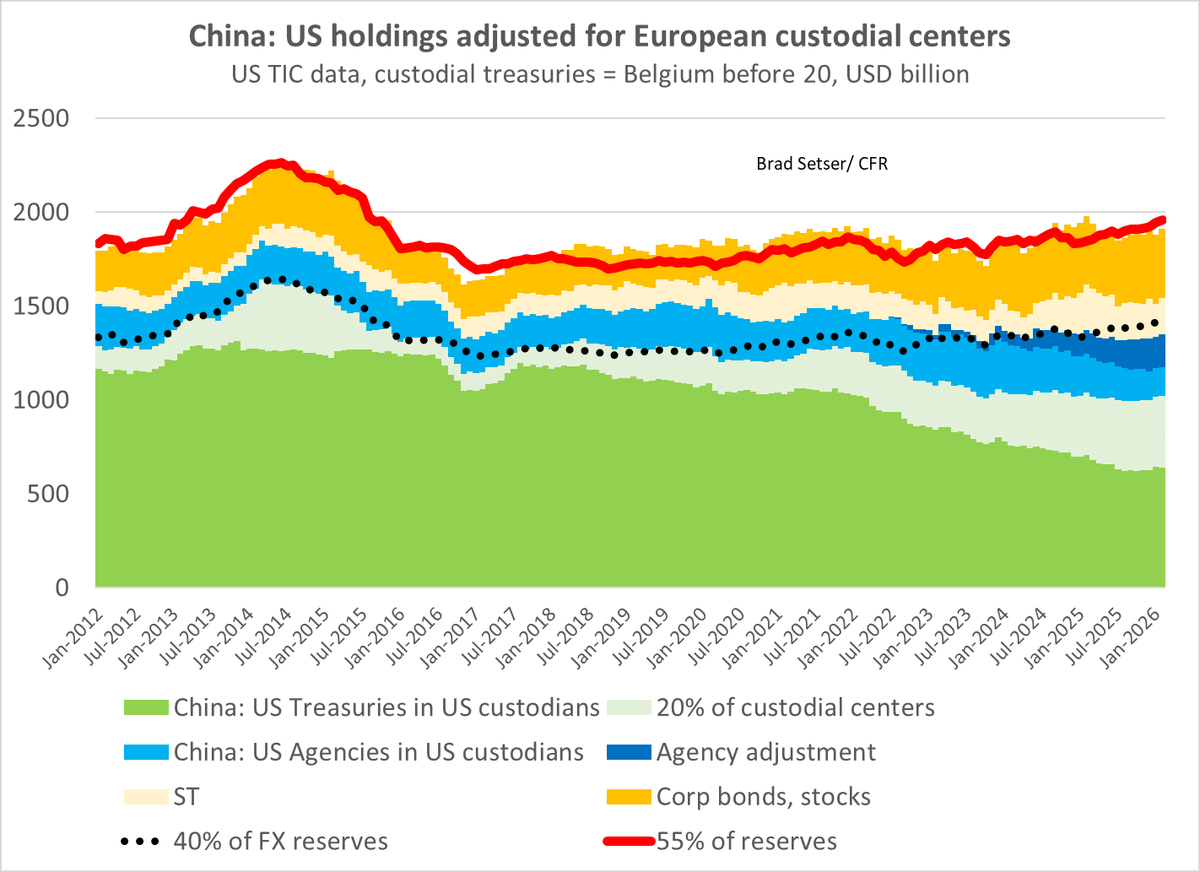

US Custodian Treasury Drop ≠ China’s Bond Holdings Decline

There is a bit more to the story -- Don't equate a fall in Treasuries held in US custodians with a real fall in China's holdings of US bonds https://t.co/ikBtmc32fc

Concentrated Chinese Manufacturing: Efficient yet Risky, Partners Must Manage Trade

Good piece "It’s no longer controversial to say that while having so much manufacturing concentrated in one place might be efficient, it is also dangerous" China's trading partners are increasingly concluding that their trade with China needs to be managed --

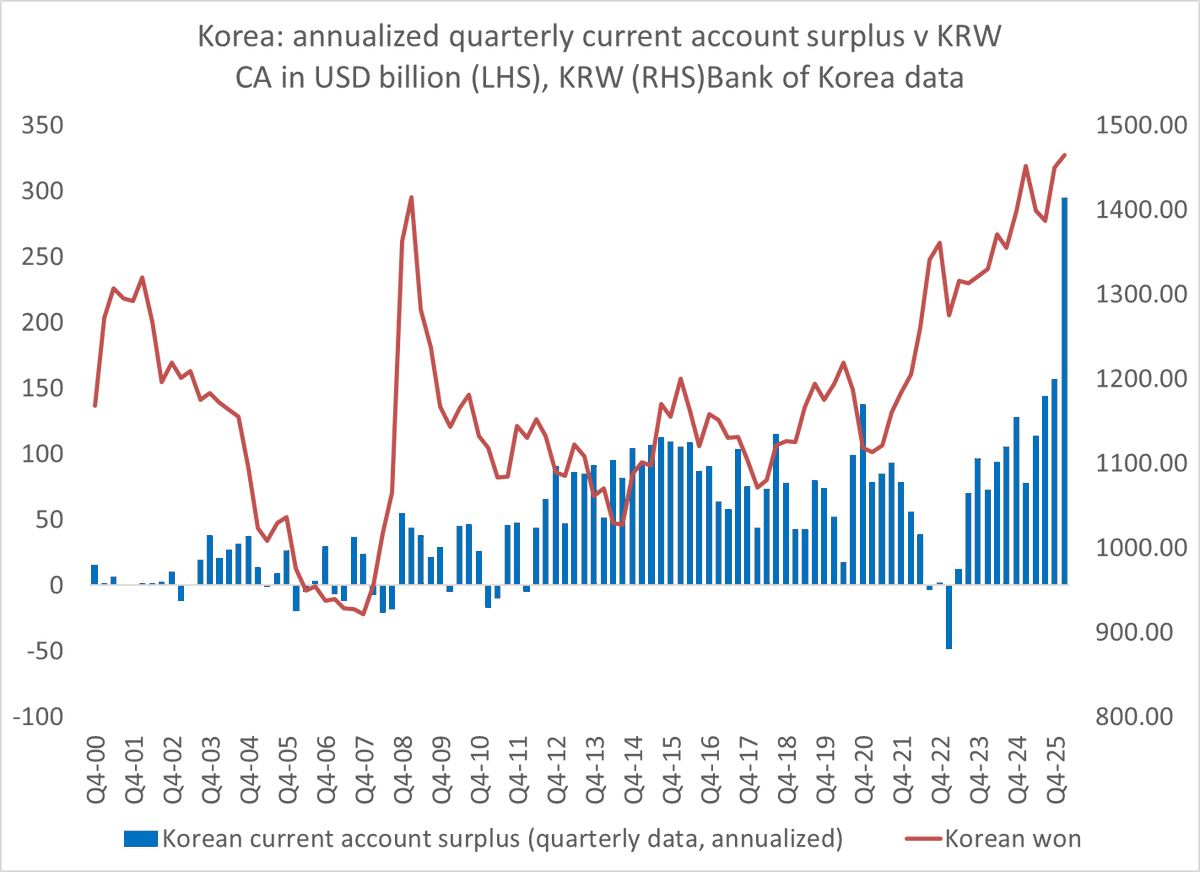

Korea Targets 20%

Hike rates, support the won, limit inflation -- Korea is on track to run a 20% of GDP current account surplus (more if March numbers hold ... ) it can manage without a super weak won

