JunkBondInvestor

Credit analyst focused on high yield bonds, leveraged loans, and distressed/special situations with frequent deal/document analysis.

Consultants Demand Equity as AI Threatens Debt

The tough conversation goes something like this: Step 1: We hired consultants Step 2: They say AI will disrupt you Step 3: Please inject equity to protect our debt

Lenders Seize Medallia, Opt for Cash Control

Lenders taking the keys from Thoma Bravo on Medallia is actually the right call. Imagine the BSL version. Uptiers, primings, LMEs. Sponsor kicks the can for 18 months and plays for optionality with your principal. At least here, lenders can take the...

JPM’s Private Credit Push Exploits Peers’ Public Warnings

Dimon: "Some firms may be brilliant, but I guarantee you not all 1,000 of them are." $JPM this month: launching a multi-billion dollar private credit strategy. The playbook: warn publicly, build privately, take share when peers stumble.

Trump’s Spirit Deal Sets New Restructuring Playbook

Trump's offer for Spirit: $500M 1L loan, 90% of the equity via warrants. Bondholders fighting over the leftover 10%. This is the new restructuring playbook.

AI‑crafted Earnings Remarks Risk Tone‑tuning Scandal

Waiting for the first CEO to get caught reading AI-generated earnings remarks and accidentally reading "I can generate additional versions in a more conservative or optimistic tone."

Redeem NAV, Buy Discounted Public BDC: Simple Arbitrage

Redeeming a nontraded BDC at NAV and buying the corresponding public one at a discount. Funny WSJ is calling this an "arbitrage."

PE Treats Sports Teams Like Fund, LPs Await Returns

PE guys focusing on running sports teams while their LPs wait for distributions is the asset class in one sentence.

JPMorgan’s Private‑credit Playbook: Inflate Rates, Warn

The JPMorgan private credit playbook this month: 1. Raise back-leverage rates 50-150bps. 2. Mark down the collateral. 3. Tell the press the asset class is risky. 4. Launch your own fund. The warnings were always going to end in a product launch.

Credit Investors Snap up BDC Bonds as Retail Exits Equity

Third BDC bond deal in eight days. All oversubscribed. All priced tighter than talk. Credit investors are buying the liability stack while retail is trying to exit the equity below it

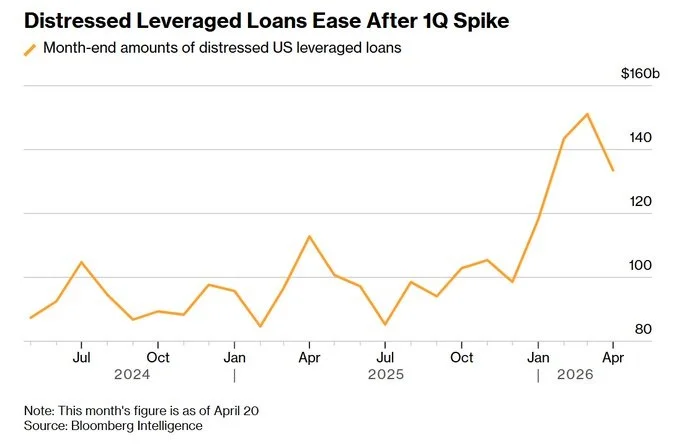

Tech Junk Debt Spikes as Broader Credit Stays Risk‑on

Software 45% of distressed lev loans, up from 42% $130B+ of junk-rated tech debt maturing in 2028 Meanwhile, the rest of credit is firmly risk-on

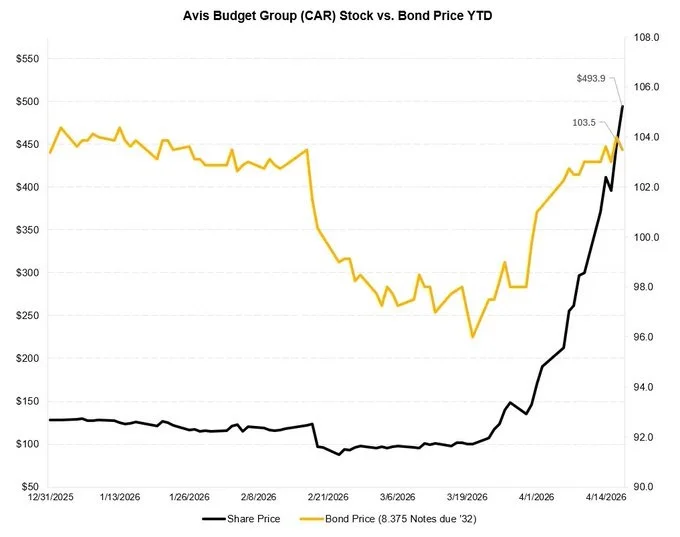

Avis Soars 300% on Float Squeeze and Geopolitics

Anyone following the Avis situation? Pentwater 22% + TRS synthetics + SRS 49% = >100% of float owned. 54% of float short. Stock doubles on that alone: ~$100 to $200. Then Iran hits: > Domestic travel substitution -> more rental days > Crude up...

