The Business Reality Behind FAA Authorized Spaceports

Companies Mentioned

Why It Matters

Understanding the real economic drivers behind FAA‑authorized spaceports helps investors and policymakers target infrastructure that delivers jobs and revenue, rather than counting licenses as a proxy for activity.

Key Takeaways

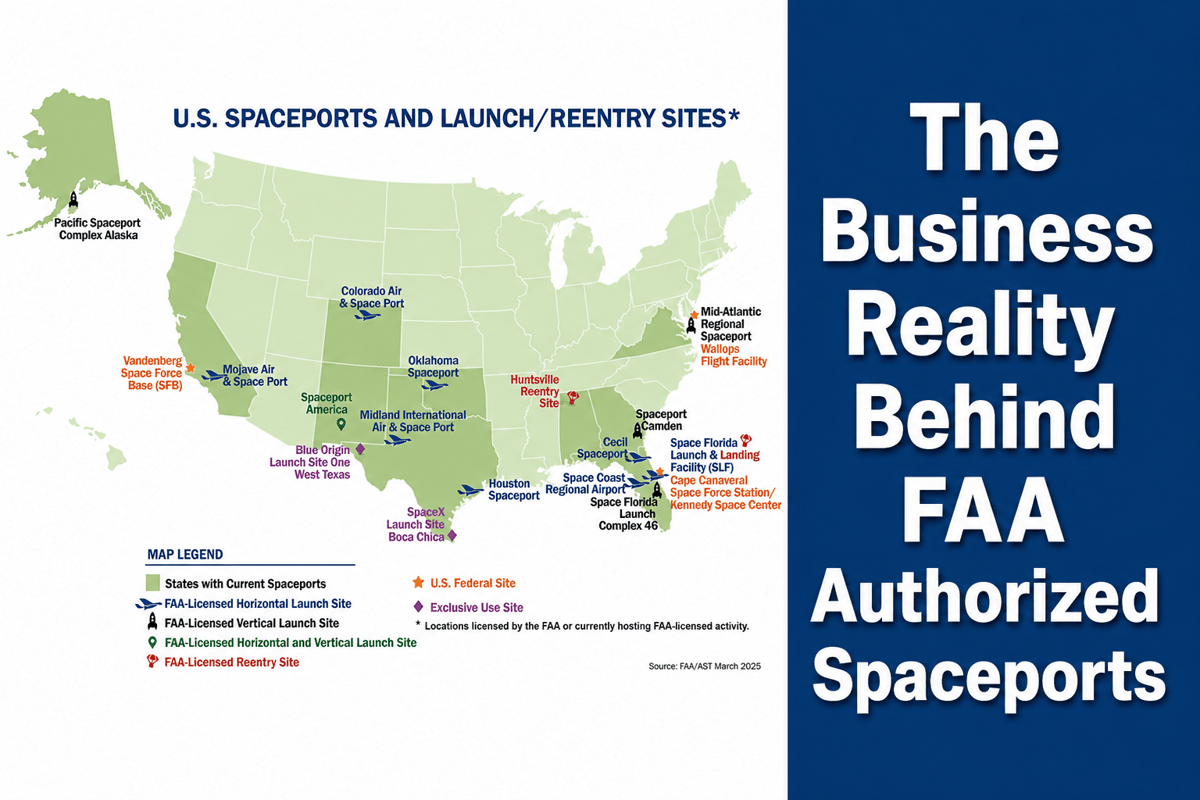

- •FAA licenses 20 U.S. sites, but launch cadence varies widely

- •Federal ranges in FL and CA drive most commercial launches

- •Horizontal spaceports rely on aerospace tenants, not launch frequency

- •Private exclusive‑use sites tie regional economies to single corporate programs

- •License status alone doesn’t guarantee activity; land and community issues matter

Pulse Analysis

The United States’ spaceport ecosystem is a patchwork of federal ranges, state‑backed launch sites, and privately owned exclusive‑use facilities. The FAA distinguishes between launch‑site operator licenses (14 CFR Part 420) and re‑entry licenses (Part 433), creating three categories that appear on a single public list. This regulatory framework masks the operational reality: only a handful of sites—Cape Canaveral Space Force Station, Kennedy Space Center, Vandenberg Space Force Base, and the private Boca Chica complex—support a high launch cadence, while the remaining licensed ports serve niche roles such as horizontal launch testing, re‑entry operations, or aerospace manufacturing clusters.

Economic impact studies underscore the uneven contribution of these ports. Florida’s federal range complex alone underpinned $8.2 billion in state economic output and over 35,000 jobs in FY 2023, while Spaceport America’s 2025 study reported $240 million in output and 790 jobs, a threefold increase from 2019. In contrast, Spaceport Camden retains a valid license but remains dormant due to land disputes and community opposition, illustrating that a license does not equal a revenue stream. Horizontal ports like Mojave and Huntsville leverage their runway infrastructure to attract test‑flight programs and defense contractors, generating indirect employment even with limited launch activity.

For investors and policymakers, the lesson is clear: the value of a spaceport lies in its ability to attract anchor tenants, integrate with existing aerospace clusters, and secure stable funding beyond the initial licensing. Federal ranges benefit from decades of infrastructure and government contracts, while state‑backed ports must diversify into research, manufacturing, and education to stay viable. Private exclusive‑use sites, tied to single corporate programs, can deliver rapid regional growth but also pose concentration risk. Future growth will depend on aligning licensing with realistic market demand, addressing community concerns, and fostering public‑private partnerships that turn regulatory approvals into sustainable economic engines.

The Business Reality Behind FAA Authorized Spaceports

Comments

Want to join the conversation?

Loading comments...