JunkBondInvestor

Credit analyst focused on high yield bonds, leveraged loans, and distressed/special situations with frequent deal/document analysis.

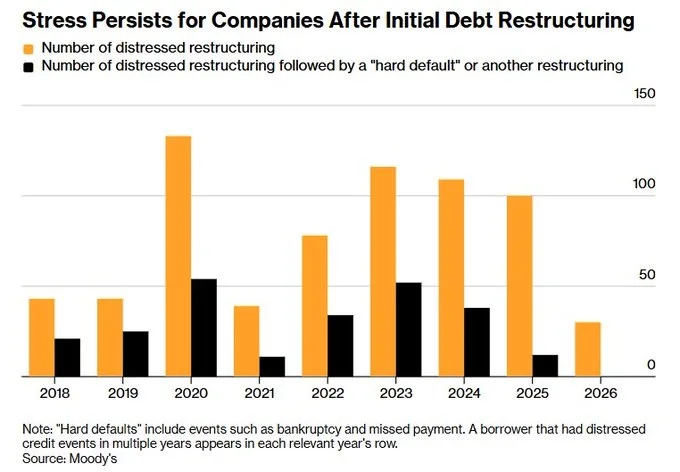

Distressed Exchanges Lead to Hard Defaults, Not Chapter 11

Moody’s on distressed exchanges: > 35%+ end in hard default or another rx > Credit events after a rx typically hit within 3 years > 65% of last year’s defaults were distressed exchanges, not Ch. 11 The 2023 cohort is up next

Spirit's Double Bankruptcies Cost $110M, Left 17k Jobless

Spirit Airlines filed bankruptcy twice in one year and spent $110M+ on advisors. The first Chapter 11 cost $33M and changed nothing. The second is at $80M (still billing) and ended in liquidation. 17,000 employees out of a job. The advisors will...

KKR Injects $150M, Backs FSK Amid Q1 Slump

$FSK Q1'26: > NAV -9.9% > Non-accruals: 3.4% -> 4.2% > Dividend cut from 48c to 42c KKR's response? $150M in preferred equity. $150M tender offer at $11. Plus a $300M buyback authorization and KKR waiving its incentive fees for 4 quarters.

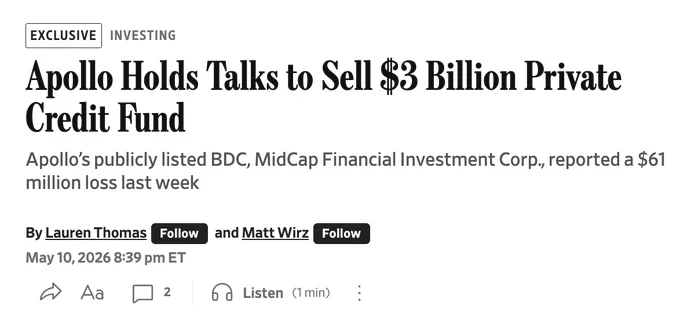

MFIC Defaults Surge; Apollo Seeks Private Buyer

MFIC defaults jumped from 3.9% to 5.3% in one quarter. Stock at 0.85x NAV. Mostly stopped new lending. Using cash from repayments to buy back stock and pay down debt. Now Apollo is trying to sell it. This is what BDCs do...

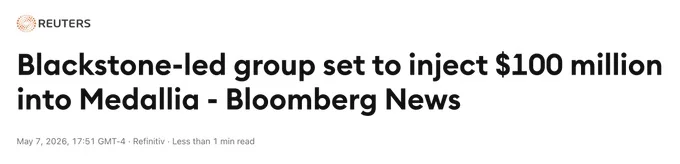

Lenders Convert to Owners, Inject $100M Into Medallia

Somehow I missed this. The lenders are writing a $100M equity check into Medallia. Started as senior secured creditors. Now they own the company and are putting more money in. Never a good sign.

AI Infra High‑Yield Bonds Double, Outpace 2025 Forecast

High-yield bond issuance for AI infra: 2025 full year: $13.5B 2026 YTD (through April): $26.6B Already doubled last year's total and ahead of most full-year estimates Source: Pitchbook

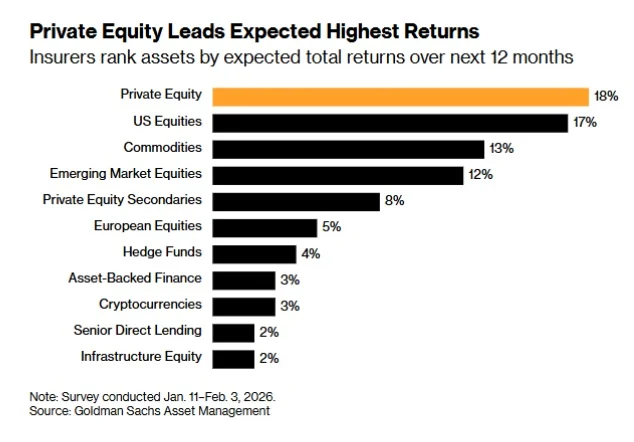

Senior Direct Lending Returns Shrink to Risk‑Free Levels

Goldman survey of insurers on expected 12-month returns: PE: 18% Crypto: 3% Senior direct lending: 2% Sold for years as high single digits with downside protection. Now it's just the risk-free rate without the risk-free part

NMFC's 65‑cent Loan Profit Raises Seller Mystery

NMFC bragging about a loan they bought at 65 cents. It’s now at 75. Mgmt is telling investors the strategy is paying off. The bigger question: who sold it at 65?

