Why It Matters

The influx of capital and strategic acquisitions accelerates AI‑driven SaaS consolidation, while operational readiness and outcome‑based pricing become decisive for growth and fundraising.

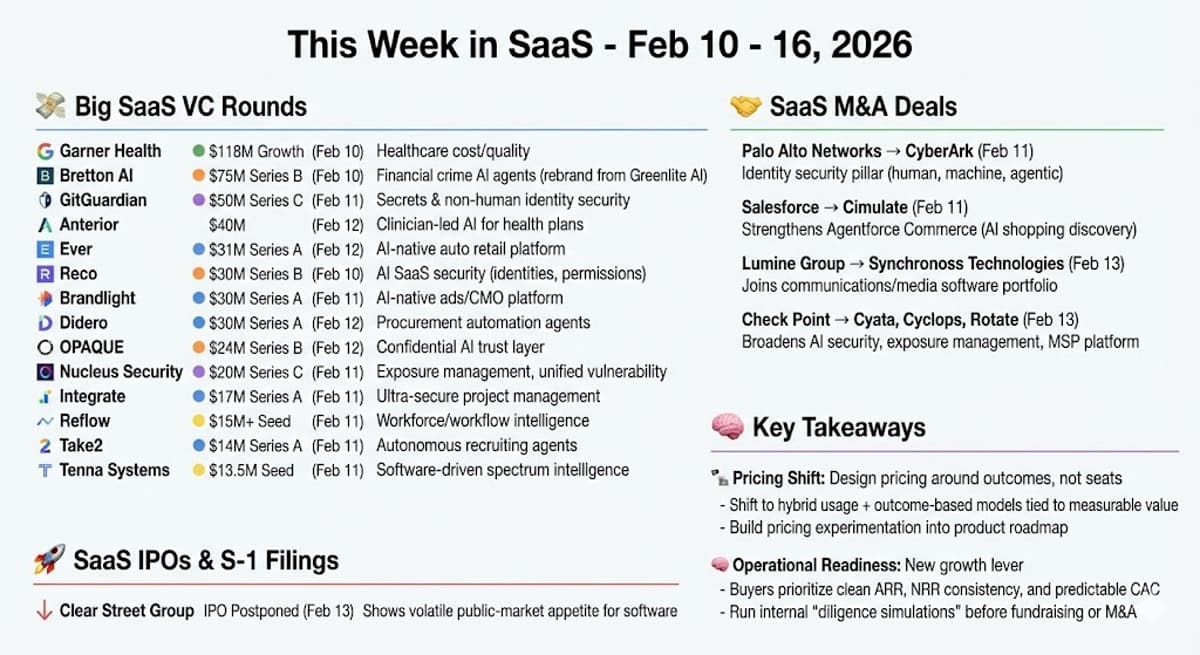

Key Takeaways

- •$118M raised by Garner Health for provider ranking engine.

- •Palo Alto acquires CyberArk, bolstering identity security.

- •SaaS pricing shifting to outcome‑based models.

- •Operational readiness now critical for late‑stage funding.

- •Growth program targets $1M+ ARR SaaS firms, $5k/month.

Pulse Analysis

The February funding surge signals that investors are betting heavily on AI‑native SaaS platforms that can embed intelligence into core business processes. Companies like Garner Health, Bretton AI, and GitGuardian secured multi‑digit million‑dollar rounds to expand capabilities ranging from provider‑ranking engines to AI‑agent compliance tools. This capital influx not only validates the market appetite for AI‑enhanced solutions but also raises the competitive bar for emerging startups seeking differentiation in crowded verticals.

Concurrently, strategic M&A activity reshapes the SaaS landscape, with Palo Alto Networks absorbing CyberArk to fortify its identity security suite and Salesforce targeting Cimulate to deepen its Agentforce Commerce offering. These deals illustrate a broader industry trend: larger platforms are acquiring niche AI and identity technologies to create unified, end‑to‑end experiences for both human and machine users. The acquisitions also hint at a future where security and contextual AI become inseparable components of enterprise software stacks.

For founders and executives, the week’s developments underscore two actionable imperatives. First, outcome‑based pricing models are rapidly supplanting traditional seat‑based licensing, demanding granular usage instrumentation and value‑linked pricing experiments. Second, operational readiness—clean ARR reporting, consistent NRR, and predictable CAC payback—has become a decisive lever for late‑stage investors and acquirers. Programs like SaasRise’s Growth Initiative provide a practical pathway to embed these practices while scaling go‑to‑market engines, positioning SaaS firms to thrive amid heightened capital activity and consolidation pressures.

This Week in SaaS Feb 10 - 16, 2026

0

Comments

Want to join the conversation?

Loading comments...