Execute Non‑Pro Rata LME to Capture Discount, Reduce Holdout Risk

Claude, execute a non-pro rata LME capturing principal discount while minimizing holdout risk Make no mistakes

Private Credit Talk: Focus on Their Fundraising Motives

Every major player in the industry has something to say about private credit. Before you read any of it, ask one question: what are they raising, and how does this help them raise it? https://www.junkbondinvestor.com/p/private-credit-unfiltered-everyone

TCW Wipes Red Lobster Equity, Keeps Full Debt Exposure

TCW marked its Red Lobster equity down 98%. Its PIK'ing private credit loan maturing in 2029? Par Equity at zero and debt at 100 in the same company. C'mon, are you kidding me?

Levered Lending Cycles Always End the Same, Just Bigger

The FT pointing out what should be obvious: every levered lending cycle ends roughly the same way. New financing innovation, rapid growth, retail participation expands, crisis, etc Each cycle is bigger. Each wave of retail participation arrives later

AA DIP Tranche Hits QofE, Global Refi Begins

The year is June 2027. First Brands’ new money ultra-priority DIP Tranche AA just traded down to 50 cents. Great news though - the QofE just hit. Finally, the global refi can commence.

Yahoo Launches $1.6B

Yahoo kicking off a $1.6B refi. S+550 at 98.5. Mid-to-high 9s. Apollo paid $5B for this in 2021. Existing debt matures in 2027. Let’s see how this goes

PE Market Crashes: Deals, Exits Plummet,

PE deal values down 36% Exits down 33% Fundraising weakest since 2018 LPs “completely risk off” on software The $4T PE exit backlog is getting bigger…

Blue Owl’s Credit Woes Mask Hidden Asset Value

$OWL hit all-time lows today after record redemption requests. The credit business deserves every bit of this. But Blue Owl also has a GP Stakes business and a real assets business that have zero direct connection to software loans or BDC redemptions. Ran...

Oracle Data Center Debt Costs Surge to High‑Yield Levels

Wow, borrowing costs on Oracle data center projects have widened to as high as S+450 $ORCL is IG. The data centers being built for Oracle are pricing like high yield.

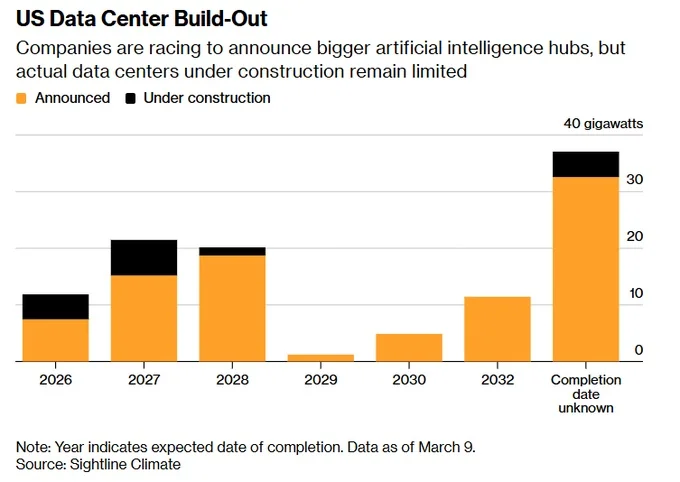

Only One‑Third of 2026 Data Center Capacity Under Construction

12GW of data center capacity supposed to come online in 2026. Only a 1/3rd is actually under construction. The capex is committed. The infrastructure can't be built fast enough.

Mativ's 95¢ Pricing Ranks Among Deepest US Lev Discounts

Mativ priced at 95 cents. Only 2 US lev loans have priced at deeper discounts this year.

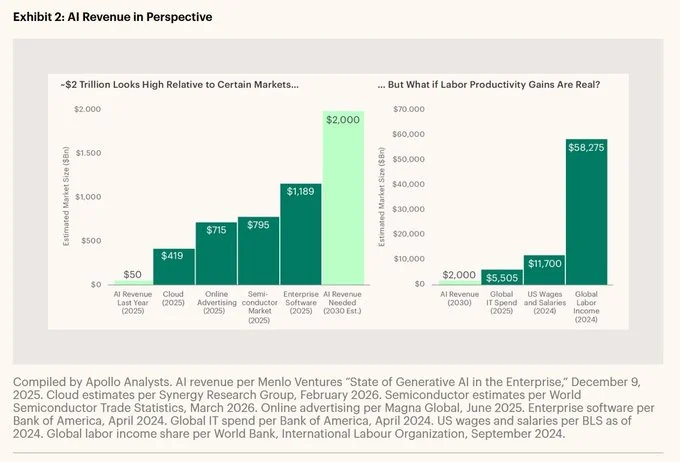

AI Needs $4‑5T Investment to Reach $2T Revenue

According to Apollo, $4-5T in AI infrastructure investment needed by 2030 To earn an acceptable return, AI revenue needs to hit $1.5-2T annually. Current AI end-user revenue: $35-65B. Revenues just need to 30-40x from here

Cliffwater’s $33B Fund Cracks Under Redemption Pressure

Cliffwater is a $33B fund invested in 50+ other funds that are all gating simultaneously. $4.6B in unfunded commitments. 14% redemption requests. S&P negative outlook. “It all works great when no one wants their money back.”