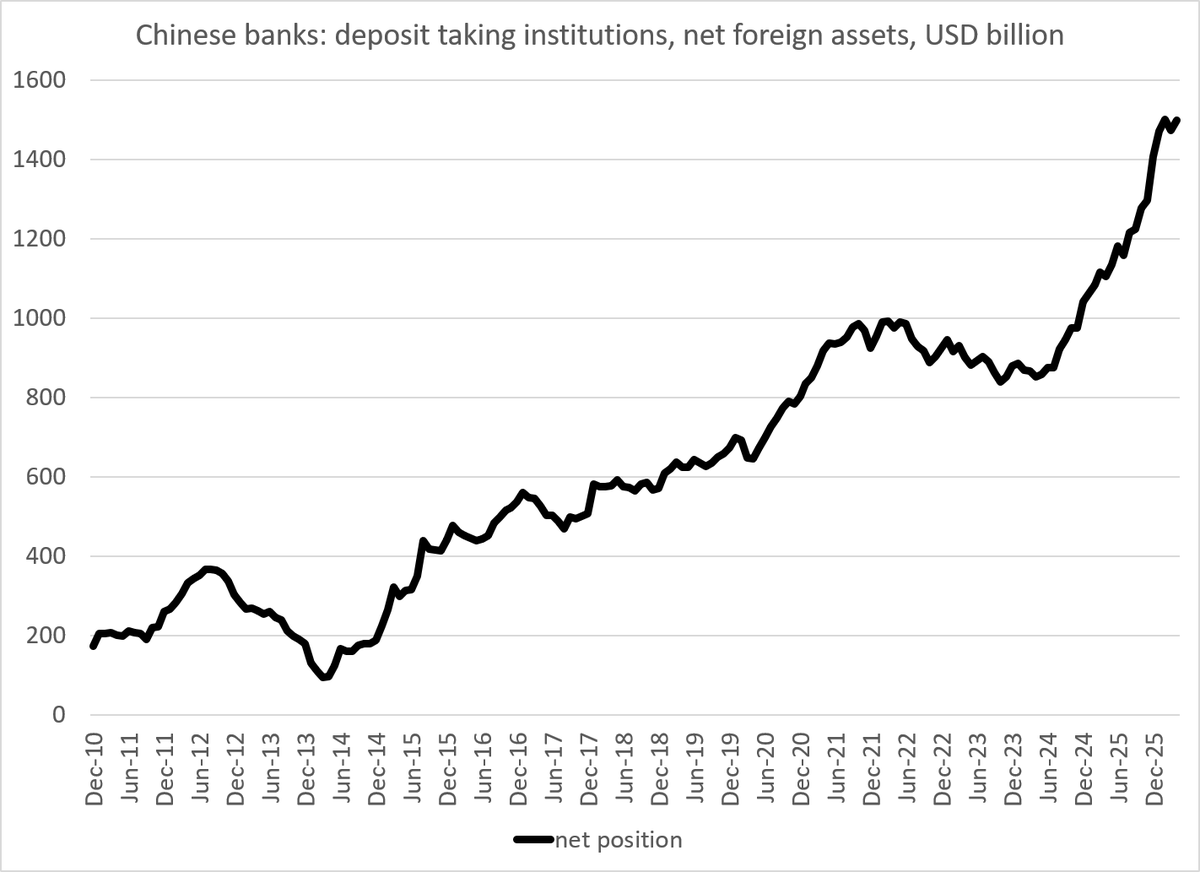

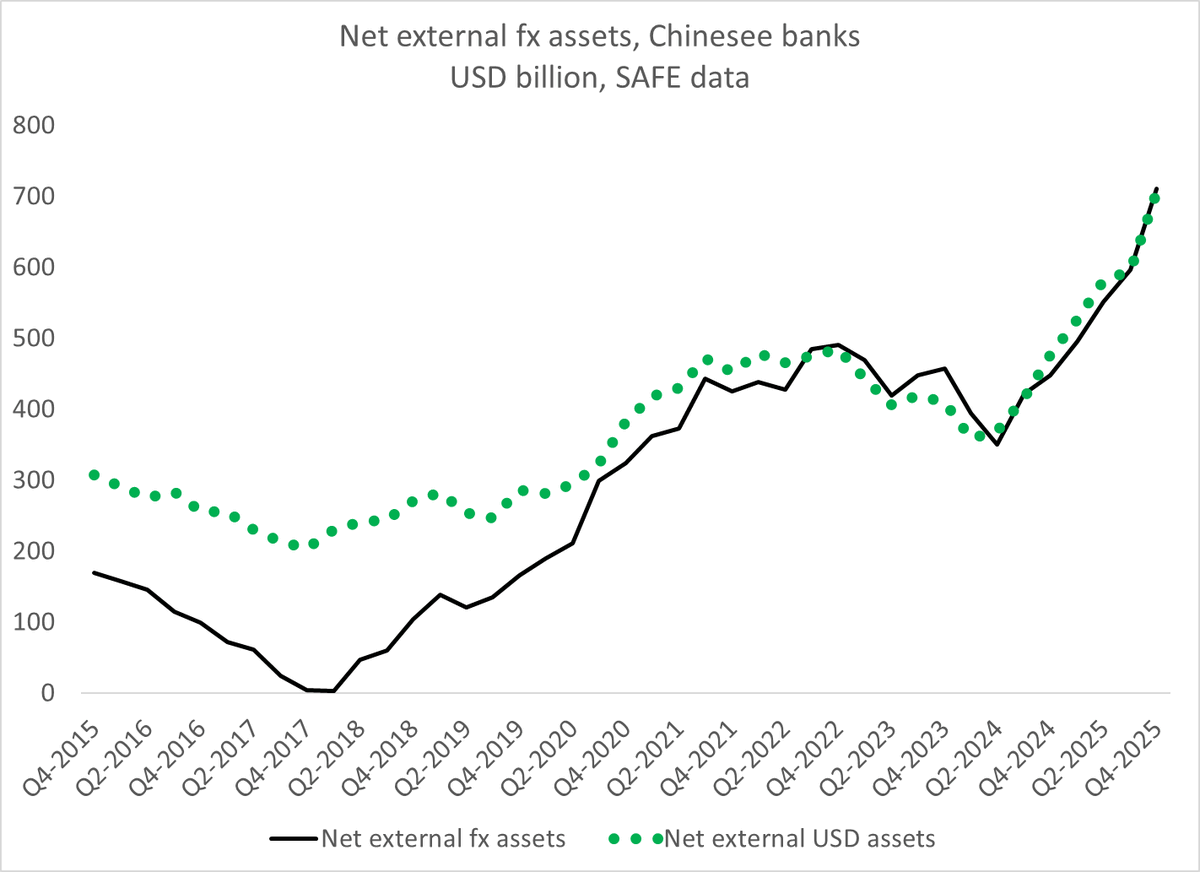

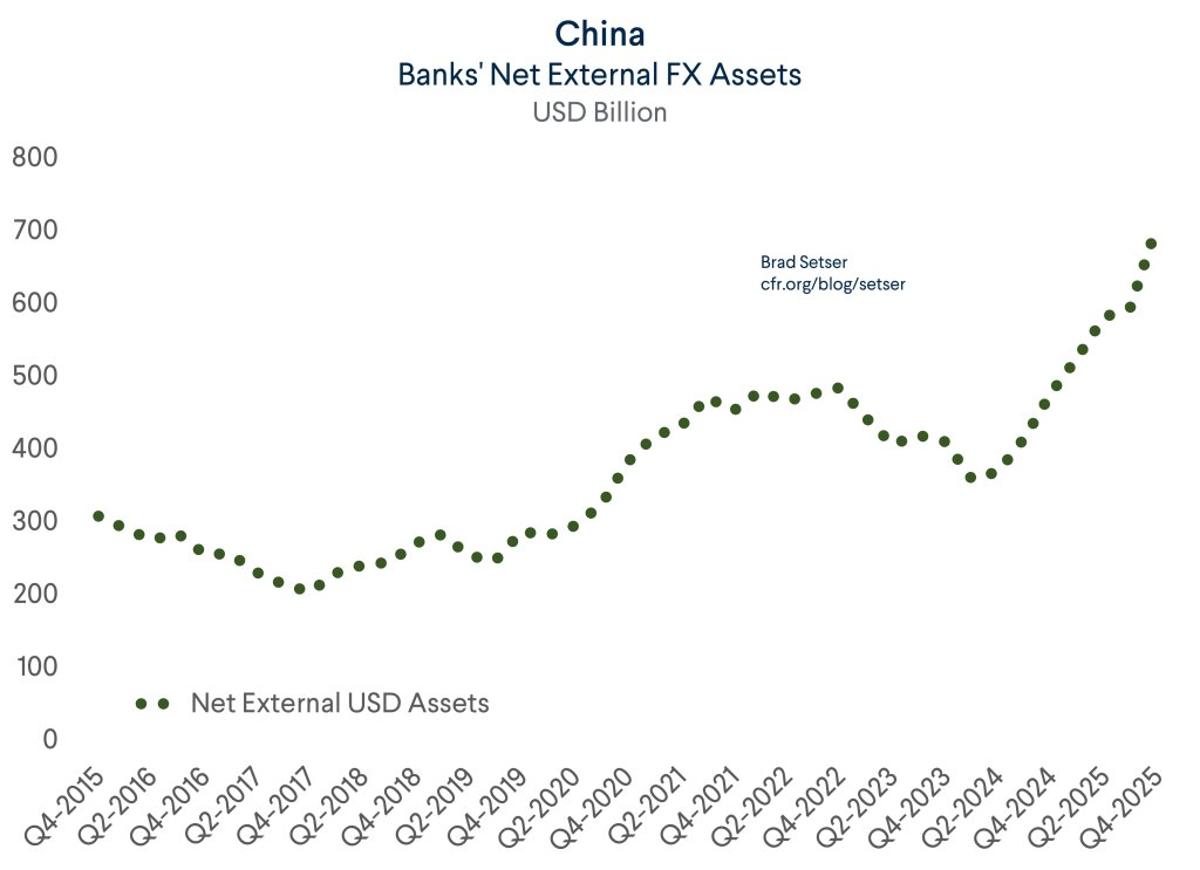

China’s State Banks Hold $1.5 Trillion, Eclipsing Japan’s Reserves

The net foreign asset position of China's state banks (in both dollars and RMB) is now $1.5 trillion -- a rather big sum (close to 1/2 China's formal reserves, a sum bigger than Japan's reserves ... ) 1/ many https://t.co/Rd90nZTcgw

MoF's Dollar Sales Cut Japan Debt, Not Just Spend Reserves

A reminder -- whenever the MoF sells dollar it bought for 80 yen for 155-160 yen, it books a massive profit and reduces Japan's gross debt significantly ... "spending reserves" is a common frame for intervention, but it misses something...

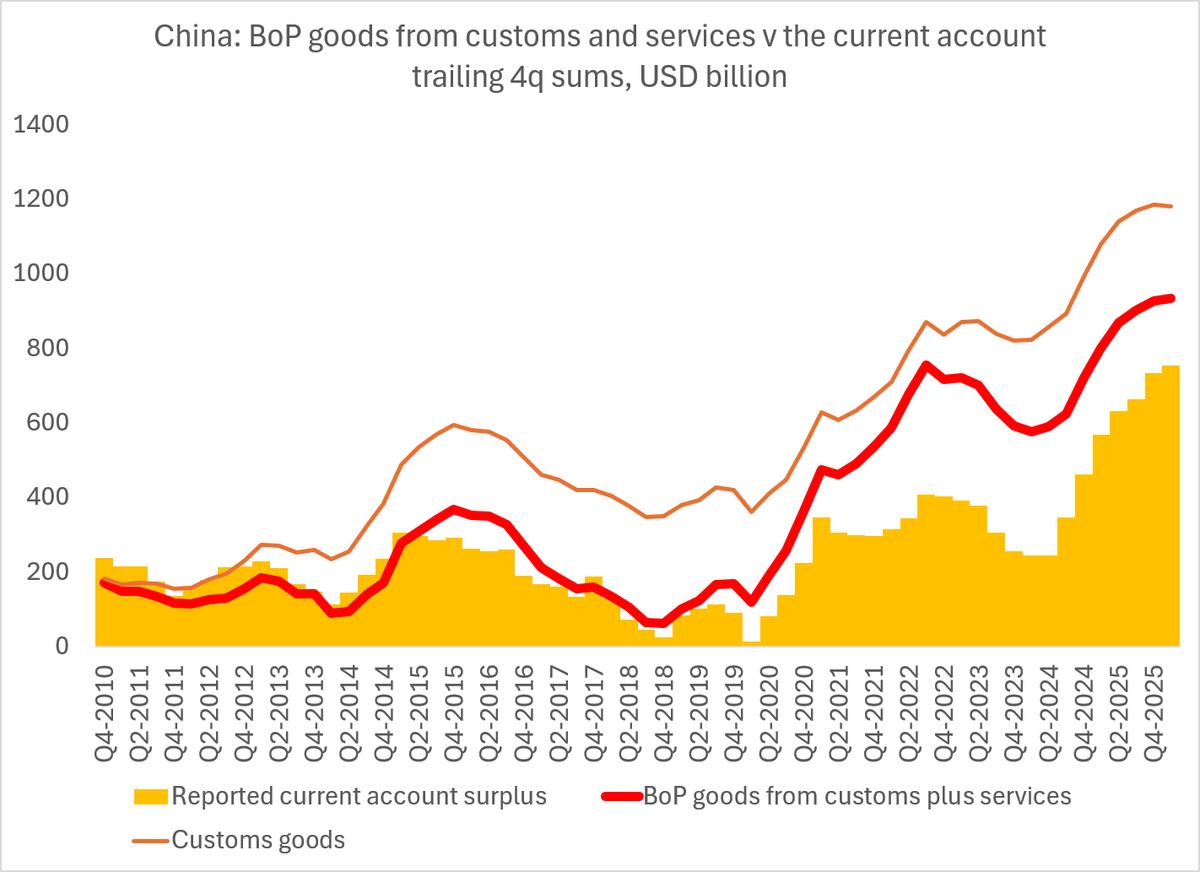

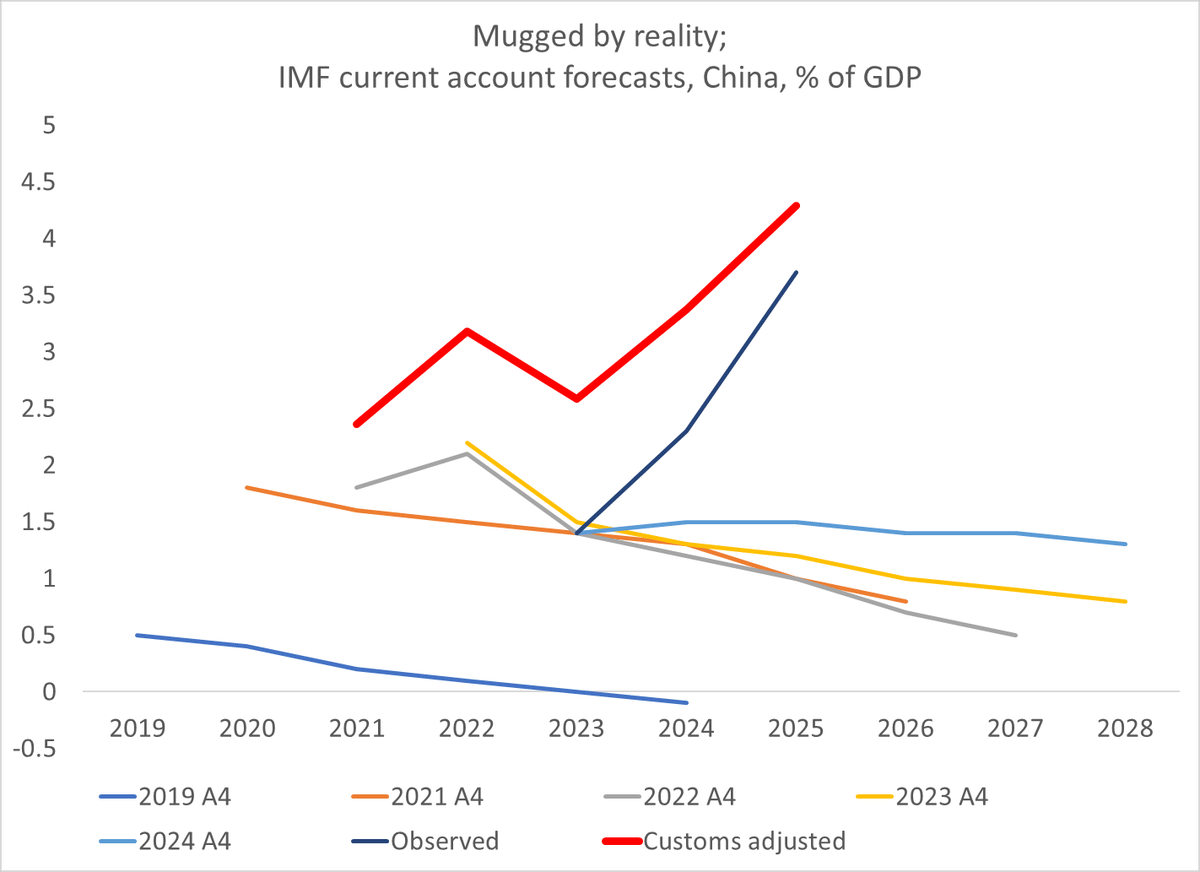

China’s Q1 Surplus Lifts Four‑quarter Total to $750bn

China's $184 billion q1 current account surplus pushed the surplus over the last 4qs of data to $750b -- a sum well short of the just under $1.2 trillion goods surplus/ what the surplus should be, but still a very...