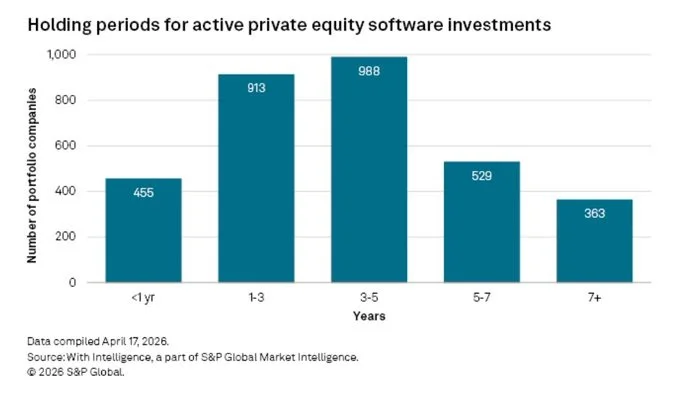

PE‑backed SaaS Stuck; Continuation Funds Become Lifeline

7% of PE-owned software companies in NA have been held 5+ years. 11% have been held 7+. The exit market for these names doesn’t exist: > Can’t be sold to strategics (their stock is down) > Can’t be sold to PE peers...

Creditor Conflict Shifts: From Companies to Private Co‑Ops

Evolution of creditor warfare: 10 years ago: creditors vs company 5 years ago: creditor vs creditor via doc changes (drop-downs, priming) Today: creditor vs creditor via private co-op Preview of the software maturity wall https://www.junkbondinvestor.com/p/credit-weekly-the-co-op-is-the-trade

FSK Trades at Half Book Amid Massive Losses

The $FSK setup: > Stock at $10.51 vs. $20.89 reported NAV > $517M in realized losses over five quarters > PIK at 34% of NII > 21 names on non-accrual > Bonds got downgraded to junk Stock trades at ~0.54x of book while...

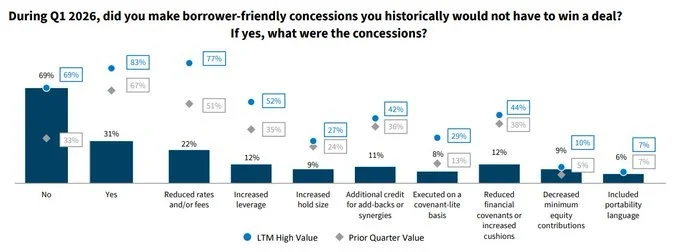

Lender Concessions Halve as Redemptions Surge

Direct lender concessions just collapsed. Q4 2025: 67% of lenders made borrower-friendly concessions to win deals. Q1 2026: 31%. The discipline showed up the moment the redemptions started. Funny timing. Source: William Blair

Bondholders' Holdout Triggers Spirit Airlines' Liquidation

Spirit Airlines is shutting down. The bondholders had two choices: 1. Take 10% of the equity in a Trump-backed reorg. 2. Hold out for more and risk liquidation. They held out. The cash ran out. Liquidation it is.

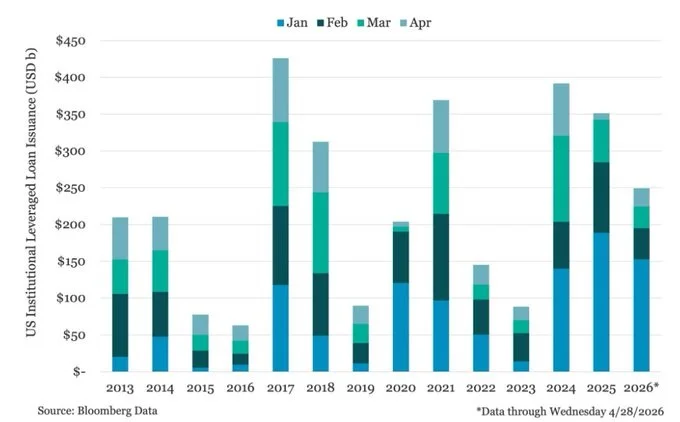

April Lev Loans Fall to Lowest Since Blackout

$25B of lev loan issuance in April (~15% below March). Lowest run rate since the post-Liberation Day blackout.

CVC Pumps €210M Into Tea Amid Falling Demand

CVC injecting EUR210M into its tea business to avoid debt restructuring Bought from Unilever for EUR4.5B in 2021 Tea consumption declining as young people switch to coffee Can't restructure consumer preferences