Credit for Builders Tightens in the First Quarter, But Only Slightly

Why It Matters

The modest easing signals that financing remains constrained for builders, potentially slowing new home supply, while the rise in one‑time‑close loans reshapes risk allocation between developers and buyers.

Key Takeaways

- •NAHB AD&C net‑easing index at –2.7, closest to zero in four years

- •Fed SLOOS reading –4.9, still negative but within unchanged range

- •Effective rates fell since 2023‑24 peaks despite mixed quarterly moves

- •Construction‑to‑permanent loans used for 35% of single‑family builds

- •Half of homes built financed with one‑time‑close loans to buyers

Pulse Analysis

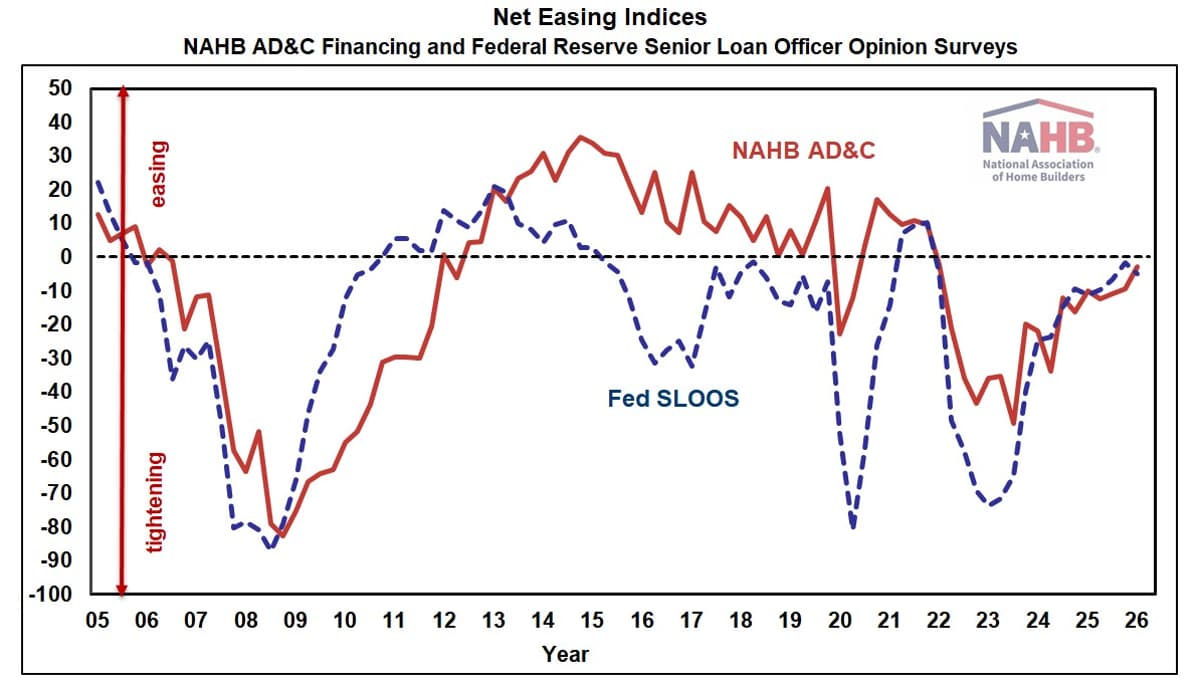

The latest NAHB AD&C financing survey shows credit tightening at a slower pace, with the net‑easing index moving to –2.7 in Q1 2026. While still negative, this marks the most neutral reading in four years, suggesting lenders are cautiously re‑engaging after a prolonged period of tightening. The Federal Reserve’s Senior Loan Officer Survey mirrors this trend, posting a –4.9 reading that falls within its “essentially unchanged” range. Together, these indices indicate that while credit remains tighter than in 2025 Q4, the pace of contraction is decelerating, offering a modest reprieve for developers seeking construction financing.

Effective interest rates, which combine contract rates and upfront points, have trended lower since their peaks in late 2023 and early 2024. Land acquisition rates fell to an effective 9.36%, and land development to 10.15%, reflecting modest point reductions. Conversely, speculative and pre‑sold single‑family construction rates edged higher, pushing effective rates to 11.22% and 11.68% respectively. The overall decline from peak levels eases cost pressures for builders, yet the mixed quarterly shifts underscore the sector’s sensitivity to broader monetary policy and inflation dynamics. Lower rates can stimulate project starts, but lingering uncertainty may temper builder confidence.

A notable shift is the growing reliance on construction‑to‑permanent (one‑time‑close) financing. In Q1 2026, 35% of builders reported using this structure, with 51% of the homes they built financed through a single loan to the eventual buyer. This approach reduces the need for separate construction loans, streamlining the financing process and transferring more risk to homebuyers. For lenders, it offers a more efficient pipeline, while buyers benefit from reduced closing costs and faster loan approvals. As credit conditions remain cautiously tight, the one‑time‑close model may gain traction, influencing future financing strategies across the residential construction market.

Credit for Builders Tightens in the First Quarter, But Only Slightly

Comments

Want to join the conversation?

Loading comments...