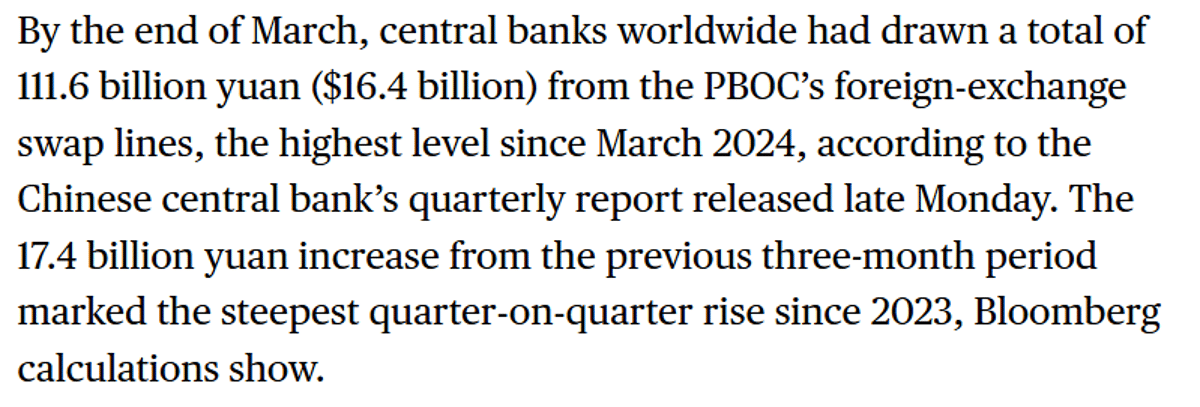

China Ramps up Dollar Swaps to Curb Yuan Rise

Bloomberg is reporting a $3b (CNY 17.4b) increase in the use of PBOC swaps in Q1 ... Que forecasts of dollar doom In the first quarter China (PBOC and state banks) bought $180 of fx to keep the CNY from rising --...

ESF Funds Favor Wealthy Allies,

if the $212b (counting ~ $175b in SDRs that Republicans historically haven't liked using) Exchange Stabilization Fund is going to be given to allies without a financial need (like the UAE) not everyone is going to be able to get...

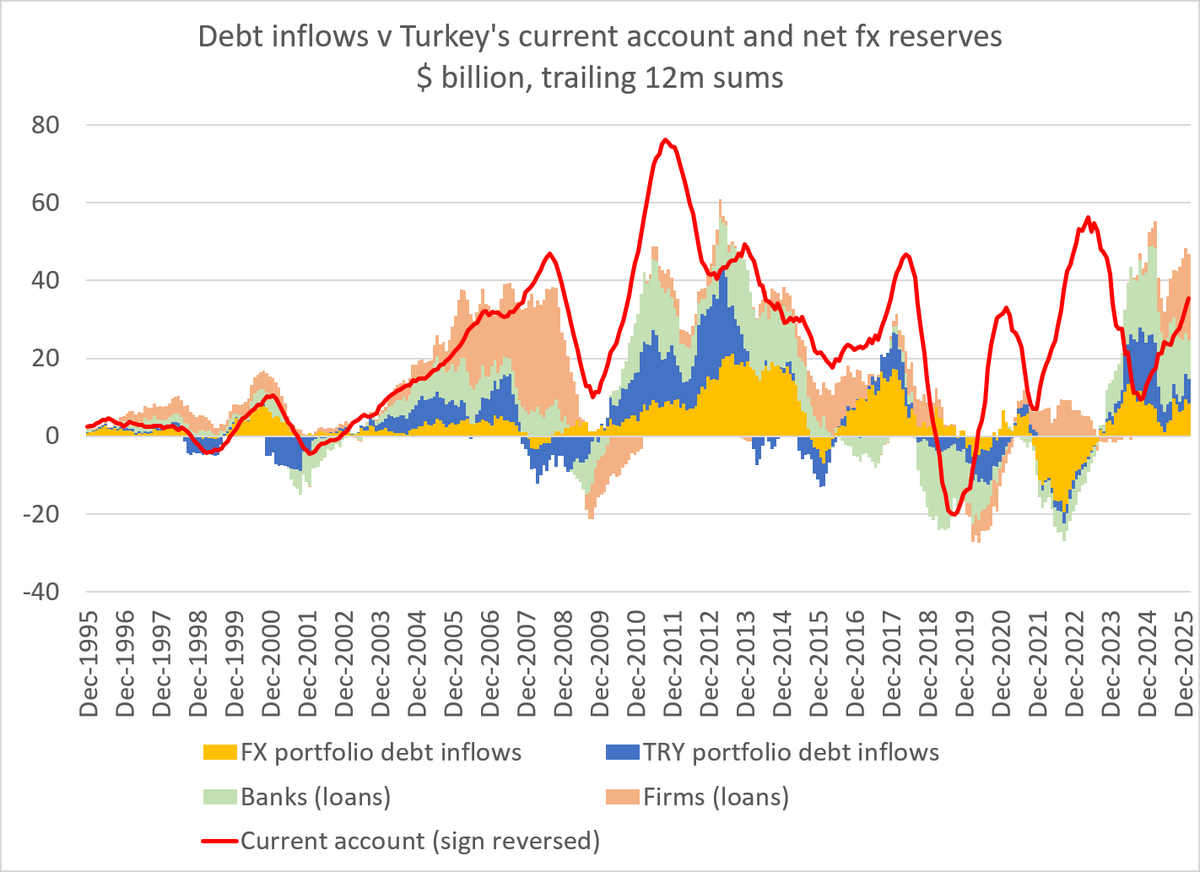

Turkey's Deficit Growing Pre‑Oil Shock, Targets $50B

I think the underlying issue that Bloomberg highlighted is that Turkey's current account deficit was rising even before the oil shock -- it stood at $35b in the 12ms to February, and was on a trajectory toward $50b even if...

Is China’s Reserve Shift Real Insight or Overfit?

Question for @EtraAlex and other students of the TIC data. Is this overfitting to the last known data point, or valuable new insight into where China's reserve holdings appear now that it is minimizing the use of US...

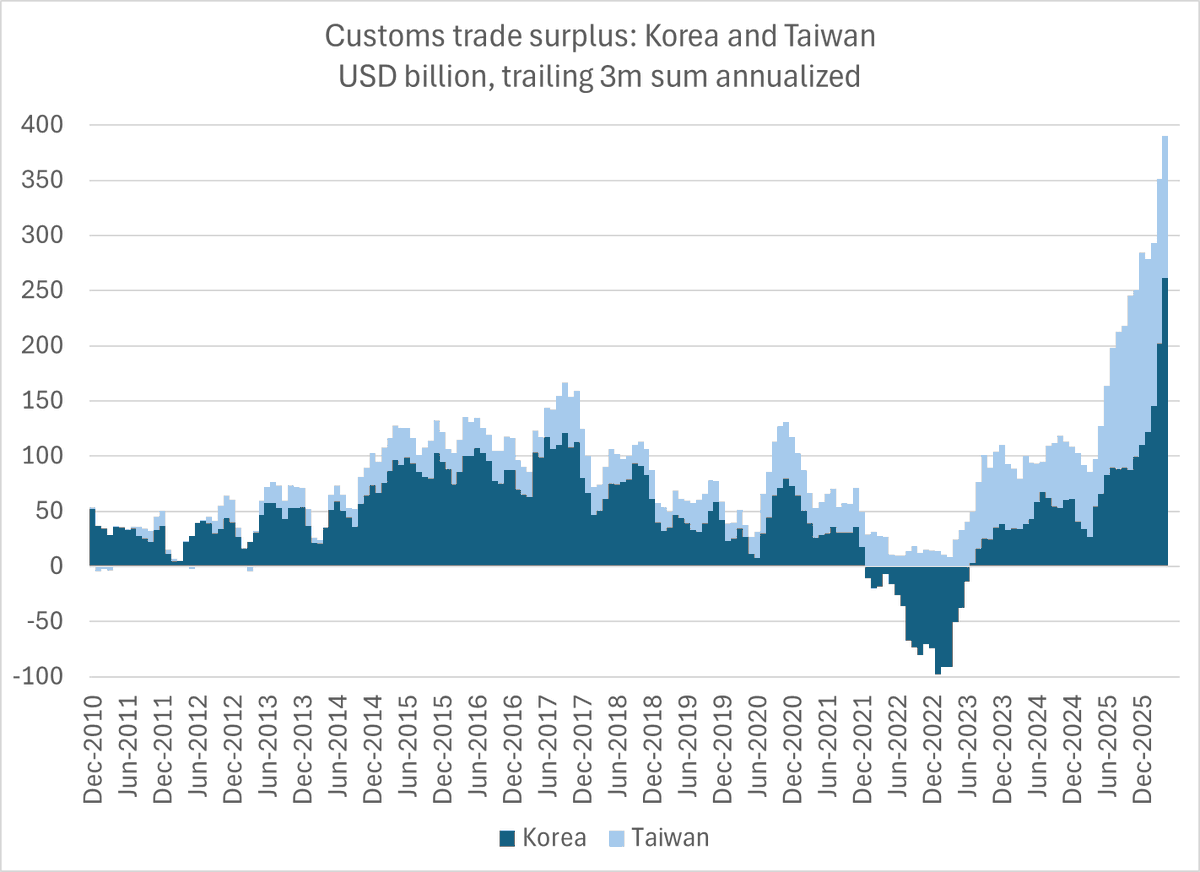

Korea Posts $300B Surplus Amid Record Won Weakness

Two things I never thought I would see: a $300b Korean current account surplus, and a $300b surplus paired with near record won weakness against the US dollar Strange times https://t.co/iSymq2hcGb

IMF Model Shows Yuan Undervalued About 25‑30%

With a realistic current account surplus number (one that takes out the 22 downward adjustment in the goods surplus and uses a realistic estimate of the income balance), the IMF's model would suggest a 25-30% undervaluation

