QSBS Eligibility Checklist: Does Your Stock Qualify Under Section 1202?

The article provides a step‑by‑step checklist to determine whether a stock qualifies as Qualified Small Business Stock (QSBS) under IRC Section 1202. It outlines eight eligibility criteria—including C‑corporation status, a $75 million gross‑asset ceiling at issuance, direct original issuance, an active‑business test, and a five‑year holding period—that together unlock up to $15 million of tax‑free capital gains. The guide also highlights documentation needs and the impact of recent federal and Washington state tax reforms. Entrepreneurs and investors can use the checklist to avoid costly disqualification before a sale.

Oregon QSBS Decoupling Is Law: What Kotek's Signing Letter — and the Referendum — Mean for Founders

Governor Tina Kotek signed Senate Bill 1507 on April 9, 2026, officially decoupling Oregon from the federal qualified small‑business stock (QSBS) exclusion and applying the change retroactively to Jan 1, 2026. The move means Oregon residents must pay state tax on gains that remain...

The 183-Day Rule and Safe-Harbor Day-Counting for Washington Taxpayers

The article explains Washington’s emerging 183‑day statutory residency rule and how it interacts with domicile analysis for founders leaving the state. It details how states define a “day,” the pitfalls of permanent places of abode, and why merely staying under...

Trust Planning for Washington High Earners: ING, NING, and DING Trusts Under ESSB 6346

Washington will launch a state income tax on residents whose AGI exceeds $1 million in 2028. High‑earning Washingtoners can use non‑grantor trusts—often called ING, NING, or DING—sited in Nevada, South Dakota, or Delaware to shift portfolio and passive investment income out...

QSBS and Washington Residency: Timing Section 1202, the Sale, and the Move

Washington founders face a narrow 20‑month window before ESSB 6346 takes effect, during which federal Section 1202 qualified small business stock (QSBS) treatment, Washington’s 7% capital gains tax, and the new 9.9% income tax intersect. The article outlines four levers—QSBS...

The Marriage Penalty in ESSB 6346: Why Two Unmarried Washington Earners Can Save $40,000 a Year

Washington's ESSB 6346 imposes a 9.9% tax on household income exceeding $1 million, creating a built‑in marriage penalty for dual‑high‑earner couples. A pair earning $700,000 each would pay roughly $39,600 annually, or nearly $600,000 over a 15‑year career, solely because they...

What Counts as Washington Taxable Income Under ESSB 6346?

Washington’s new income tax under ESSB 6346 uses federal adjusted gross income as its starting point, then applies state‑specific additions, subtractions, and structural adjustments. After these modifications, a $1 million household standard deduction is allowed and the remaining amount is taxed at...

Washington’s Capital Gains Tax Charitable Deduction Has a Hidden Catch

Washington’s capital gains tax offers a charitable deduction, but it only applies when the donation is made to a “qualified organization” that is principally directed and managed within the state. The rule diverges from federal law, which merely requires 501(c)(3)...

The Alternative Minimum Tax and Stock Options: A Complete Guide for Washington Startup Employees

The guide explains how the federal Alternative Minimum Tax (AMT) hits incentive stock options (ISOs) and how Washington’s new tax regime reshapes planning. The 2026 One Big Beautiful Bill Act raises the AMT exemption to $90,100 for singles and $140,200...

RSUs and Washington State's New Taxes: What Seattle Tech Employees Need to Know

Washington’s new tax regime adds a 7‑9.9% capital‑gains levy (effective 2025) and a 9.9% broad‑based income tax (effective 2028) that together reshape the cost of restricted stock units for Seattle tech workers. RSU vesting is ordinary income, so any vesting...

Convertible Notes Vs. SAFEs: A Startup Lawyer’s Guide to Choosing the Right Instrument

A seasoned startup lawyer breaks down the differences between SAFEs and convertible notes, highlighting that SAFEs are equity‑like, interest‑free contracts while convertible notes are debt instruments with interest and maturity dates. The guide details legal costs, balance‑sheet impact, speed to...

Section 1045 Rollovers: How to Defer QSBS Gains When You Sell Too Early

Section 1045 permits owners of Qualified Small Business Stock (QSBS) to defer capital gains by reinvesting sale proceeds into new QSBS within 60 days. The rollover treats the original gain as unrecognized, reducing the basis of the replacement shares, while...

