January’s Mild Inflation Report Comes with ‘Qualifications’

•February 14, 2026

0

Key Takeaways

- •CPI rose 0.3% month‑over‑month

- •Core inflation eased to 4.8% annual

- •Energy prices dropped, offsetting services inflation

- •Fed likely to hold rates longer

- •TIPS yields gain investor attention

Summary

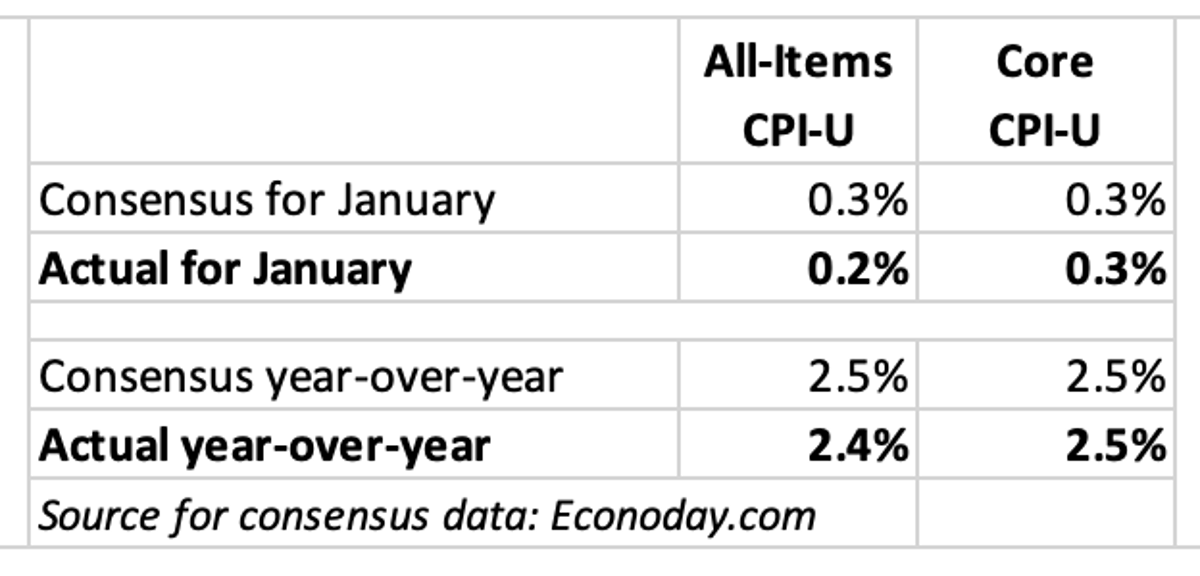

January’s consumer‑price index showed modest headline inflation, rising 0.3% month‑over‑month and 3.2% year‑over‑year, but the report included several qualifiers. Core CPI eased to 4.8% annual, driven by lower energy costs, while shelter and services remained sticky. Analysts highlighted the mixed signals for the Federal Reserve, noting that the modest headline may not translate into immediate policy easing. The data also revived interest in Treasury Inflation‑Protected Securities as investors reassess real‑yield expectations.

Pulse Analysis

January’s inflation report delivered a headline figure that appeared milder than expected, but the underlying components told a more complex story. While the overall CPI increased 0.3% from the previous month, core inflation—excluding volatile food and energy—slowed to 4.8% year‑over‑year, reflecting easing pressure in sectors such as transportation and manufacturing. Energy prices, in particular, fell sharply, providing a counterbalance to persistent shelter costs that continue to weigh on the broader price index. These mixed signals suggest that the inflation trajectory is uneven, prompting analysts to look beyond headline numbers when forecasting monetary policy.

For the Federal Reserve, the qualified softness offers limited room for aggressive rate cuts. The central bank’s dual mandate still prioritises price stability, and the stickiness in housing and services inflation signals that underlying demand pressures remain. Consequently, many market participants expect the Fed to maintain its current policy stance through the next meeting, using a data‑dependent approach rather than pre‑emptively easing. This cautious outlook is reflected in the bond market, where real‑yield expectations have adjusted, and investors are scrutinizing the spread between nominal Treasury yields and Treasury Inflation‑Protected Securities (TIPS).

The TIPS market, in particular, has seen renewed interest as investors seek protection against any resurgence in inflation. With the 30‑year TIPS auction approaching, the qualified inflation data has made the real yield more attractive, prompting discussions about longer‑duration inflation hedges despite the inherent maturity risk. Market analysts suggest that the upcoming auction could set a benchmark for future real‑rate expectations, influencing portfolio allocations across both institutional and retail investors. Understanding these dynamics is crucial for anyone navigating the current fixed‑income landscape, where nuanced inflation readings drive strategic decisions.

Comments

Want to join the conversation?