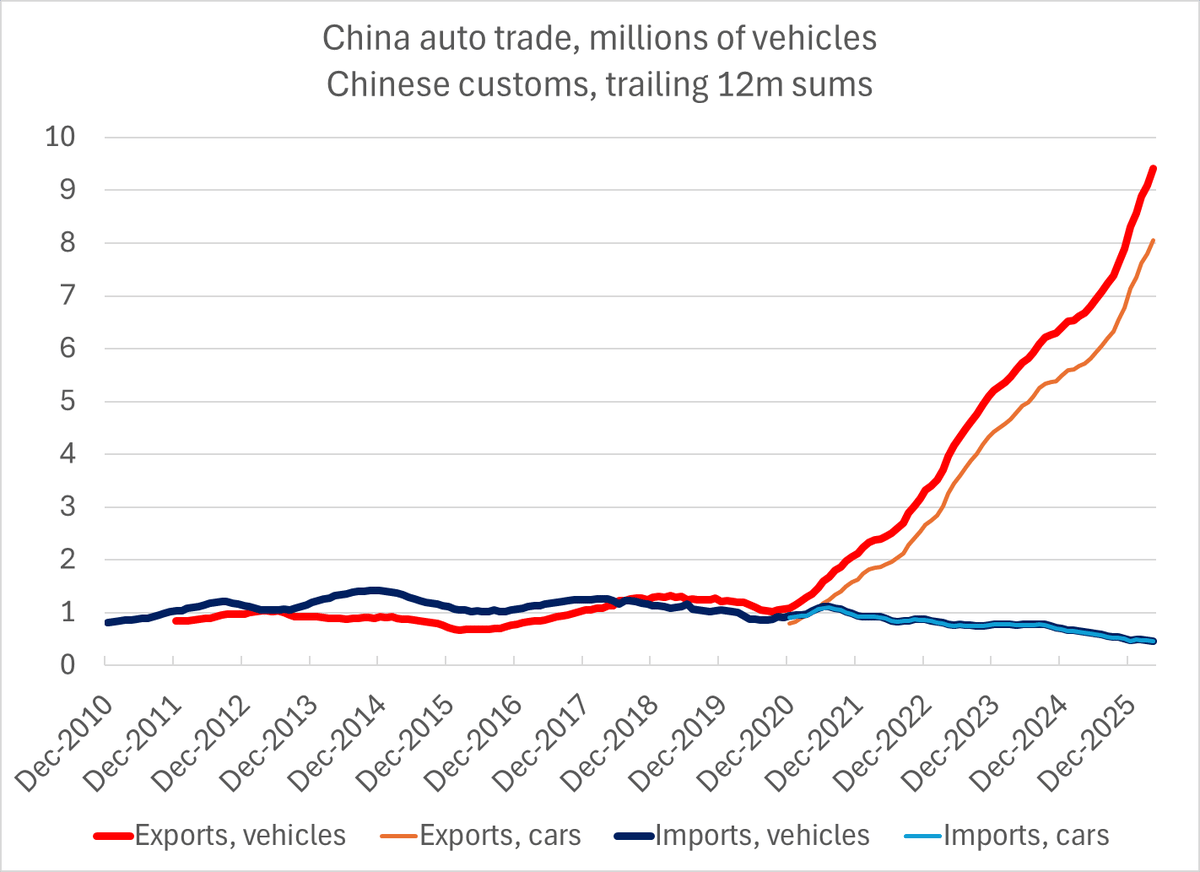

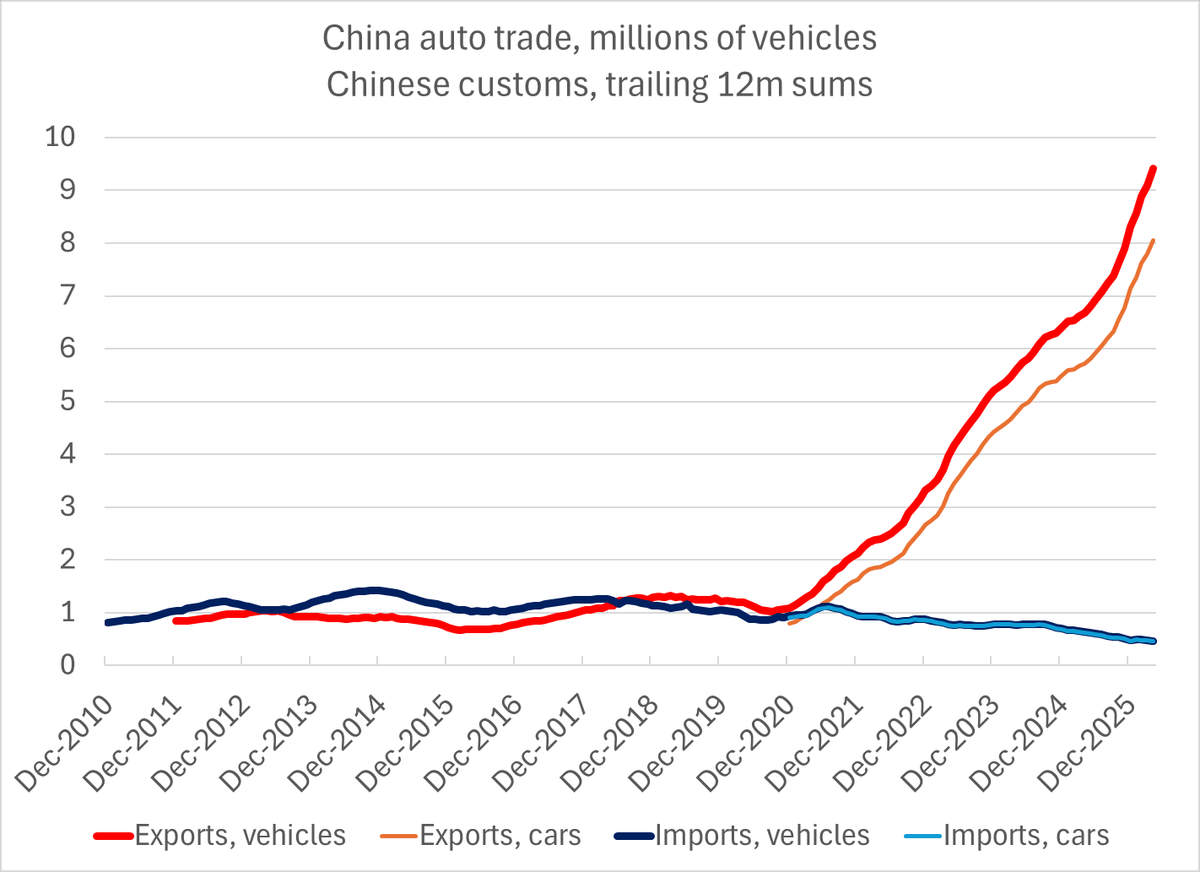

China's Auto Exports Surge While Domestic Demand Falters

China's auto sector is a near-perfect metaphor for China's economy -- domestic demand is down, quite significantly. But exports are on a rocket ship up -- vehicle exports should come close to reaching 12m this year, car...

IMF Misses Surge in China's Surplus, Predicts Decline

The IMF didn't see the big rise in China's surplus coming. In fact, @IMFNews always forecasts that the surplus will dissipate -- From work in progress with Shahin Vallee 1/ https://t.co/Wp2uhY73cS

China Leverages SOEs to Weaponize Import Bans

I am not the first person to observe that when China decides to make a political point by not importing it makes that point forcefully -- by zero'ing out its imports from a specific country. Big SoEs control a...