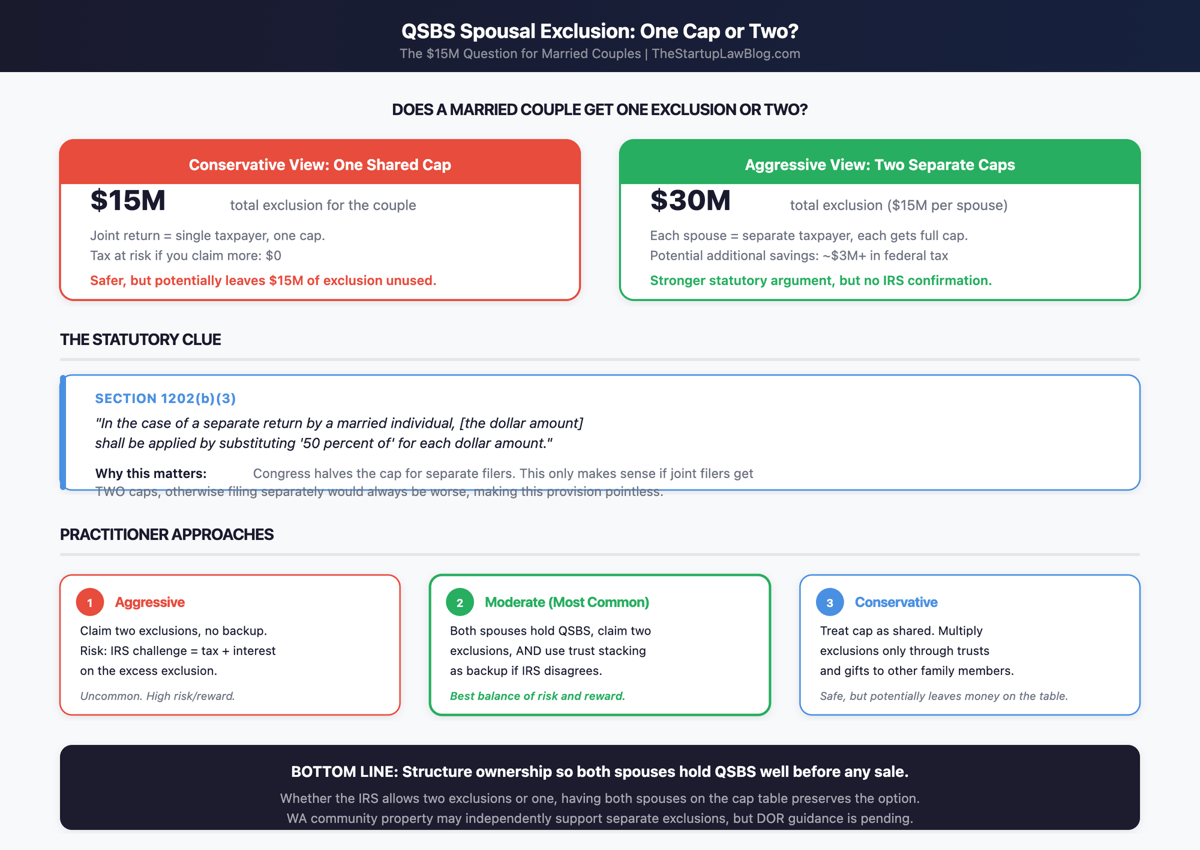

Can Both Spouses Claim the QSBS Exclusion? What Section 1202 Does and Doesn't Say About Married Couples

Section 1202 lets a taxpayer exclude up to $15 million of qualified small‑business stock (QSBS) gains, but the law is silent on whether a married couple filing jointly receives one $15 million cap or two. The statute only specifies that married filing separately...

How to Negotiate Startup Equity: A Practical Guide for Employees

The Startup Law Blog’s new guide walks employees through every facet of a startup equity offer, from decoding share counts and percentage ownership to understanding 409A valuations and option types. It outlines how to benchmark grants by role and financing...

Restricted Stock Vs. Stock Options: Which Is Better for Startup Equity?

