Achmea Targets €75m Windmill III Re 2026-1 Cat Bond for More Windstorm Reinsurance

Achmea Reinsurance Company is targeting a €75 million (≈ $81 million) Windmill III Re 2026‑1 catastrophe bond, marking its fifth cat‑bond issuance and the first to stagger maturity alongside the 2024 deal. The single‑tranche Class A notes will provide a four‑year layer of collateralized reinsurance, attaching at $540 million and exhausting at $702 million of loss. Pricing guidance sits between 4.25% and 5% spread, reflecting a softer market compared with the 2024 bond’s 5.25% rate. The move deepens Achmea’s capital‑market‑backed protection for European windstorm and severe convective risks.

SEADRIF and FAO Launch First Parametric Drought Insurance Pilot in Lao PDR

SEADRIF Insurance Company and the UN Food and Agriculture Organization have launched Southeast Asia’s first parametric drought insurance pilot in Lao PDR. The scheme links the Combined Drought Index to pre‑arranged payouts for the Ministry of Finance, enabling funds to...

Verisk Launches Updated U.S. Tropical Cyclone Model via Its New Synergy Studio Platform

Verisk announced an updated U.S. Tropical Cyclone Model delivered through its new cloud‑native Synergy Studio platform, available from June 15, 2026. The model incorporates a near‑present climate view, an expanded stochastic event catalog, and a peer‑reviewed wind‑field methodology. Enhanced hazard...

Swiss Re Names Martin Zingg to Lead Alternative Capital Partners (ACP) as Minter to Retire

Swiss Re has appointed long‑time senior executive Martin Zingg as head of its Alternative Capital Partners (ACP) division, succeeding Chris Minter who will retire after nearly 13 years. Zingg, currently Group Head of Corporate Development and Strategic Investments, will assume...

The Hanover Raises Target 50% to $150m for Its Fourth Commonwealth Re Cat Bond

The Hanover Insurance Group has increased the size of its fourth catastrophe bond, Commonwealth Re Series 2026-1, by 50% to $150 million. The fully‑collateralized, multi‑peril bond will protect against US named storms, earthquakes, severe thunderstorms, winter storms and wildfires from July 2026...

Heritage Gets “Substantial Cost Savings” As It Renews $2.2bn of Reinsurance and Cat Bond Limit

Heritage Insurance Holdings renewed its 2026 reinsurance and catastrophe‑bond program with a total limit of $2.2 billion, down from the $2.5 billion placed in 2025. The renewal includes $712 million of multi‑year coverage, $550 million from cat bonds and $162 million from private markets. Pricing...

Jamaica Govt Praise Investor Support for New Cat Bond, Plan Parametric CCRIF Cover Expansion

Jamaica’s government announced the successful issuance of a $200 million catastrophe bond, the third of its kind, which was upsized by one‑third and attracted 25 global investors. The bond, facilitated by the World Bank and financially supported by Singapore’s Monetary Authority,...

Florida Renewal Risk-Adjusted Pricing Down 15% to 20% Across Many Layers: Guy Carpenter

Guy Carpenter reported that Florida property catastrophe reinsurance pricing dropped 15% to 20% across multiple layers at the June 1 renewals. The decline reflects stronger market fundamentals, including robust reinsurer balance sheets, heightened investor appetite, and recent legal reforms that...

Buckle and Subsidiary Gateway Sue China Construction Bank over Vesttoo LOC Fraud

Fronting specialist Buckle and its carrier Gateway have filed a lawsuit in Illinois against China Construction Bank (CCB), alleging the bank issued nine forged letters of credit worth nearly $9.8 million. The complaint also seeks an additional $3.3 million for consequential damages...

RenRe Saw Stronger Reinsurance Demand Ahead of Mid-Year Renewals, CUO Marra

RenaissanceRe reported a 209% jump in fee income from its joint‑venture and ILS platforms in Q1 2026, while Chief Underwriting Officer David Marra said demand for U.S. mid‑year reinsurance renewals is outpacing the firm’s original forecast. The company has already...

LGT Reinsurer Lumen Re Maintains Its Lower Loss Ratio, Premiums Written Increasing

Lumen Re, the Bermuda‑based reinsurer for LGT ILS Partners, posted a 23% jump in gross premiums to nearly $207 million in 2024 and saw net premiums rise to $77.1 million. AM Best reaffirmed its Class 3B status in 37 US states for 2026, noting...