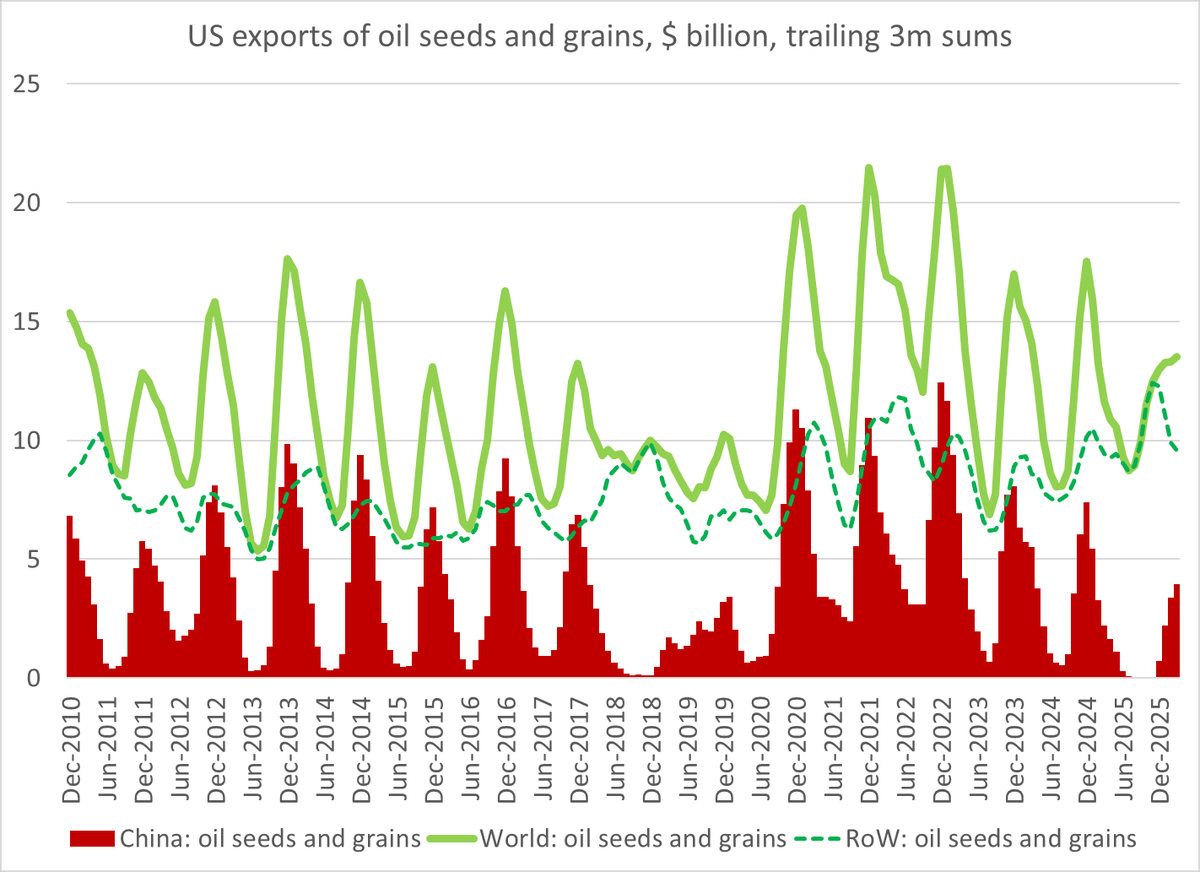

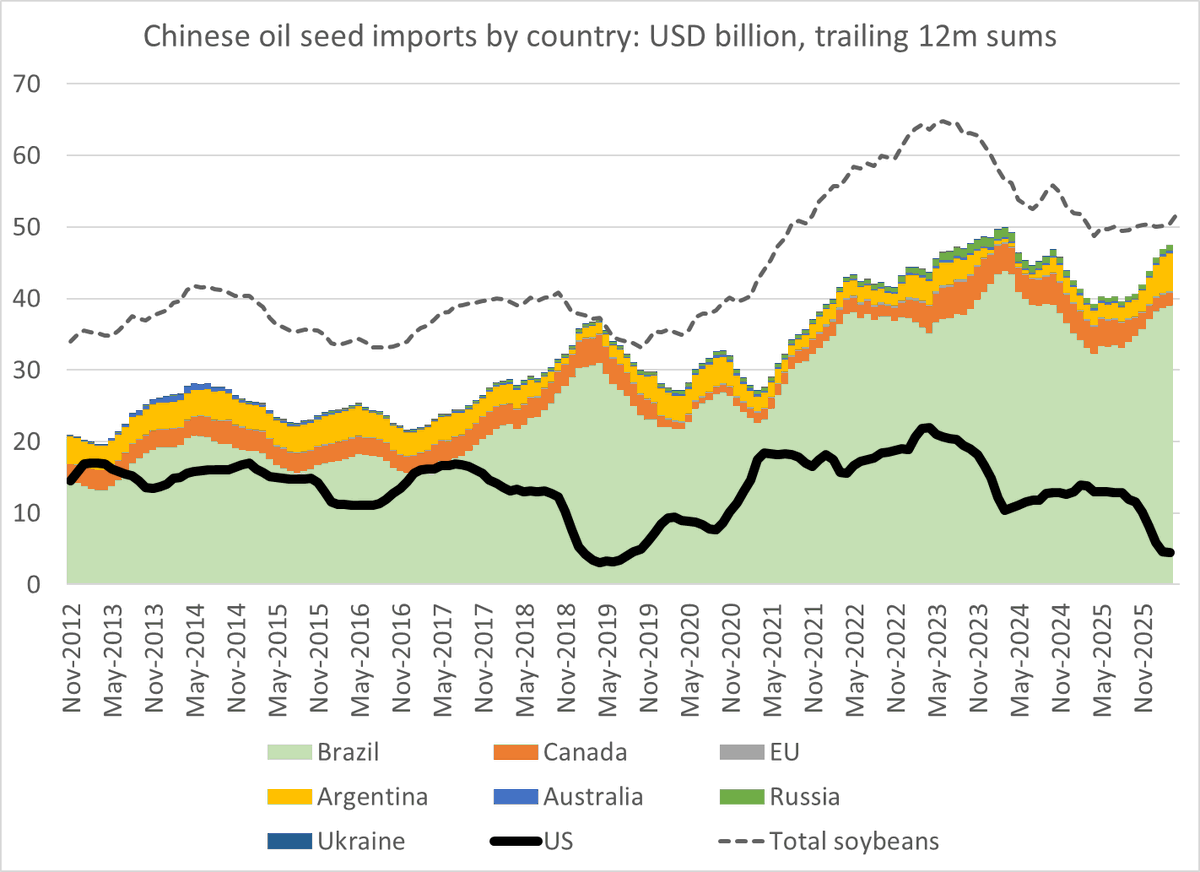

China Uses Trade Deals as Leverage, Creates Hostages

China loves these deals, as they create "hostages" that China can seize if the relationship goes sour -- (of course China never delivered on its "phase one commitments, and it squeezed 'beans hard over the last year) 1/3 https://t.co/54LagYdspc

Questioning Flawed Research on Banks' Dollar Holdings

Mr. Balding needs to back up his assertion here -- What part is wrong? The increase in banks foreign assets? The SCB's rising dollar holdings (in SAFE's data) The policy banks' dollar lending (from AIDdata) 1/2 https://t.co/bGHKNMvvNj

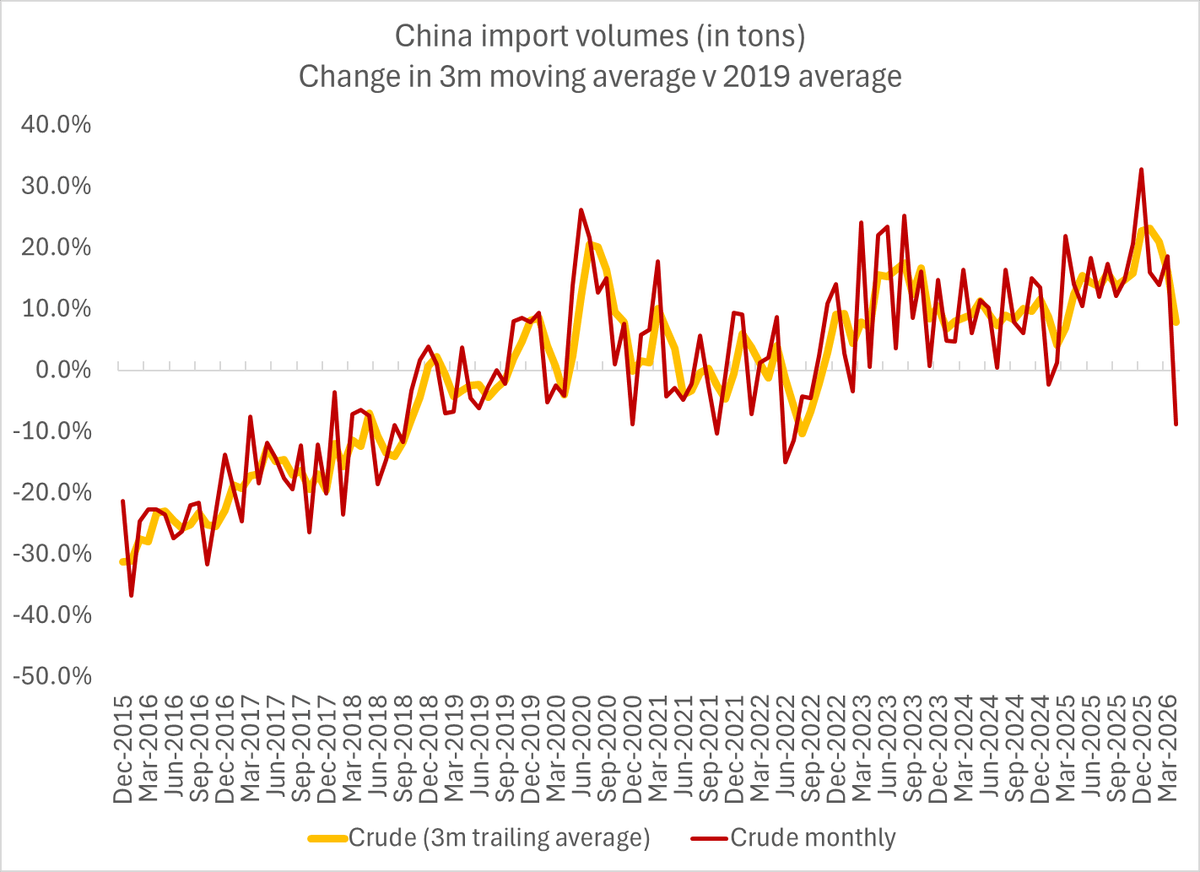

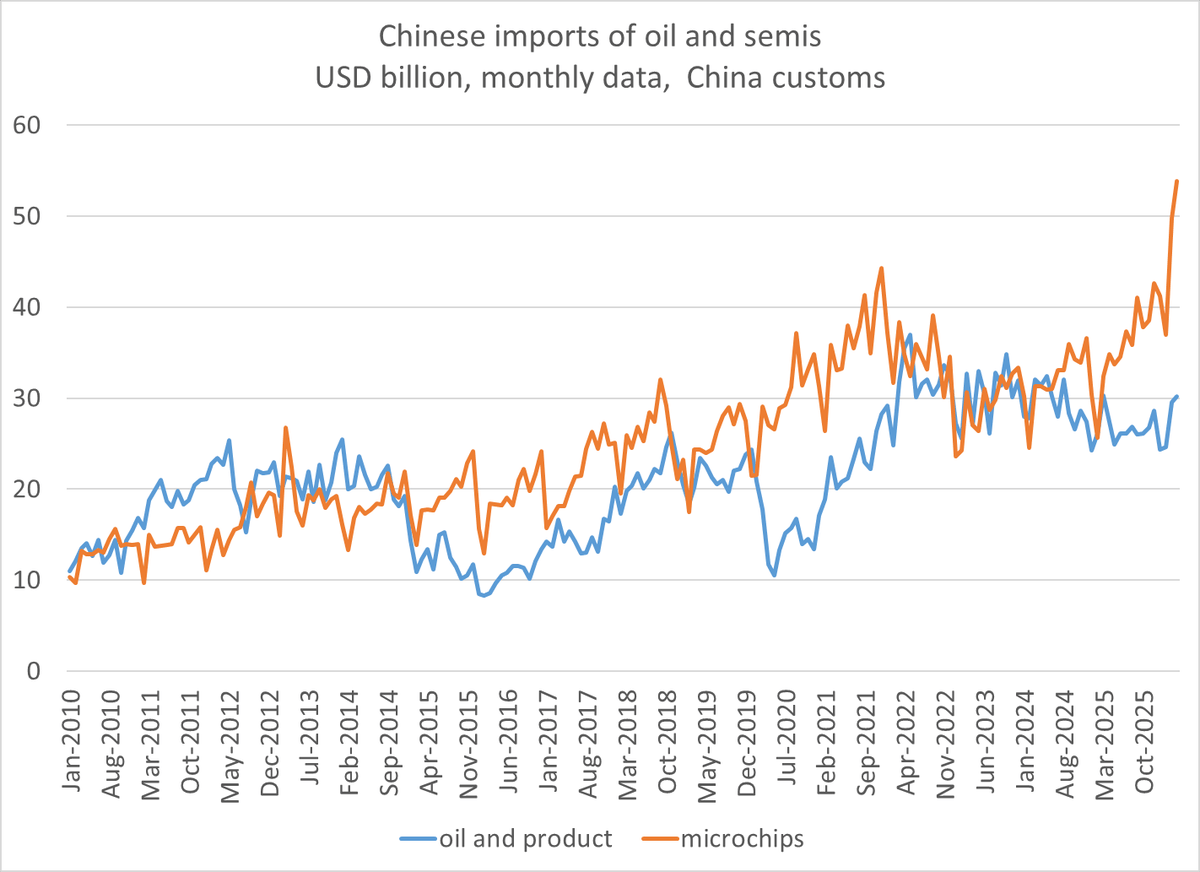

China's April Crude Imports Plunge Below 2019 Levels

Big drop in crude import volumes out of China in April Imports dipped below 2019 levels Clearly helped stabilize the global market (gas imports also down) https://t.co/XJmsiZkLkp

Rising Chip Prices Boost Chinese Export Volume Growth

Estimating Chinese export and import volumes is challenging now, as rising chip prices are pushing up export and import prices -- if March prices carried over, April export volumes were around 15% ... and export volume growth is accelerating at the...

China’s Chip Imports Surge to $50B, Oil Stalls

If you want to sell to China, it sure helps to make chips -- at least right now. April chips imports topped USD 50b Note the lack of any bounce in oil imports in dollars terms as well 1/ https://t.co/sc6I5sL5uw

China's Vehicle Exports Surge 50% to 12 Million

50% y/y growth in vehicle export volumes pushed China's April vehicle exports to an annualized pace of 11.2 million. Full year exports could reach 12m, passenger car exports are on track to to 10m -- 1/2 https://t.co/7rRg8aSumT

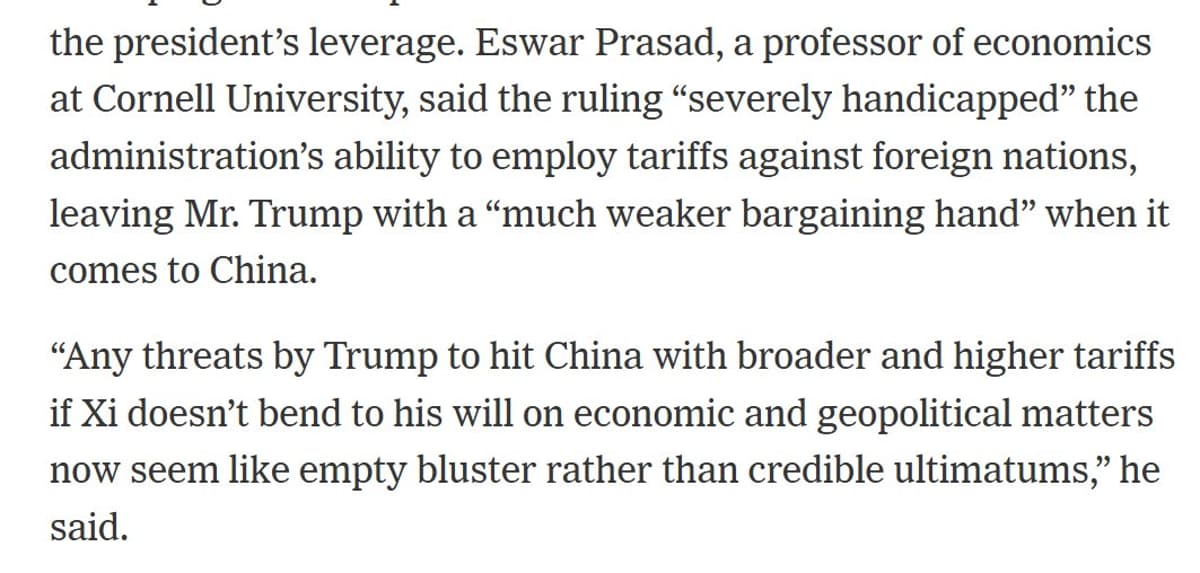

Setback Targets Global Tariff, Not US‑China Talks

Will push back a bit against Dr. Prasad's take here, and the NYT headline framing the "122" decision as a set back for the US in the negotiations with China. The actual set back is to any attempt to generate a...

