The Brutal Truth About Series B: Only 1 in 3 Deals Even Double Investors’ Money, Per Latest Carta Data

•October 28, 2025

0

Why It Matters

The findings reveal the low probability of meaningful returns at the Series B stage, forcing venture firms to concentrate capital in a few winners and prompting founders to price conservatively and pursue category leadership.

Key Takeaways

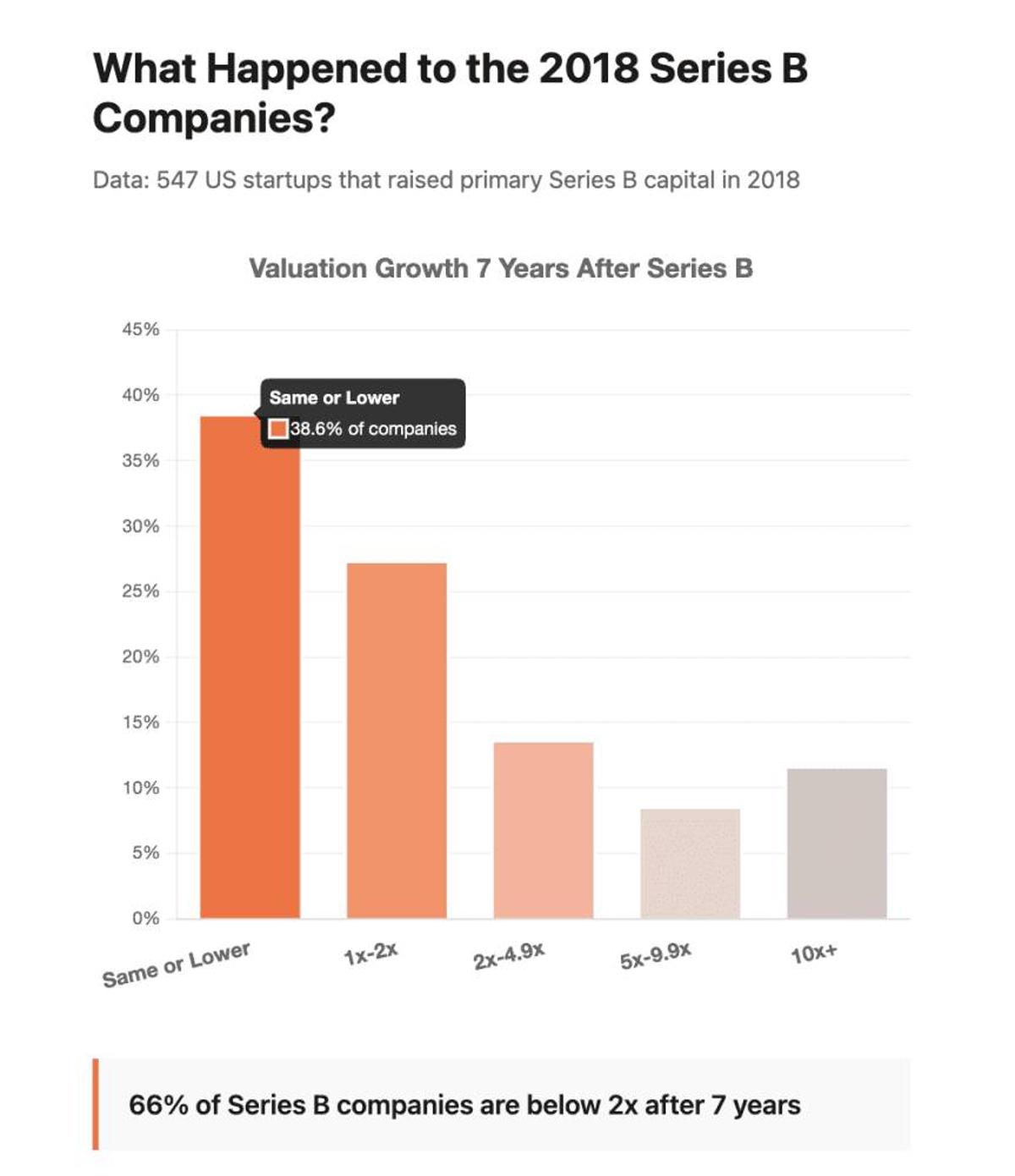

- •66% of 2018 Series B deals underperformed 2× returns.

- •Only 11.7% achieved 10×+ multiples.

- •Valuation discipline crucial for investor upside.

- •Follow‑on capital needed to capture winner upside.

- •Founders must target category dominance, not just PMF.

Pulse Analysis

Series B financing sits at the crossroads of early traction and scaling ambition, yet Carta’s seven‑year follow‑up shows that most companies fail to justify the capital deployed. The power‑law distribution—where roughly 12% of deals generate tenfold returns and the remaining two‑thirds languish below 2×—mirrors the broader venture ecosystem. This concentration means that limited partners rely heavily on a few blockbuster exits to meet their 3×‑plus net‑multiple targets, making the selection process for Series B investors more akin to a high‑stakes lottery than a predictable pipeline.

For venture firms, the data compels a shift toward larger check sizes in a narrower set of high‑conviction bets and a disciplined reserve for follow‑on rounds. By allocating substantial capital to the 10% of deals that can become category leaders, funds can offset the inevitable losses from the 66% that underperform. This approach explains why top‑tier VCs are raising billion‑dollar funds and writing $20‑30 million Series B checks—it's a mathematical necessity to capture the outsized upside of the power‑law tail.

Founders, meanwhile, should treat the median outcome as a warning sign. Pricing the round conservatively, securing investors with deep pockets for future rounds, and building defensible market positions are essential tactics. A focus on category dominance, rather than merely achieving product‑market fit, improves the probability of landing in the elite 10‑plus‑multiple cohort. In a landscape where two‑thirds of Series B companies never return capital, disciplined valuation and strategic growth plans are the only levers founders can pull to tilt the odds in their favor.

The Brutal Truth About Series B: Only 1 in 3 Deals Even Double Investors’ Money, Per Latest Carta Data

0

Comments

Want to join the conversation?

Loading comments...