Companies Mentioned

Why It Matters

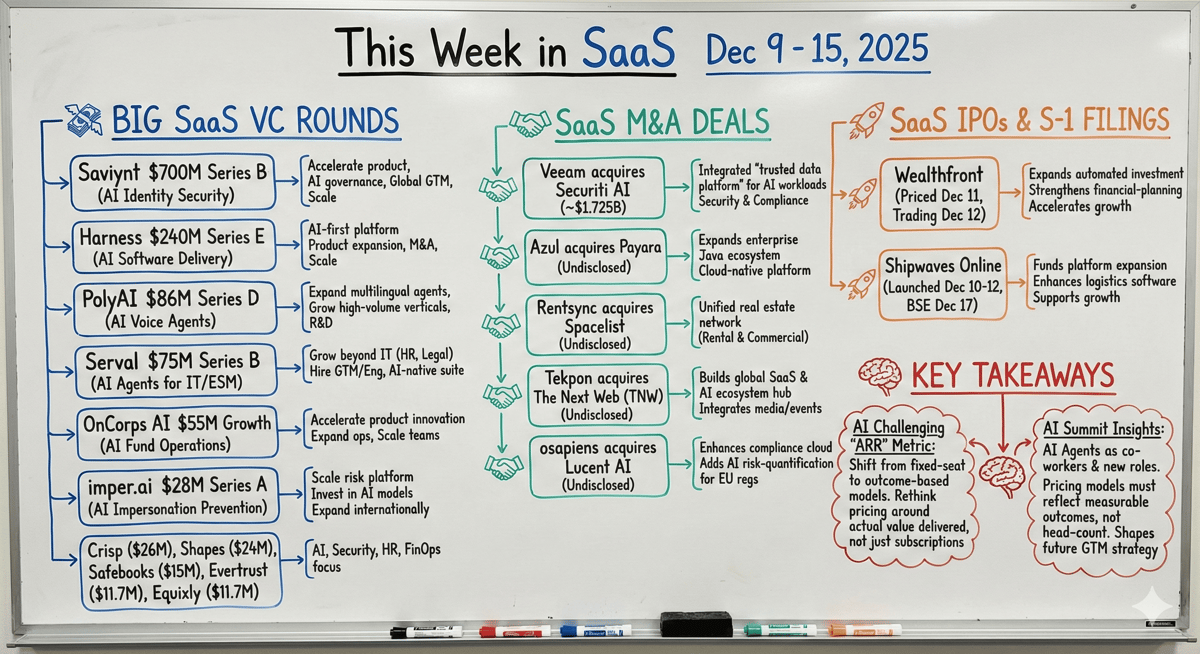

The surge in AI‑focused capital and strategic acquisitions accelerates consolidation and innovation across enterprise SaaS, while the move toward outcome‑based pricing reshapes valuation benchmarks and investor expectations.

Key Takeaways

- •AI‑focused SaaS raised over $1.3 B in December

- •Veeam’s acquisition creates integrated trusted data platform

- •Wealthfront IPO funds automated investment platform expansion

- •Outcome‑based pricing challenges traditional ARR metrics

Pulse Analysis

The December funding wave underscores how AI is reshaping the SaaS landscape. Companies such as Saviynt, Harness and PolyAI secured $700 M, $240 M and $86 M respectively, pushing total AI‑centric capital inflows past $1.3 billion for the week. Investors are rewarding platforms that embed generative models into identity security, DevOps and conversational agents, signaling a market pivot toward AI‑first product roadmaps and global go‑to‑market scaling.

Parallel to the financing surge, strategic M&A activity is consolidating AI and data‑security capabilities. Veeam’s $1.7 B purchase of Securiti AI merges data‑resilience with cloud‑native security, while Azul’s acquisition of Payara strengthens its Java‑centric SaaS stack. These deals illustrate a broader trend: larger incumbents are buying niche AI specialists to accelerate product integration, broaden addressable markets, and meet tightening regulatory demands, especially in Europe’s emerging compliance frameworks.

Beyond capital and consolidation, the industry’s valuation fundamentals are evolving. Traditional ARR multiples are losing relevance as AI‑driven, outcome‑based pricing gains traction, a shift highlighted by Business Insider and HubSpot analyses. Investors now prioritize demonstrable productivity gains and AI adoption metrics over static subscription revenue, prompting founders to reframe growth narratives around value delivery. This pricing transformation, coupled with robust funding and M&A activity, suggests a more dynamic, performance‑orientated SaaS ecosystem for 2026.

This Week in SaaS - Dec 9 - 15, 2025

0

Comments

Want to join the conversation?

Loading comments...