Korea, Taiwan Post Record Surpluses Amid Currency Weakness

The surpluses of Korea and Taiwan this year will be incredible The fact that these surpluses coincide with a historically weak Korean won and continued deep weakness in the Taiwan dollar is most interesting

Administration Fails to Meet 1974 BoP Deficit Standard

Great thread, and an interesting observation -- There is no doubt that the Administration didn't attempt to meet the standard for 122 (a BoP deficit as understood in 1974 ... ); the USTR filing more or less just noted the deficits...

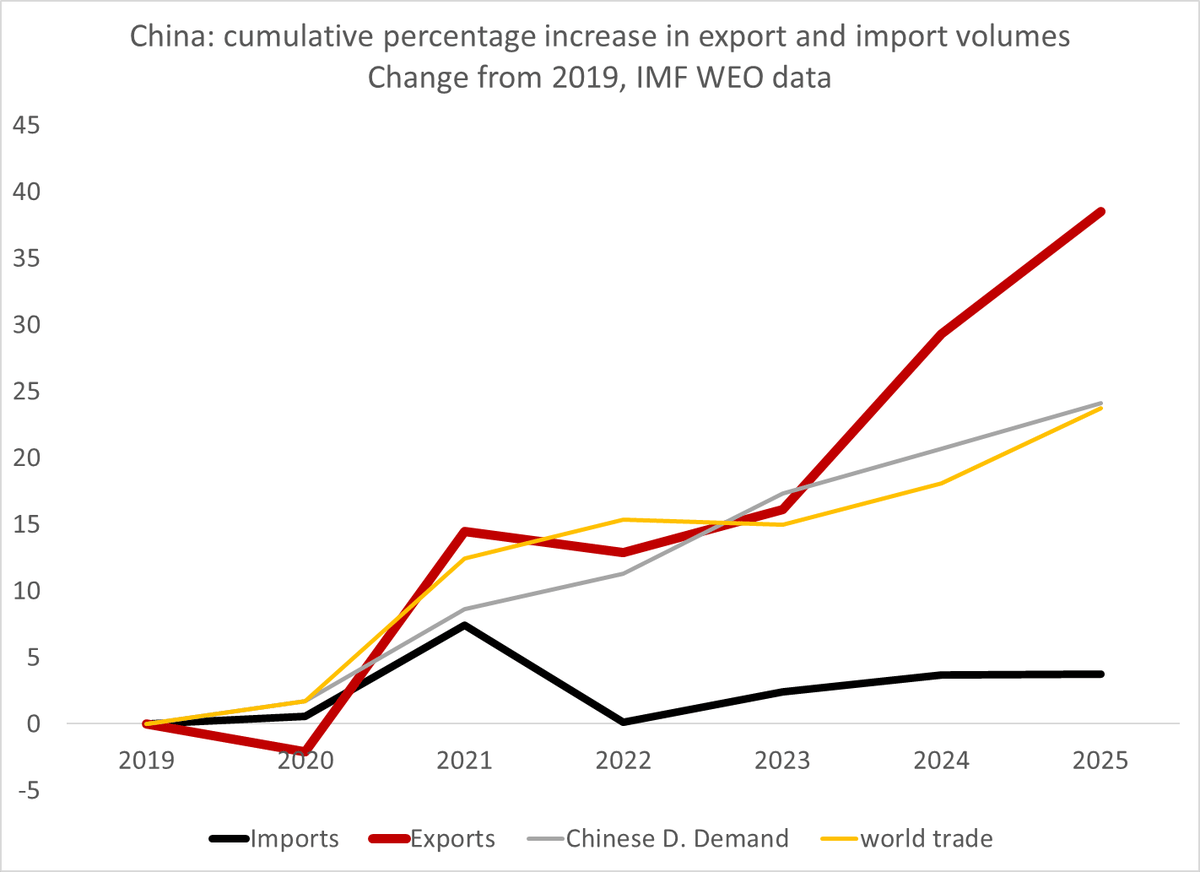

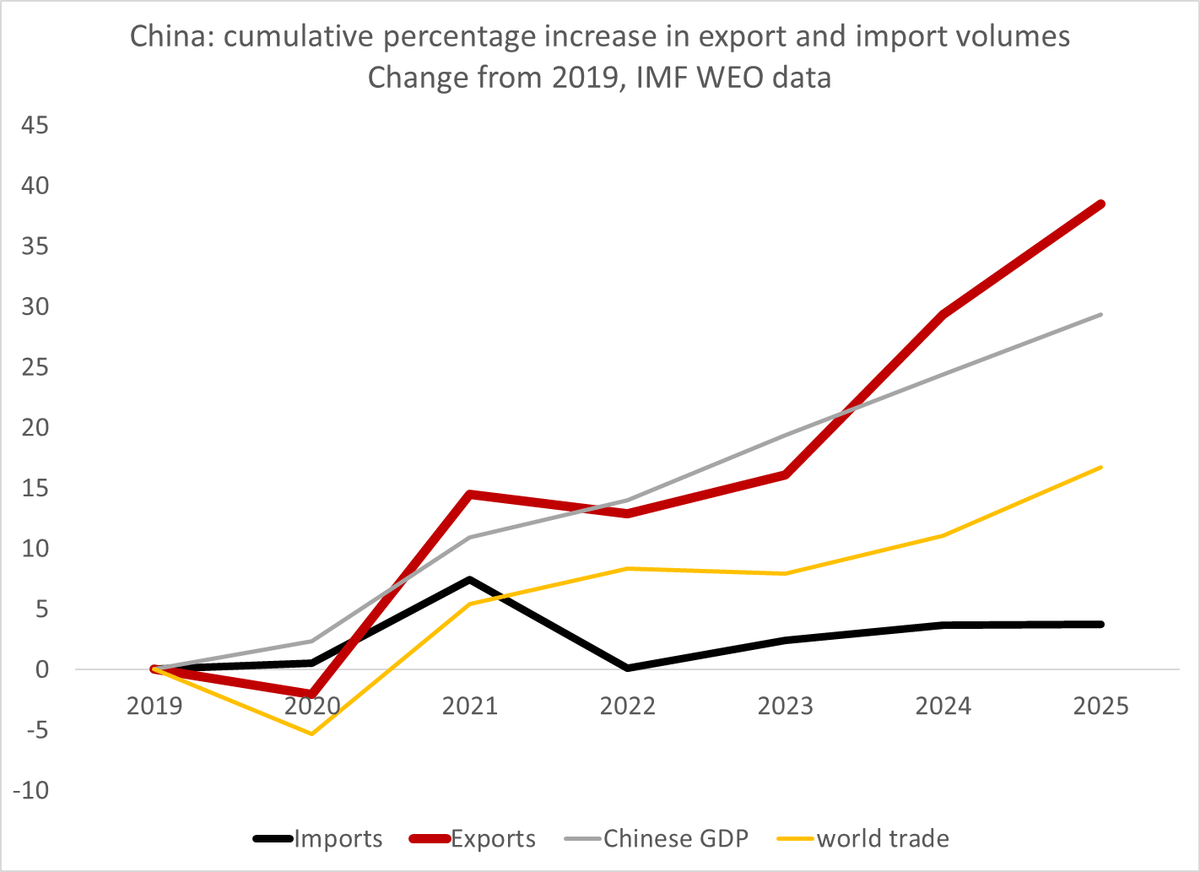

China's Imports Stall While Exports Surge, Creating Trade Imbalance

Chinese import growth has stopped tracking with Chinese domestic demand growth. With Chinese export volumes growing much faster than global trade, there is now enormous gap -- an imbalance -- in China's trade https://t.co/BhObwF49bG

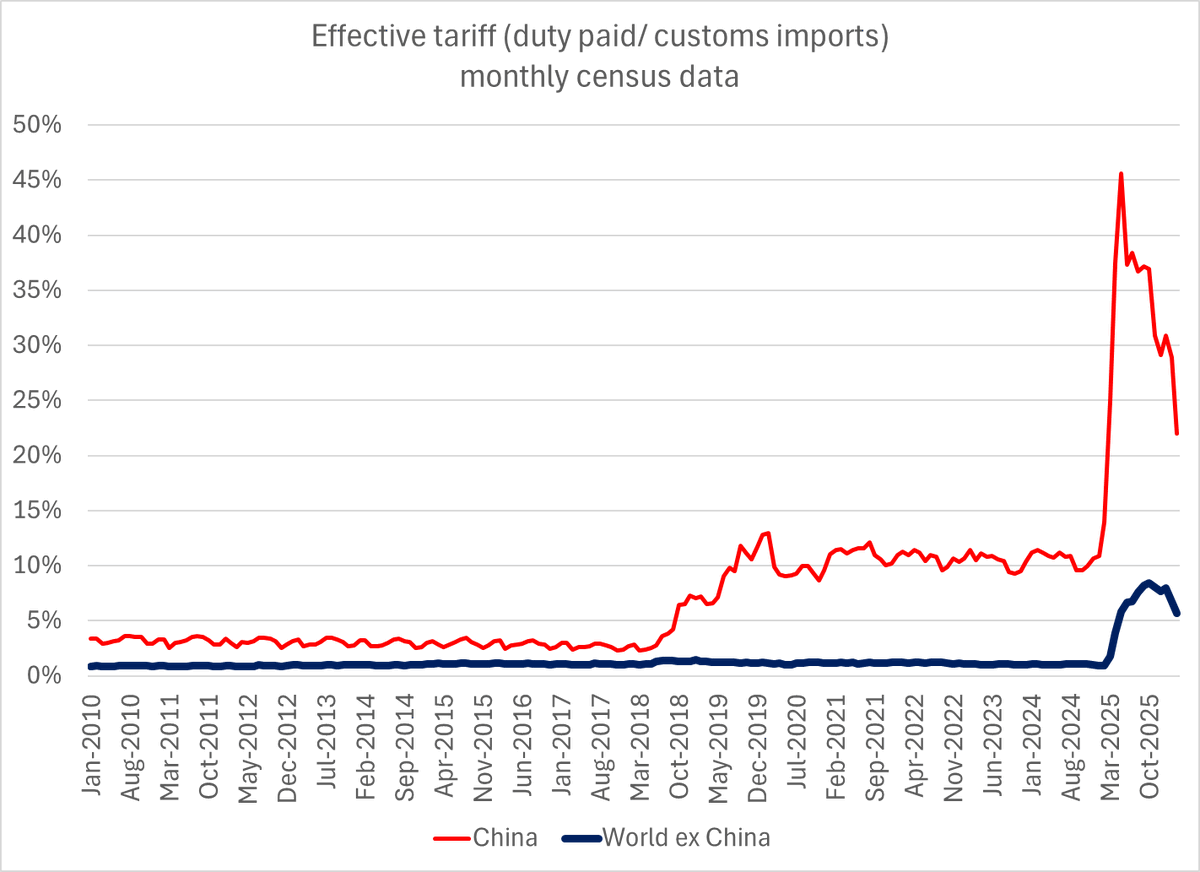

China’s March Tariff Triples Global Average After IEEPA End

In March, the simple effective tariff (tariff revenue/ imports) for China was a bit over 20% -- and the simple effective tariff for the rest of the world was 5%. The end of IEEPA had an impact 1/2 https://t.co/URjXF3lbbB

Korea and Taiwan's Chip Trade Surplus Soars $300B

The combined trade surplus of the chip superpowers (Korea and Taiwan) is running about USD 300b above its 2024 level ($400b v 100b). Taiwan's April surplus was down a bit (oil and gas imports) but it didn't change the...

