs, but could also see reduced revenue if price‑linked contracts are renegotiated. For equity investors, energy stocks tied to gas production may face headwinds, while renewable‑energy firms could gain relative appeal. Monitoring storage data, LNG contract negotiations, and policy shifts on carbon pricing will be critical for forecasting the next phase of the U.S. gas market.

Hedge Funds Are Bearish on Natural Gas for First Time Since 2024

Comments

Want to join the conversation?

Loading comments...