T-Bill Yields Climb After 7-Week Slide

•March 2, 2026

0

Why It Matters

Higher T‑bill yields signal tighter financing conditions for the Philippine government and could foreshadow stronger monetary policy to curb inflation. The shift also highlights how regional geopolitical shocks transmit to emerging‑market debt markets.

Key Takeaways

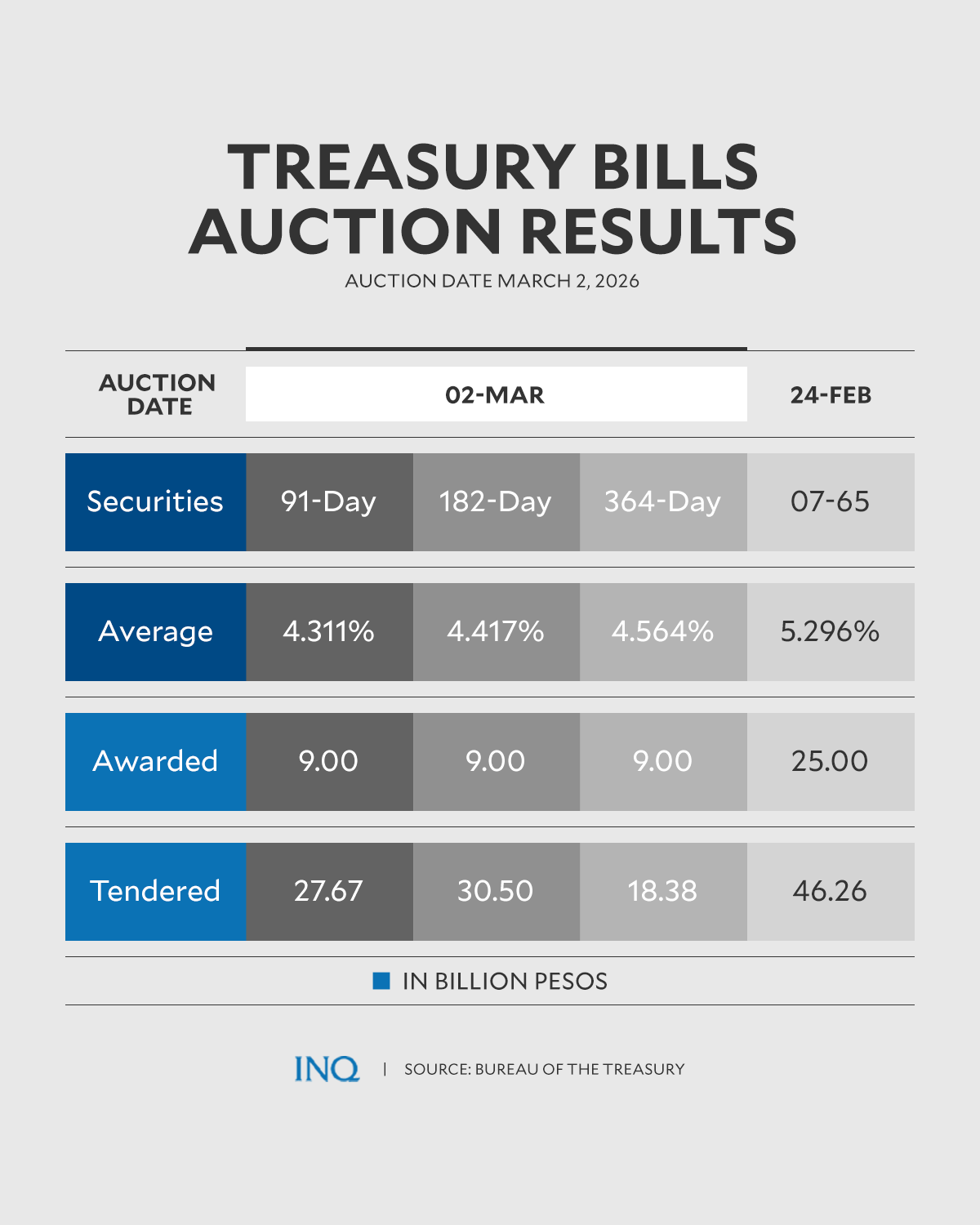

- •91‑day T‑bill yield reached 4.311%

- •182‑day yield climbed to 4.417%

- •364‑day yield rose to 4.564%

- •Investors wary of February inflation data

- •Middle‑East tensions push oil prices, affect yields

Pulse Analysis

The recent uptick in Philippine Treasury bill yields marks a notable reversal after a month‑long decline, underscoring the sensitivity of the country’s short‑term debt market to external shocks. While the Bureau of the Treasury managed to raise only P27 billion—significantly lower than the P37.8 billion average earlier in the year—the higher auction rates suggest investors demand a premium for perceived risk. This premium reflects not just domestic inflation concerns but also the broader macro‑environment, where emerging‑market currencies often react sharply to global volatility.

Two primary forces are driving the yield correction. First, the upcoming February inflation report is expected to show a rise from the 2% recorded in January, prompting market participants to anticipate a tighter monetary stance from the Bangko Sentral ng Pilipinas. Second, the renewed US‑Israel‑Iran confrontation has spiked crude‑oil prices and heightened fears of supply disruptions through the Strait of Hormuz, a chokepoint responsible for roughly 20% of world oil flows. Higher oil prices feed into domestic fuel costs, eroding real incomes and reinforcing inflationary pressures, which in turn push short‑term borrowing costs upward.

Looking ahead, the Treasury’s reduced auction size may signal a cautious fiscal approach, but the higher yields could increase the cost of servicing public debt if the trend persists. Investors will likely monitor the inflation data closely and assess whether the central bank will adjust policy rates. Meanwhile, regional peers will watch the Philippines as a barometer for how Middle‑East tensions can ripple through Asian sovereign markets, influencing portfolio allocations and risk‑premia calculations across the continent.

T-bill yields climb after 7-week slide

0

Comments

Want to join the conversation?

Loading comments...