Hate-Sold Growth Stocks May Still Be Bargains

Key Takeaways

- •Growth stocks down 20% since October versus 2% S&P gain

- •Goldman’s Rule of 10 identifies 30+ S&P firms, most ever

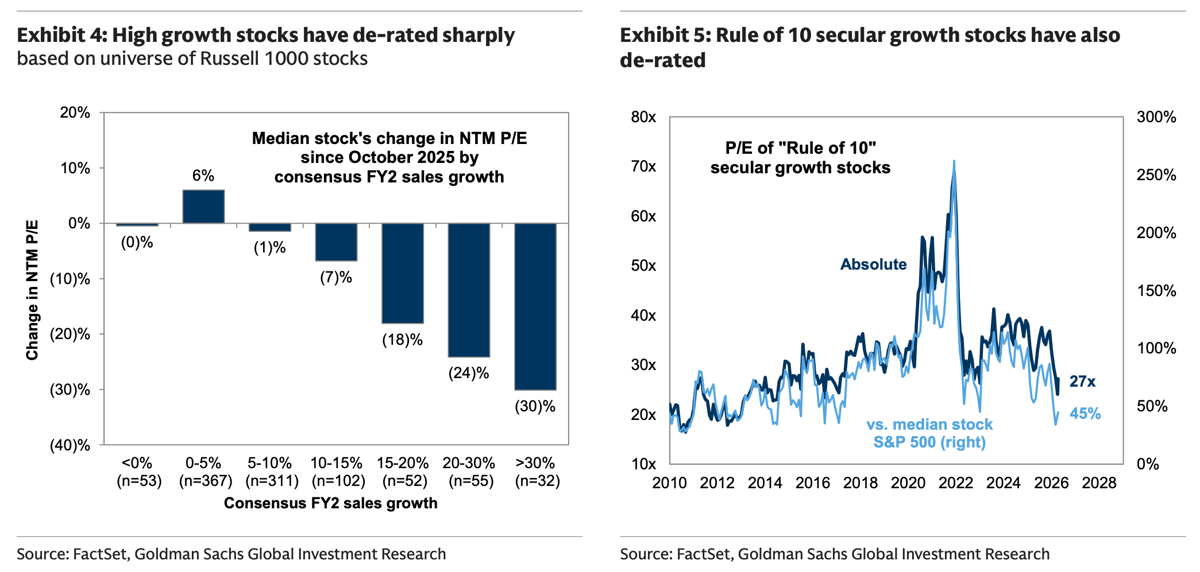

- •Median P/E for secular growers at 27x, a post‑pandemic discount

- •Non‑software growers trade at 29x, near decade‑low premium

- •AI scare and higher yields erased two years of outperformance

Pulse Analysis

Goldman Sachs’ secular‑growth screen, popularly known as the Rule of 10, isolates non‑financial S&P 500 companies that have sustained double‑digit sales growth for three straight years. The latest data shows the cohort has suffered a roughly 20% slide since October, starkly contrasting the broader market’s modest 2% gain. This underperformance coincides with an AI‑related market scare, rising bond yields, and a surge in oil prices that together erased two years of outperformance for growth‑heavy indices.

Valuation metrics reinforce the narrative of a market correction. The Rule‑of‑10 basket now trades at a forward price‑to‑earnings multiple of about 27x, a figure that, while not cheap by absolute standards, represents a significant compression from its pandemic‑era premium of over 50% to the median S&P stock. Even non‑software growth firms, often overlooked in the current software‑centric debate, are priced around 29x, hovering near the lowest premium levels observed in the past decade. This de‑rating, especially the 30% drop in the highest‑growth segment, signals that investors are demanding a larger discount for future uncertainty.

For portfolio managers, the convergence of steep price declines and historically low valuation premiums may signal a buying opportunity. The breadth of the list—more than three dozen companies, a record high—means exposure is not confined to a single sector, offering diversification benefits. However, the lingering macro headwinds—persistent inflation, volatile oil markets, and lingering AI execution risk—require disciplined risk management. Savvy investors might consider selective re‑entry, focusing on firms with solid balance sheets and clear growth trajectories, while maintaining vigilance for further market turbulence.

Hate-Sold Growth Stocks May Still Be Bargains

Comments

Want to join the conversation?