China’s Imports Trail Global Trade and GDP Growth

in volume terms China's imports have lagged both global trade and China's reported GDP growth bigly https://t.co/GytLVBfdJq

Peter Harrell Nails

Hard to beat Peter Harrell's take on the Court of International Trade's ruling on the section 122 tariffs -- 1/ a few

Call Out China Threat, Drop “Imbalance” Rhetoric

Hauge to me and Pettis: "Don't hide behind the language of "imbalances." If you think China is a competitive threat and that wealthy nations should actively use industrial policy to keep it at bay, say so" I object to the idea...

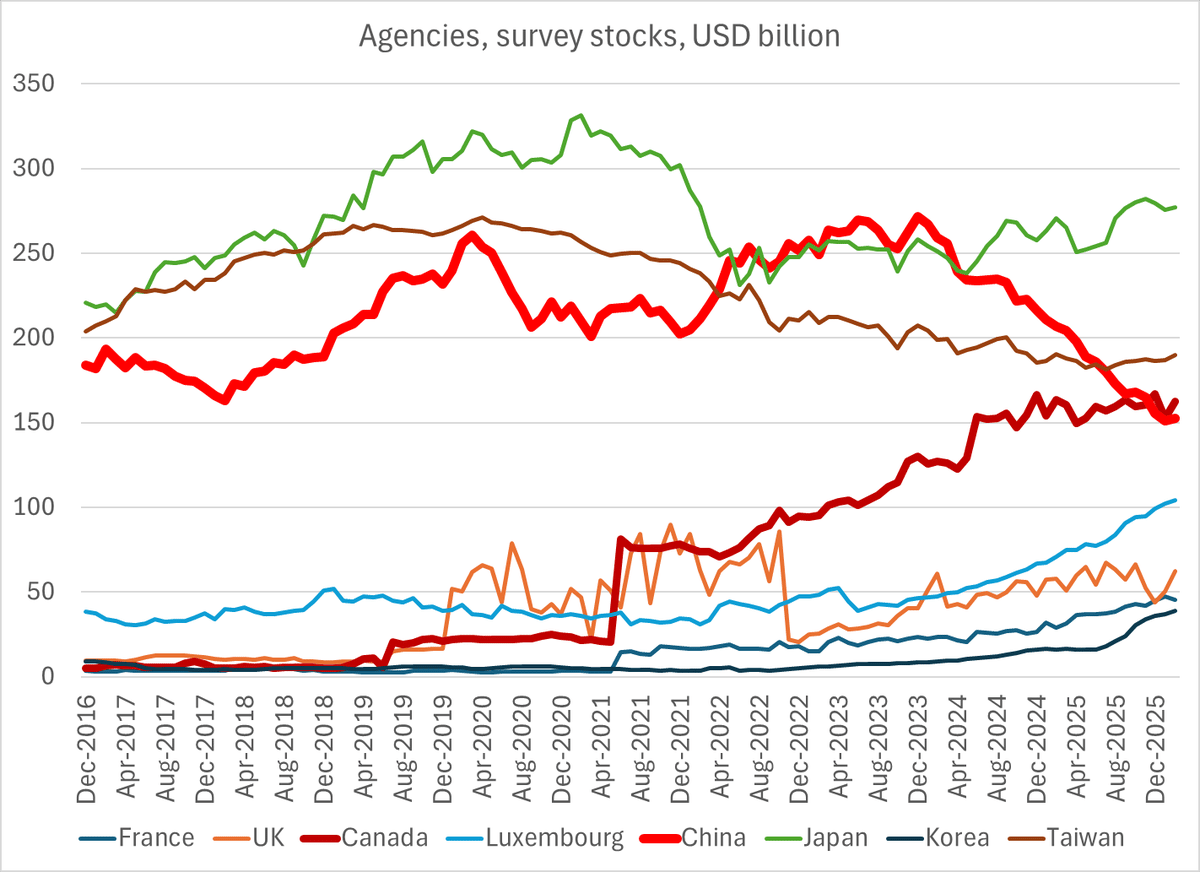

China’s Agency Holdings Drop, Canada and Europe Gain

A little fun with the TIC data -- China's Agency holdings are down a lot the last few years: they are now about 150b v a peak of over 250b. But there is more going on to. Canadian holdings are up...

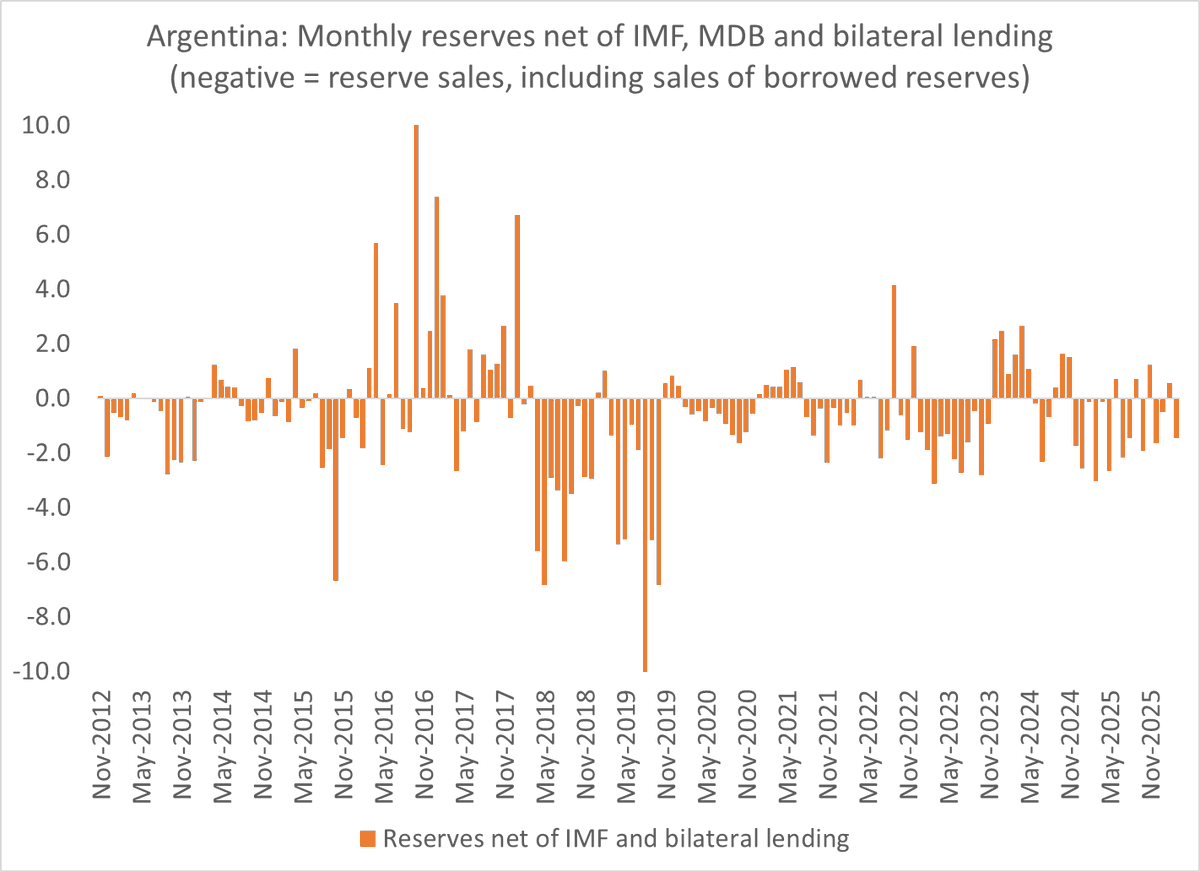

Milei's Fiscal Discipline Stalls Without FX Reserve Growth

Milei's commitment to fiscal balance (aided by a relatively low interest burden) is clear -- His kryptonite has been Argentina's inability to generate a sustained increase in its foreign exchange reserves 1/ https://t.co/yJLGDJnIV8

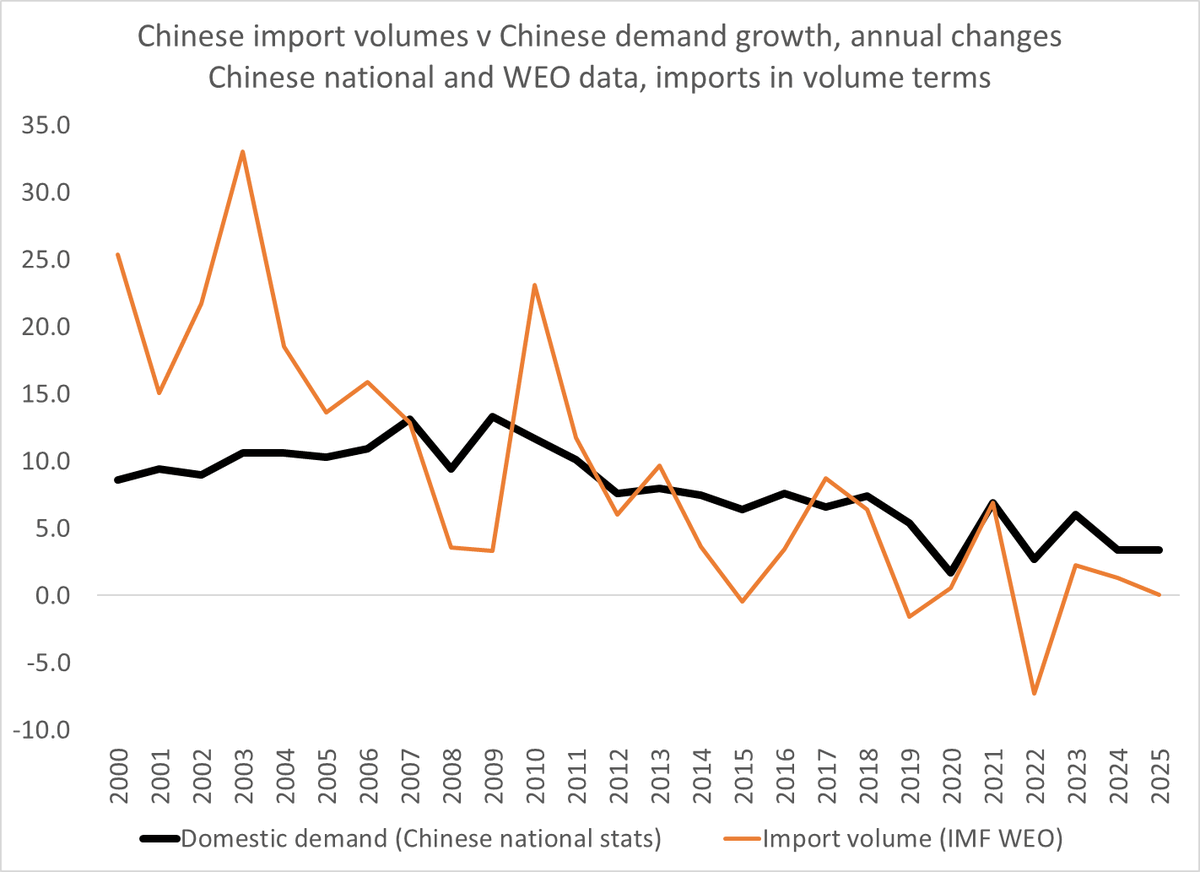

China’s Imports Lag Behind Domestic Demand Since 2012

One important stylized fact about the Chinese economy that doesn't get enough attention -- import growth has lagged domestic demand growth since at least 2012, and arguably since 2007 or so 1/3 https://t.co/K5wsTUcAhf

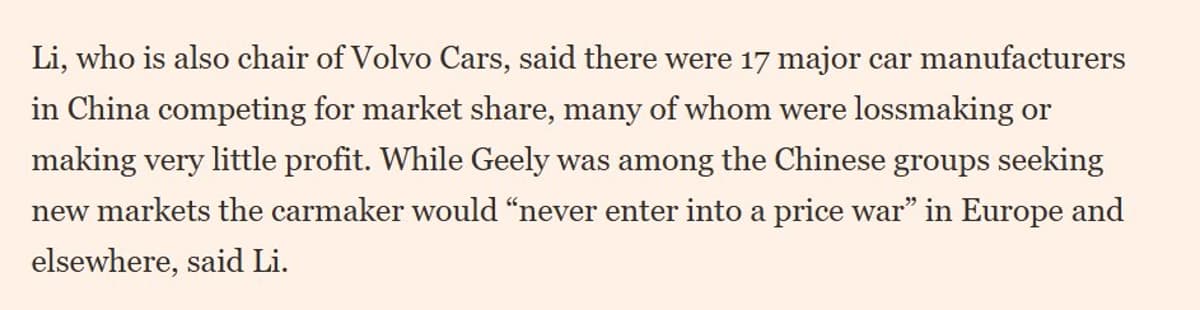

Li Shufu: Most Chinese Automakers Still Unprofitable

Li Shufu = founder of Geely Holding/ owner of Volvo Cars told the FT many [Chinese car manufacturers] ... "were lossmaking or making very little profit" https://t.co/b9aO9GoKOZ

Chinese Automakers Face Excess Capacity, Seek Overseas Markets

Guess I should have said shrinking industry margins rather than summarised for stiklers for accuracy like Glenn: " In China alone, experts estimate annual demand of about 25mn cars against estimated factory capacity of 45-50mn. The prolonged price war and eroding...

