The Next Muni Credit Debate: Tax Policy, Mobility and Revenue Durability

Companies Mentioned

Why It Matters

The preservation of the muni tax exemption and emerging state tax reforms directly influence borrowing costs and credit ratings, shaping capital‑raising strategies for local governments and essential service providers.

Key Takeaways

- •Federal muni bond tax exemption costs U.S. Treasury ~$25 billion annually

- •2017 tax cuts limited tax‑exempt advance refundings, raising issuers’ refinancing risk

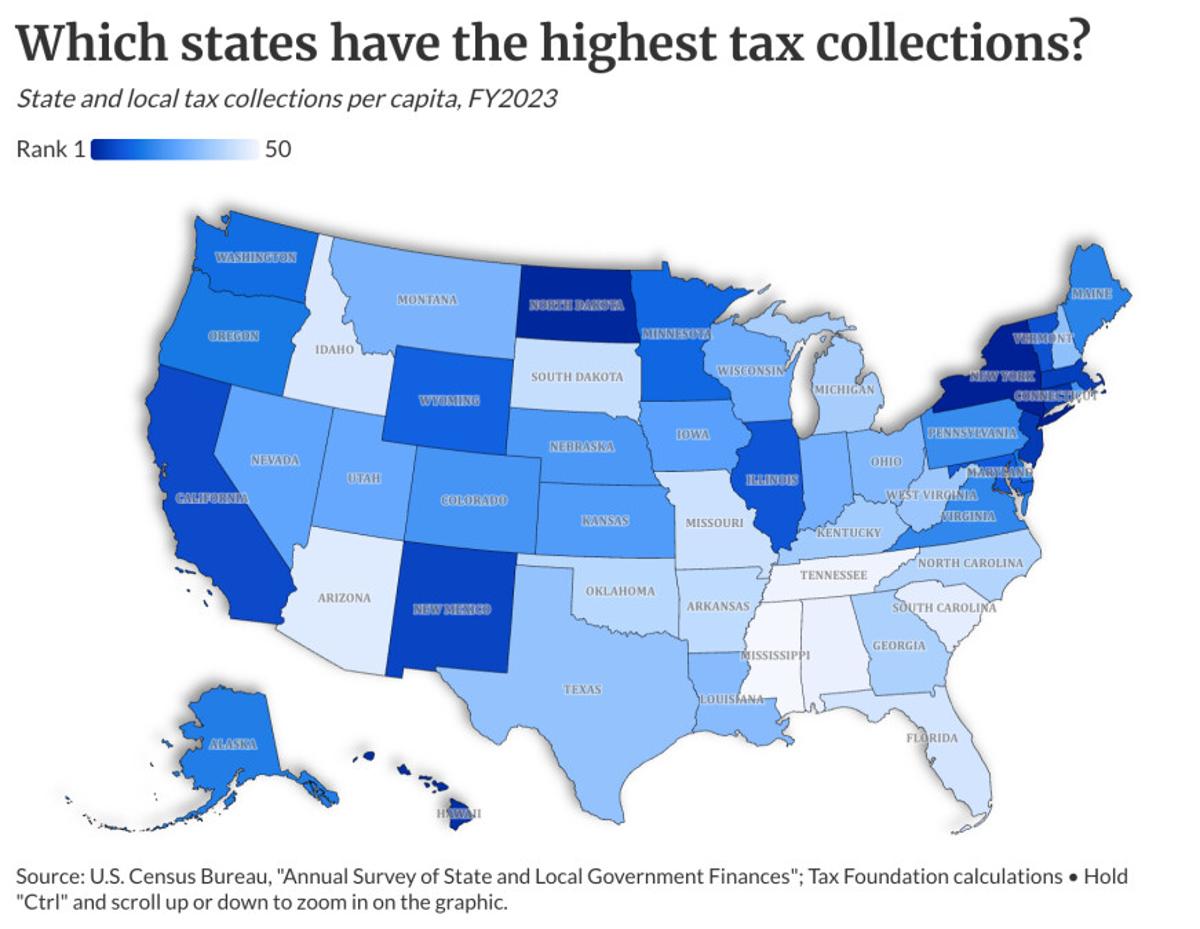

- •State wealth‑tax proposals could generate $100 billion (CA) but face migration concerns

- •Property‑tax cuts in Florida risk $13‑$18 billion revenue loss, affecting services

- •Investors are scrutinizing general‑obligation bonds for credit exposure amid tax reforms

Pulse Analysis

The federal tax exemption on municipal bonds remains the cornerstone of the U.S. public‑finance ecosystem, effectively subsidizing issuers with up to $25 billion in annual lost federal revenue. While the One Big Beautiful Bill Act removed immediate threats of repeal, the exemption’s political fragility resurfaced during the 2026 election cycle, where a narrow Republican majority could face a Democratic surge and renewed calls for reform. Coupled with the 2017 Tax Cuts and Jobs Act’s restriction on advance refundings, issuers now confront higher refinancing costs and reduced balance‑sheet flexibility, especially for long‑duration borrowers such as hospitals and universities.

State‑level tax experiments are adding another layer of uncertainty. California’s ballot‑qualified wealth tax aims to raise roughly $100 billion over five years, yet analysts caution that even modest out‑migration of high‑net‑worth individuals could erode the projected fiscal boost. Meanwhile, Washington’s looming 9.9% surtax on incomes above $1 million and Florida’s proposal to eliminate most non‑school homestead property taxes threaten to create revenue gaps of $5 billion and $13‑$18 billion respectively. These measures force local governments to reconsider funding models for schools, infrastructure, and affordable‑housing programs, potentially shifting reliance toward sales taxes or new fees.

Investors are recalibrating portfolios in response to this policy turbulence. General‑obligation and appropriation bonds, which depend heavily on broad‑based tax revenues, are now viewed as more vulnerable than essential‑purpose revenue bonds such as utilities or airports. Credit analysts are monitoring legislative calendars, reserve levels, and the legal durability of emerging wealth‑tax regimes to gauge default risk. For issuers, proactive engagement with advocacy groups and transparent communication of fiscal strategies will be critical to maintain market confidence. As the midterms approach, the muni market’s ability to adapt to shifting tax landscapes will likely dictate pricing spreads and capital‑raising capacity for years to come.

The next muni credit debate: tax policy, mobility and revenue durability

Comments

Want to join the conversation?

Loading comments...