Bond Yields Fall After CPI Report Shows Tamer Inflation

•February 13, 2026

0

Why It Matters

The yield decline improves borrowing costs for state and local projects, while the Fed’s cautious stance signals limited near‑term rate volatility for fixed‑income investors.

Key Takeaways

- •CPI cooler than expected, inflation nearing four‑year low

- •U.S. Treasury yields slipped 8‑10 bps; munis followed

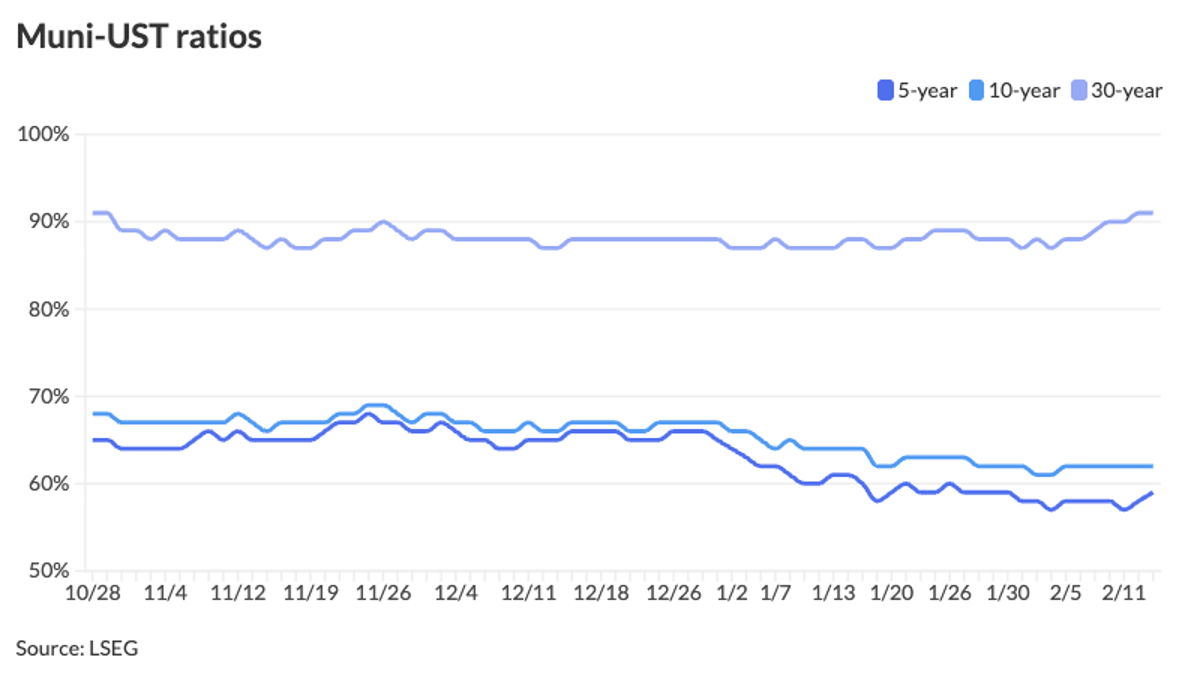

- •Muni‑UST ratios remain rich, 10‑yr around 62%

- •February new‑issue calendar $6.9 billion, demand remains high

- •Fed likely holds rates, eyeing cuts later this year

Pulse Analysis

The latest consumer‑price index showed inflation easing to a four‑year low, easing pressure on the Federal Reserve’s policy curve. While the data was better than forecasts, the labor market’s strength kept the Fed from committing to immediate cuts, prompting analysts to project only two rate reductions by year‑end. Treasury yields responded with an 8‑10 basis‑point dip, a move mirrored by municipal bonds, which have been buoyed by the broader risk‑off sentiment and a relatively stable demand environment.

Municipal markets entered the week on a firm footing, with the two‑year muni‑UST spread hovering around 60% and the 10‑year spread near 62%, indicating that muni yields remain rich compared with Treasuries. A $6.9 billion new‑issue pipeline, led by green revenue bonds from California and GO improvement bonds from Nashville, kept supply modest, while inflows of roughly $2 billion underscored strong investor appetite. Barclays and BofA strategists note that the technical backdrop for munis remains supportive, even as the broader Treasury market grapples with demand constraints.

Looking ahead, the combination of modest inflation, resilient employment, and a limited new‑issue slate suggests a sideways trajectory for rates through the spring. Investors are likely to shift focus from macro‑driven rate bets to fundamentals such as earnings discipline and balance‑sheet strength, especially in high‑yield municipal sectors like clean‑energy and infrastructure. The prevailing environment offers a favorable cost of capital for state and local projects, but participants should monitor the upcoming bond redemption cycle and any shifts in fiscal policy that could alter the supply‑demand balance.

Bond yields fall after CPI report shows tamer inflation

0

Comments

Want to join the conversation?

Loading comments...