Glenn's Arrogance Masks Repeated China Trade Misconceptions

Glenn's arrogance is incredible given his long history of clinging stubbornly to inaccurate arguments (no overcapacity in China's exports, China doesn't "really" have a trade surplus, SAFE produces accurate BoP that no one outside China should challenge ....) 1/

US Hypocritically Slaps Auto Tariffs While Condemning EU Protectionism

Not sure the US can criticize the EU for protectionism with a straight face .... Really bad talking point when the US is raising tariffs on autos in a way that clearly violates the EU-US trade trade framework. Embassing TBH

Trump Admin Abandons Trade Deficit, Ignores AI Import Tariffs

Guess the Trump administration has lost interest in bringing the trade deficit down. Fair enough; tis clear that they aren't going to tariff the imports central to the AI boom ... 1/2

U.S. Reexports Q1 2025 Gold Over Tariff Fears

Nope. We are reexporting gold that came into the US in q1 2025 out of fear of potential gold tariffs ... 1/2

Eurodollar Market Independent of Dollar

Disagree here obviously -- The modern eurodollar market developed independently of dollar pegging; the UK is the market's hub and the pound obviously isn't pegged to the dollar ... 1/2

AI-Driven Import Surge Widens March US Trade Deficit

US imports are soaring again -- led by imports related to the "AI"/ data center investment boom. That pulled the March trade deficit up even with strong exports .. 1/ https://t.co/pyJlnGeCph

China's Banks Surge Net Dollar Holdings, Data Shows

Indeed. China's own banking data shows a big jump in its net dollar holdings in the last few quarters. And that data excludes the dollar assets of the policy banks and China's various sovereign funds https://t.co/DSd2RXCiOA

High LNG Prices Curb China's Imports, Freeing Supply Globally

Zero signal about China here China is a discretionary LNG importer. It can generate with dirtier domestic coal if needed. High prices generally mean lower imports. Helps globally -- China is freeing up LNG for folks...

EU Poised to Scrap Turnberry Deal Amid Weak 301 Case

Gives the EU an excuse to tear up Turnberry deal and retaliate in a world where Trump lacks the ability to use IEEPA to raise tariffs on everything overnight. The 301 case against the EU's overcapacity was rather thin -- 1/2

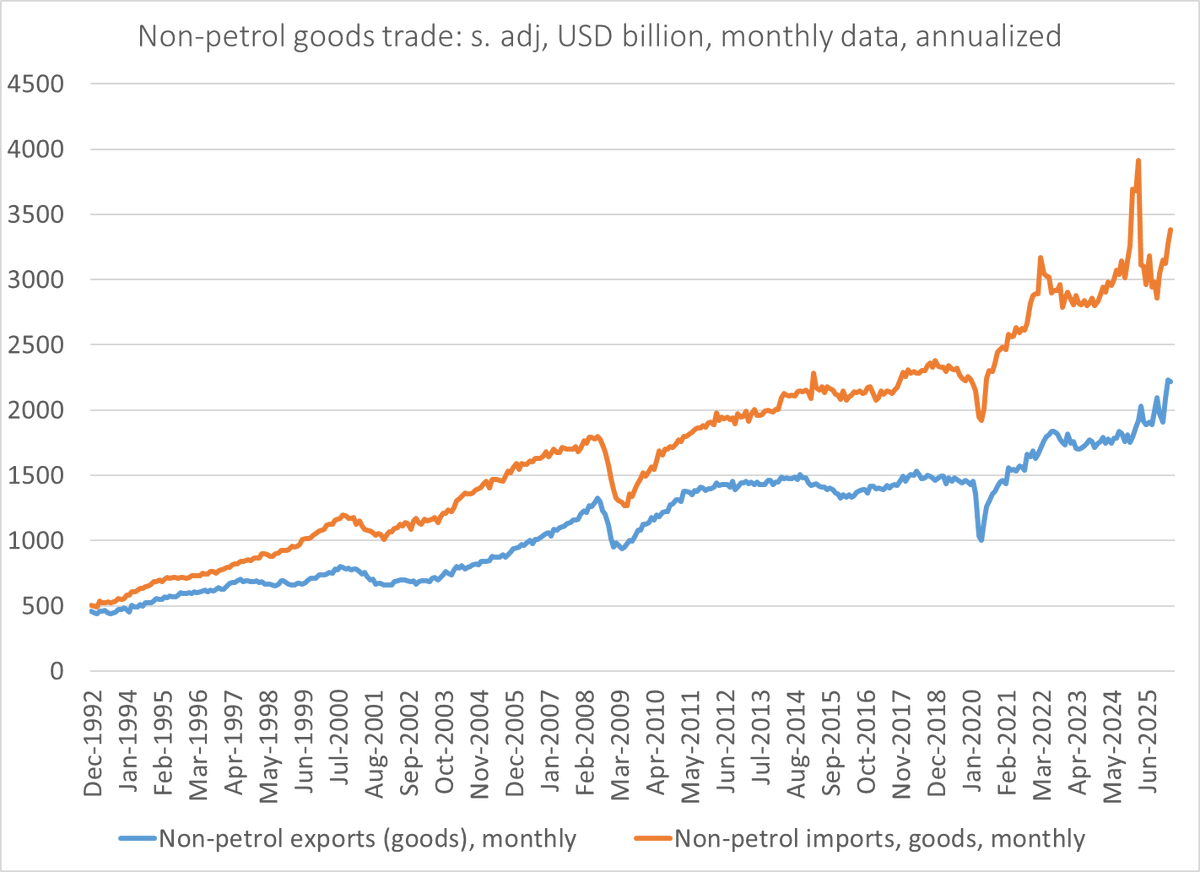

Export‑Import Gap Surges Post‑COVID, Spike After 2020‑21

The gap between imports and exports actually widened much more in 24 and 25 than during the COVID years. and my argument was in fact that there was an important break in 20-21, tied to the property market...

Japan's FX Trade Slashes Net Debt, Cuts Gross Debt

Alternative framing for Japan's intervention Japan sold $35 billion of dollars bought at around 80 yen the dollar for close to 160 yen, booking a massive profit that reduced Japan's net public debt -- and in the process brough Japan high...

GCC May Leverage Insecurity for Cheap US Funding

Very much agree and it wouldn't totally surprise me if the GCC countries are trying to play on that insecurity to get a bit of cheap funding from the US ...

U.S. Treasury Can't Afford Gulf Family Oil Bailouts

The US Treasury is too poor (and has too few reserves) to bailout -- or even provide a swap to -- the very rich Gulf family oil and investment businesses ... With @StephenPaduano https://t.co/Wz3bR4fXlH

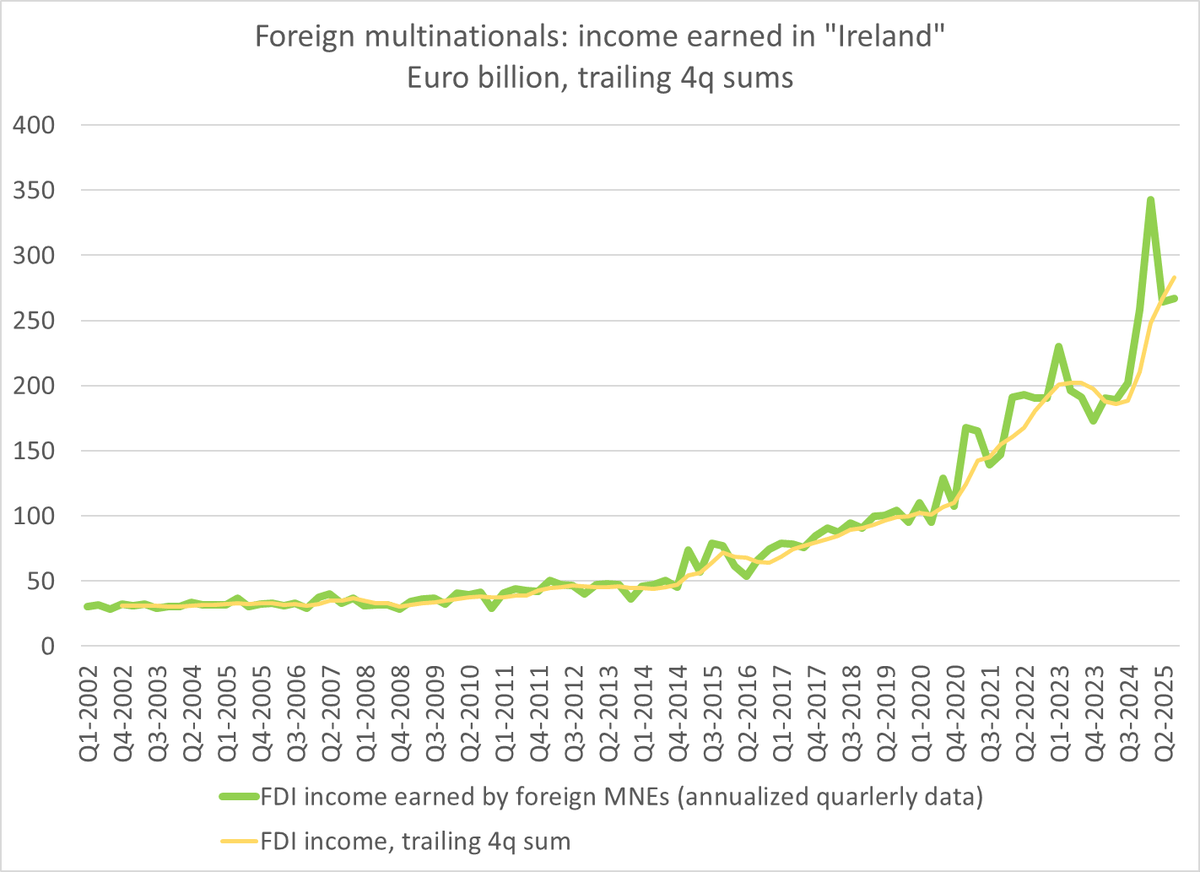

IMF Must Strip Tax‑Avoidance Distortions From Its Data

The IMF really needs to learn how to adjust its numbers to take out the distortions from tax avoidance (i would recommend some TA from Irelands own sttat office) https://t.co/i9z6sT14fo

America’s Data Centers Still Rely on Foreign Imports

A rather aggressive way of framing the fact that the US still heavily relies on imports for building out data centers -- and that a surge in investment demand for advanced manufactures largely flows to the rest of the world