Munis and U.S. Treasuries Grow Cheaper

Companies Mentioned

Why It Matters

The shift signals tighter pricing pressure for mid‑term munis and highlights renewed investor appetite for higher‑yielding municipal issues, while fund outflows from tax‑exempt money‑markets could constrain short‑term liquidity.

Key Takeaways

- •Munis front‑end yields slipped, causing slight curve inversion near 2028‑2030

- •Morgan Stanley priced $564 million UMass revenue‑refunding bonds across 2026‑2044

- •Round Rock, Texas issued $100 million AAA general‑obligation bonds at 2.5‑3.5% yields

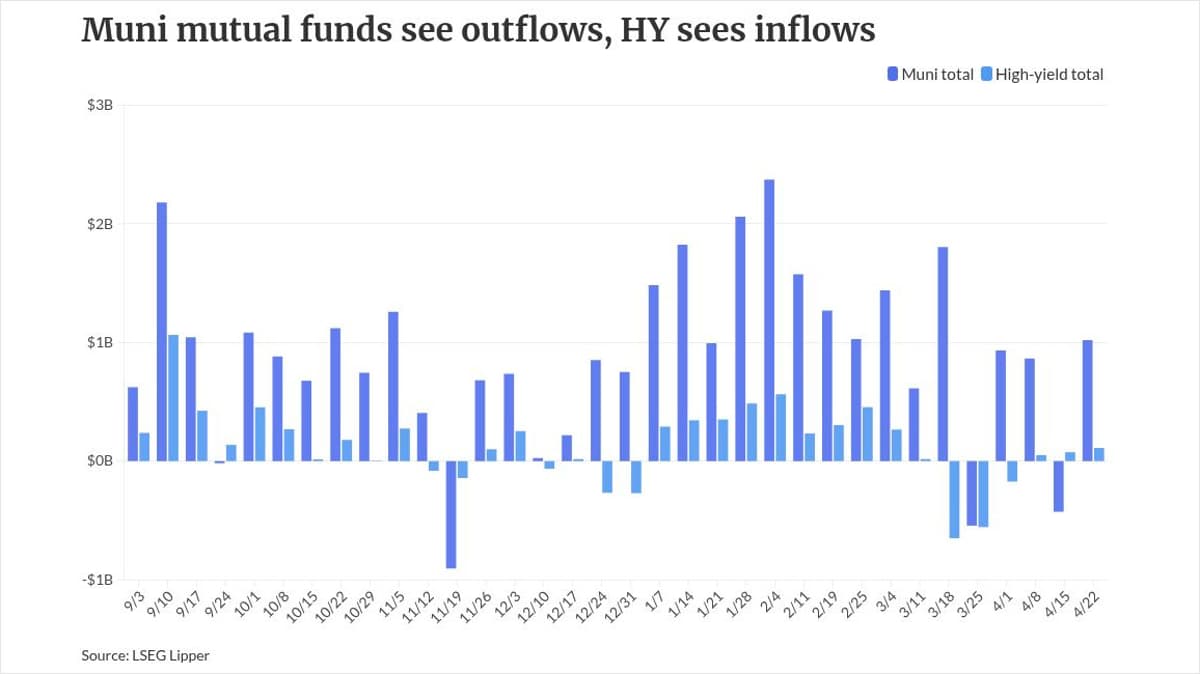

- •Municipal‑bond funds attracted $1.02 billion this week, signaling renewed demand

- •Tax‑exempt money‑market outflows hit $1.19 billion, shrinking assets to $141.8 billion

Pulse Analysis

The municipal bond market is navigating a nuanced yield environment as Treasury rates drift lower and equity markets wobble. Front‑end municipal yields have softened enough to invert the curve around the 2028‑2030 horizon, a zone traditionally favored by investors seeking a balance between credit quality and real‑yield upside. This inversion reflects heightened sensitivity to real‑yield expectations and a perception that the 2.5%‑3.0% range may be the sweet spot for new issuance, prompting some investors to pause while they reassess relative value against Treasury benchmarks.

Issuance activity on Thursday underscored the market’s willingness to price new debt despite the yield compression. Morgan Stanley’s underwriting of $564 million in University of Massachusetts revenue‑refunding bonds spanned maturities from 2026 to 2044, with yields ranging from 2.50% to 3.80% and call features designed to manage refinancing risk. Meanwhile, Round Rock, Texas secured $100 million of AAA‑rated general‑obligation bonds, offering yields between 2.52% and 3.54% across a ten‑year ladder. These deals illustrate that high‑credit municipal issuers can still attract capital by offering modestly higher yields than Treasuries, while investors remain attentive to call protection and the evolving real‑yield landscape.

Fund flow data adds another layer of insight. Municipal‑bond mutual funds absorbed $1.02 billion this week, a sharp uptick from the prior period, indicating renewed confidence in the sector’s risk‑adjusted returns. Conversely, tax‑exempt money‑market funds experienced $1.19 billion of outflows, pulling total assets down to $141.8 billion and hinting at a shift toward longer‑duration municipal exposure. The SIFMA Swap Index’s slight dip to 3.62% reinforces the broader fixed‑income softness, suggesting that investors may continue to chase higher‑yielding municipal opportunities as Treasury yields remain subdued. This dynamic sets the stage for a competitive issuance environment where pricing, credit quality, and call structures will be pivotal in attracting capital.

Munis and U.S. Treasuries grow cheaper

Comments

Want to join the conversation?

Loading comments...