Startup equity compensation typically comes in two forms: restricted stock awards and stock options. Restricted stock grants actual shares at grant and, with an 83(b) election, locks in tax on the low initial value, turning future gains into capital gains....

Double-Trigger Acceleration: What Every Startup Founder and Employee Needs to Know

Double‑trigger acceleration is a provision that only vests unvested startup equity when two events occur: a change of control and the employee’s involuntary termination. It has become the market standard because it balances employee protection with acquirers’ need to retain...

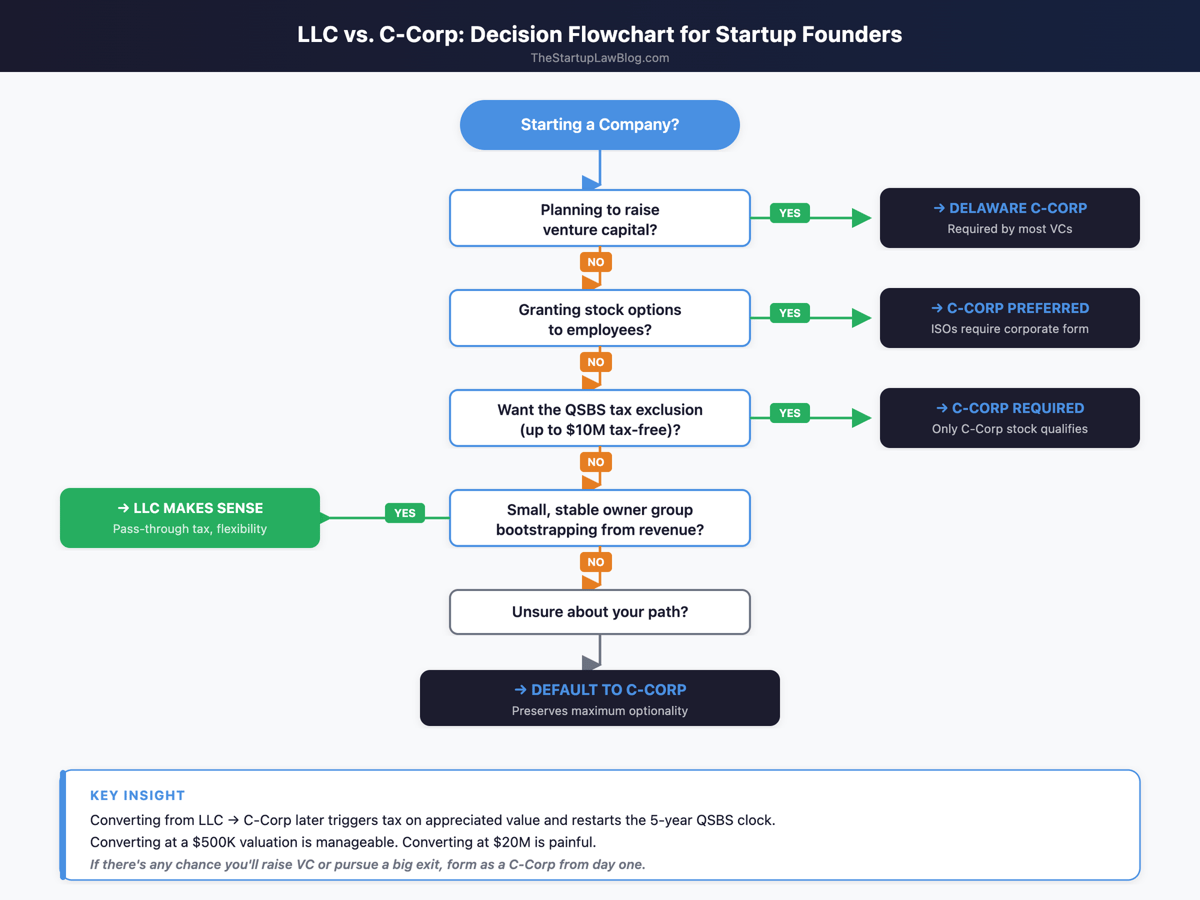

LLC Vs. C-Corp for Startups: How to Choose the Right Entity

The guide breaks down the practical trade‑offs between forming an LLC and a Delaware C‑Corporation for startups. It explains how entity choice affects fundraising mechanics, equity compensation, tax treatment, and long‑term exit strategies such as the QSBS exclusion. Real‑world examples...