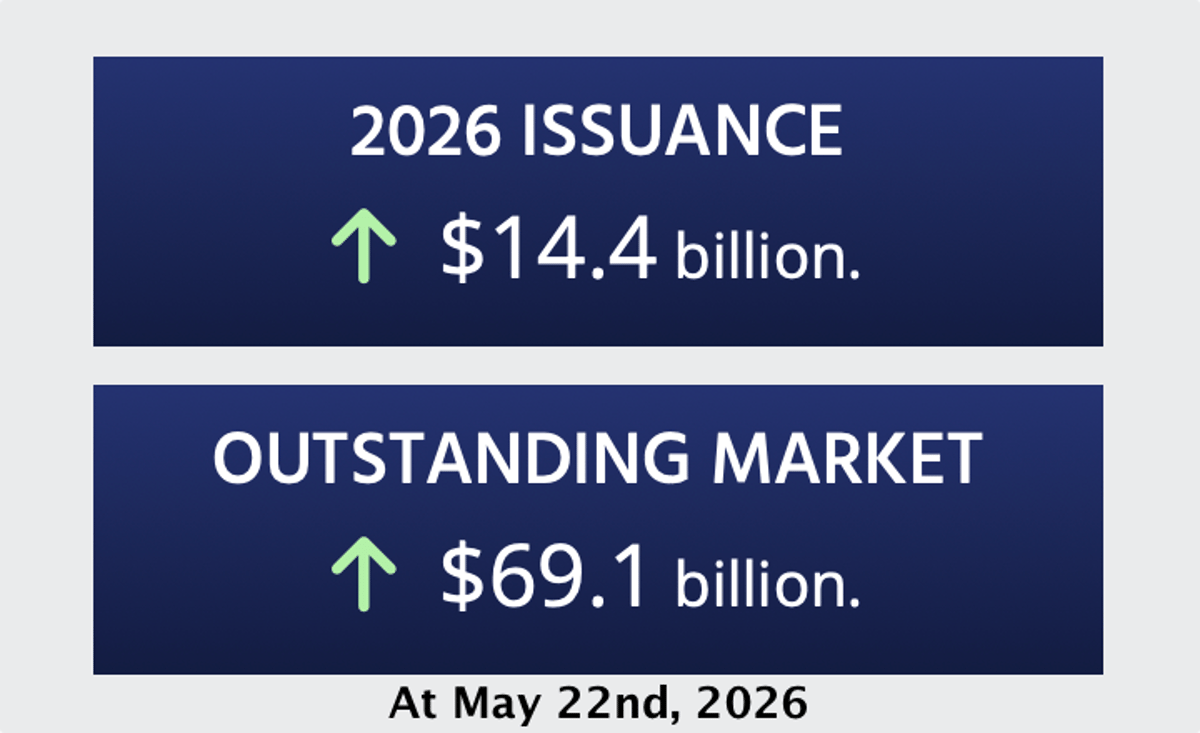

Catastrophe Bond Issuance in H1 2026 Now Projected at $16.3bn, Could Rise Further

Catastrophe bond issuance in the first half of 2026 is projected to reach $16.3 bn, up from the $14.4 bn already settled. The market has seen 60 completed transactions and a pipeline of 12 more, with property cat bonds accounting for $13.72 bn...

Massachusetts MPIUA Returns for $150m Mayflower Re 2026 Catastrophe Bond

The Massachusetts Property Insurance Underwriting Association (MPIUA) is re‑entering the catastrophe‑bond market with a new Mayflower Re Ltd. Series 2026‑1 issuance targeting at least $150 million of multi‑peril aggregate reinsurance. The deal will consist of two $75 million tranches, Class A and Class B, backed...

Allstate Secures $200m of Florida Reinsurance with Sanders Re III 2026-2 Cat Bond

Allstate has finalized a $200 million catastrophe bond issued by Sanders Re III Ltd. (Series 2026‑2) to obtain four‑year fully collateralized reinsurance for Florida. The bond, priced at the low end of guidance with a 4% risk‑interest spread, replaces an earlier...

State Farm Gets $1.5bn of Reinsurance with Merna Re Enterprise 2026-1 Catastrophe Bond

State Farm has returned to the catastrophe‑bond market, closing a $1.5 billion private issuance through Merna Re Enterprise Ltd.’s Series 2026‑1. The deal consists of two $750 million tranches, Class A at a 6.25% spread and Class B at 9.25%, providing fully collateralized reinsurance through...