LLC Vs. C-Corp for Startups: How to Choose the Right Entity

Key Takeaways

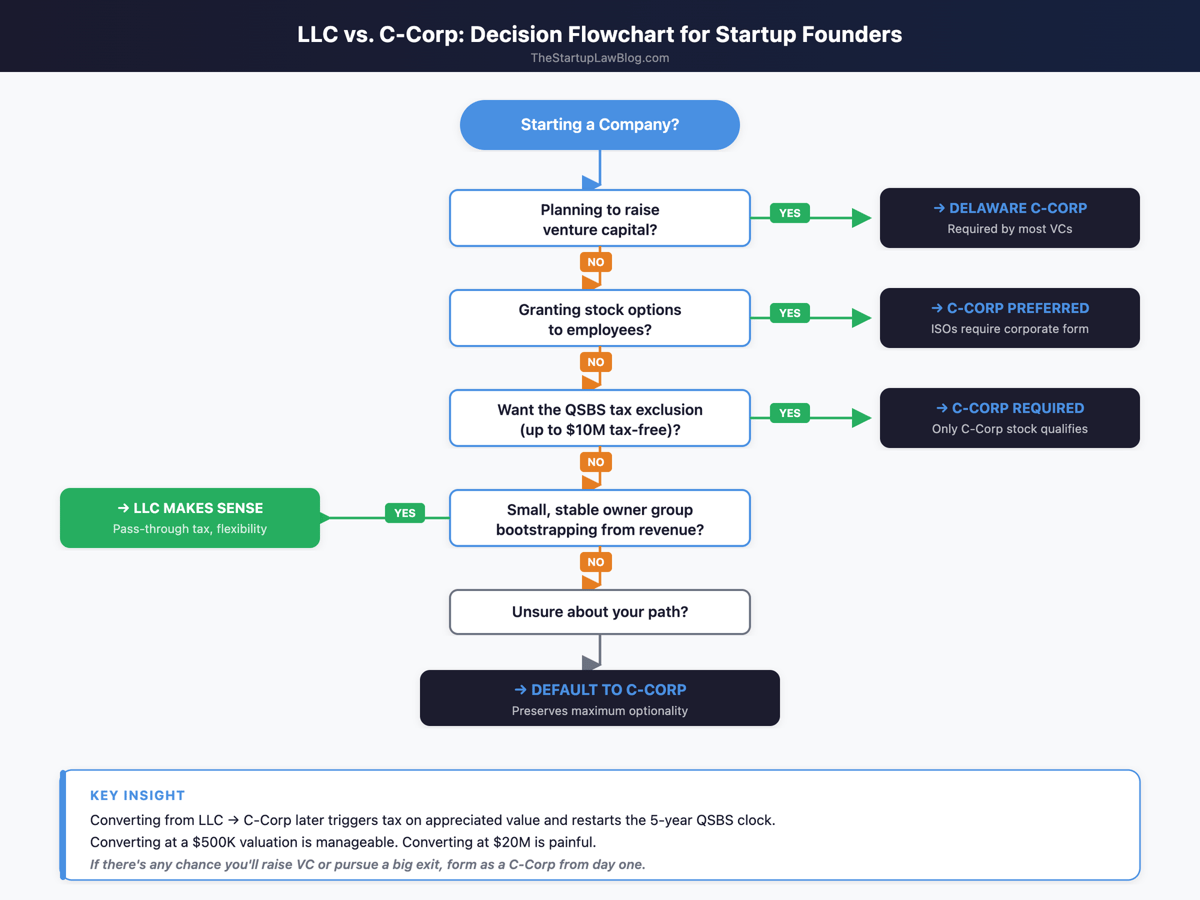

- •VC-backed startups almost always need a Delaware C‑Corp

- •LLCs avoid double tax but can create phantom income

- •C‑Corp stock qualifies for QSBS, saving millions on capital gains

- •Converting an appreciated LLC to a C‑Corp triggers taxable gain

Pulse Analysis

Entity selection is one of the first strategic decisions a founder makes, yet its ramifications echo throughout a company’s lifecycle. An LLC offers pass‑through taxation, meaning profits are taxed only once on the owners’ personal returns, which is attractive for bootstrapped teams that expect early profitability. However, the simplicity can be deceptive; founders may face "phantom income" when the LLC retains earnings, forcing them to pay tax on cash they never receive. In contrast, a C‑Corporation pays corporate tax at a flat 21% and defers shareholder tax until dividends or a sale, a structure that aligns with the reinvest‑and‑grow model of most high‑growth startups.

The fundraising landscape heavily favors the C‑Corp form. Venture capital firms prefer Delaware corporations because standardized stock classes, preferred‑stock mechanics, and clear governance frameworks simplify due diligence and legal work. Moreover, only C‑Corp shareholders can benefit from Qualified Small Business Stock (QSBS) under Section 1202, which can exclude up to $10 million or ten‑times the basis in capital gains—a potential multi‑million‑dollar advantage at exit. Employee equity compensation also leans toward C‑Corps; Incentive Stock Options (ISOs) and Non‑Qualified Stock Options (NSOs) are well‑understood, tax‑efficient, and supported by routine 409A valuations, whereas LLC profit interests are more complex and less attractive to talent.

Conversion from an LLC to a C‑Corp is technically feasible but often costly. The process is treated as a taxable exchange, meaning founders may recognize substantial capital gains when the company’s valuation has risen, eroding the very gains they hoped to capture. State tax considerations add another layer: Delaware’s franchise tax is modest for early companies, while states like Washington now impose a 9.9% income tax on pass‑through income, diminishing the LLC’s tax advantage. Ultimately, for startups eyeing venture funding, employee stock plans, or a high‑value exit, incorporating as a C‑Corp from the outset preserves flexibility, minimizes conversion pain, and unlocks the QSBS benefit. For lifestyle or consultancy businesses with limited growth ambitions, an LLC remains a sensible, low‑overhead choice.

LLC vs. C-Corp for Startups: How to Choose the Right Entity

Comments

Want to join the conversation?