Priced Equity Rounds: A Founder's Complete Guide to Series Seed, Series A, and Beyond

A priced equity round converts SAFEs and notes into actual preferred shares at a negotiated pre‑money valuation, establishing the company’s capital structure from Series Seed through IPO. The term sheet outlines four critical levers—valuation and option‑pool sizing, liquidation preferences, board...

Startup Law Glossary: 75+ Terms Every Founder Should Know

The Startup Law Glossary compiles over 75 essential legal and financial terms that founders encounter when building and scaling a company. It explains concepts such as 83(b) elections, 409A valuations, cap tables, and liquidation preferences, providing practical guidance for equity...

Accredited Investor Rules: Who Qualifies, How to Verify, and Why It Matters for Startups

The SEC’s accredited‑investor definition, set out in Regulation D Rule 501(a), hinges on income, net‑worth, or professional licensing thresholds that signal financial sophistication. The 2020 amendment added Series 7, 65 and 82 licenses, spousal‑equivalent income pooling, and knowledgeable‑employee categories, expanding the pool modestly without...

Rule 506(b) Vs. 506(c): Which Reg D Exemption Should Your Startup Use?

Rule 506(b) and Rule 506(c) are the two primary Reg D exemptions for U.S. startup fundraising. 506(b) prohibits general solicitation, allows unlimited accredited investors and up to 35 non‑accredited investors with heavy disclosure, and requires no accreditation verification. 506(c) permits advertising but mandates...

Regulation D Explained: How Startups Raise Capital Without an IPO

Regulation D (Reg D) remains the cornerstone of private capital raising for U.S. startups, allowing companies to bypass costly SEC registration. The three primary exemptions—Rule 504, Rule 506(b), and Rule 506(c)—offer varying limits, investor qualifications, and solicitation rules, with 506(b) serving as the workhorse...

State Tax Comparison for Startup Founders: Where to Incorporate and Where to Live

The guide breaks down how incorporation state and personal residence state affect a founder’s tax bill, emphasizing that residence decisions can swing after‑tax proceeds by millions. It compares Delaware’s standard corporate framework with personal tax regimes in high‑tax states like...

Anti-Dilution Provisions: What Every Startup Founder Needs to Understand Before Their Series A

Anti‑dilution clauses, a staple of Series A term sheets, adjust investors' conversion price when a startup raises a later round at a lower valuation. The two primary mechanisms—full‑ratchet and weighted‑average—have dramatically different dilution effects on founders and employees. Full‑ratchet can slash...

Washington's New Income Tax: The Complete Guide for Founders, Investors, and High Earners

Governor Ferguson signed ESSB 6346 on March 30, 2026, establishing Washington’s first broad‑based income tax—a 9.9% levy on adjusted gross income exceeding $1 million, effective January 1, 2028. The law reshapes tax planning for founders, investors, executives, and high‑earning residents, introducing residency rules, a marriage...

The Complete Guide to Qualified Small Business Stock (QSBS): Section 1202 Explained

Section 1202 of the Internal Revenue Code lets founders and early investors exclude up to $15 million of capital gains when they sell qualified small business stock (QSBS) after a five‑year hold. The One Big Beautiful Bill Act (OBBBA) enacted in July 2025 raised the...

Cap Table Management: The Founder's Guide to Getting It Right From Day One

The article is a founder‑focused guide that treats the cap table as the core legal document of a startup, detailing what must be recorded—from common and preferred stock to options, SAFEs, convertible notes, warrants, and advisor equity. It stresses the...

Equity Compensation Plan Design: How to Structure Your Startup's Stock Option Plan

Startup founders often mishandle equity compensation, either making plans too restrictive or overly generous, which can hurt talent attraction and founder ownership. A well‑crafted equity incentive plan defines the option pool—typically 10‑20% of fully diluted shares—sets clear vesting schedules, and...

Will Washington's Income Tax Rate Go Up? (History Says Yes)

Washington’s new income tax imposes a 9.9% rate on household earnings above $1 million, marking the state’s first foray into personal taxation. Historical evidence shows that every state which has introduced an income tax eventually raises the rate, lowers the threshold,...

Estate Planning Before 2028: How Washington's Income Tax Changes the Calculus

Washington will impose a 9.9% income tax on earnings above $1 million starting Jan 1 2028, adding a second layer to its already aggressive estate tax regime. The combined effect creates a double‑tax problem for high‑net‑worth residents, making the pre‑2028 window the most...

Washington Income Tax: What Happens If You Move Mid-Year?

Washington’s new income tax includes a part‑year residency provision that prorates both the tax base and the $1 million standard deduction based on days of residency. Under §406, taxpayers only owe tax on income earned while a Washington resident, with the...

How to Make Estimated Tax Payments Under Washington's New Income Tax

Washington’s new 9.9% income tax, effective Jan 1 2028, will require estimated quarterly payments for taxpayers with income above $1 million. The Department of Revenue has not yet issued detailed rules, but the statute mirrors the federal model, likely adopting similar payment dates...

Charitable Giving Strategies to Reduce Your Washington Income Tax

Washington’s new 9.9% income tax introduces a charitable deduction under §309, limited to $100,000 per year, which can shave up to $9,900 off a taxpayer’s liability. The deduction mirrors federal IRC §170 gifts, but its cap means high‑income earners must look...

Is Retirement Income Subject to Washington's 9.9% Income Tax? (Social Security, Pensions, 401(k), IRAs)

Washington’s new 9.9% income tax, effective 2028, treats retirement income like any other earnings, with a $1 million exemption threshold. Social Security benefits are only taxed to the extent they are federally taxable, while Roth withdrawals remain excluded. Traditional IRA, 401(k)...

Washington Vs. California: A Tax Comparison for Founders and Investors

Washington’s new ESSB 6346 law, effective 2028, imposes a 9.9% income tax on household income above $1 million, ending its zero‑tax reputation for high earners. California still taxes all income at a progressive rate topping 13.3%, including wages, capital gains and...

Washington's New Income Tax and Pass-Through Business Income: S-Corps, LLCs, and Partnerships

Washington enacted a 9.9% state income tax (ESSB 6346) that applies to individuals, including income passed through from S‑corporations, LLCs, and partnerships. The law permits pass‑through entities to elect to pay the tax at the entity level, converting the state...

Washington's New Income Tax: The Marriage Penalty Explained

Washington’s new 9.9% state income tax provides a $1 million standard deduction per household, not per individual. Consequently, married or domestic‑partner couples share a single deduction, creating a marriage penalty that can reach $99,000 annually for comparable earners. The penalty also...

Washington's New Income Tax and Remote Workers: Who Owes What?

Washington will launch a 9.9% personal income tax on Jan. 1, 2028, using a dual‑track residency test that hinges on domicile and physical presence. Residents—defined by domicile or a 183‑day presence test—must allocate all income to the state, subject to a...

How Washington's New 9.9% Income Tax Applies to Stock Options and RSUs

Washington’s ESSB 6346 imposes a 9.9% income tax on household earnings above $1 million starting January 1, 2028. The tax is calculated from federal adjusted gross income, meaning equity compensation can push employees over the threshold in a single year. Incentive Stock Options...

Are Real Estate Gains Subject to Washington's New 9.9% Income Tax?

Washington’s newly enacted ESSB 6346 imposes a 9.9% income tax on household income above $1 million, but it expressly excludes gains from the sale of real property. The exclusion covers primary residences, investment rentals, and commercial buildings, stripping those gains from...

Does QSBS Avoid Washington’s New 9.9% Income Tax? (Yes — For Now)

Washington’s ESSB 6346, effective 2028, imposes a 9.9% income tax on household AGI above $1 million. Because Section 1202 excludes qualifying small‑business stock gains from federal gross income, those gains never enter AGI and thus escape the state tax. The article illustrates...

QSBS Stacking: How to Multiply the $15M Exclusion with Trusts and Family Gifts

Qualified Small Business Stock (QSBS) under Section 1202 allows a $15 million exclusion per taxpayer per issuer, but founders can multiply this benefit through "stacking" strategies. By allocating shares to spouses, adult children, and non‑grantor trusts, each party receives its own exclusion,...