Jefferies Flags Multiple Hits

Jefferies: “There’s some noise in our numbers” The noise: MFS collapse, First Brands fraud, $36M telecom writedown, 24% decline in fixed income revenue.

Egan‑Jones Filled Private Credit Rating Gap, Now Under SEC Scrutiny

The private credit boom needed ratings. The big agencies were slow. Egan-Jones filled the gap. 20 analysts. Thousands of ratings. Insurers relied on them. Only now is the SEC is asking questions. 🤔

Ares Honors Few Redemptions, Claims Stakeholder Alignment

Ares: 11.6% redemption requests. Honored 5%. Called it “aligned with the best interests of all stakeholders.” The stakeholders who wanted their money back might define “best interests” differently.

EA's $15B Debt Oversubscribed, $25B Orders Signal Open Markets

$25B in orders on $EA’s $15B debt deal. Oversubscribed. Getting done. Capital markets are wide open… For the right issuers at the right price with the right Saudi SWF backstop.

LP Secondaries Plunge Below Par as GP Continuations Surge

7% of LP-led secondaries in 2H’25 sold at par. Over a quarter sold < 80 cents. Meanwhile GP-led CVs are booming. Different structure, same problem The traditional exit isn’t there at the price the GP underwrote.

S&P Threatens Downgrade Unless Funds Cap Redemptions

S&P to Cliffwater: if you keep honoring redemptions above 5%, we might downgrade you. So the choice is: gate your investors and keep your rating, or pay your investors and lose it. The product design is now working against itself.

Senior Deals Earn Fees, Then Face Distressed Capital

The 2024 SteerCo playbook: Go super-senior, get fees, get paid. The 2026 SteerCo playbook: Go super-senior, get fees, get stuck with new money that’s now also distressed.

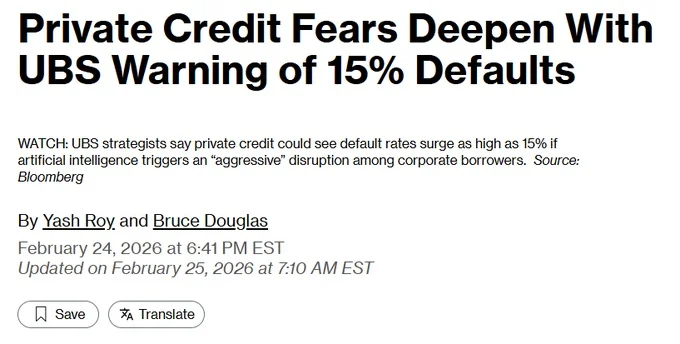

Forecasts Keep Rising, Yet Critics Call Them Irresponsible

Every month someone publishes a higher default forecast. > Fitch: 5.8% actual > Morgan Stanley: 8% > UBS: 15% worst case Every month someone in the industry calls it irresponsible.

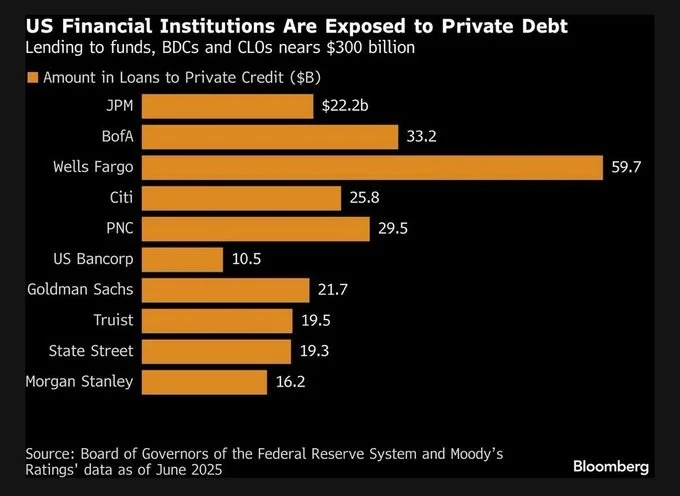

Banks Shifted $300B Risk to Private Credit Funds

$300B in bank loans to private credit funds, BDCs, and CLOs. "Private credit moved risk out of the banking system" was always the pitch. The banks just lent to the funds instead of the borrowers.

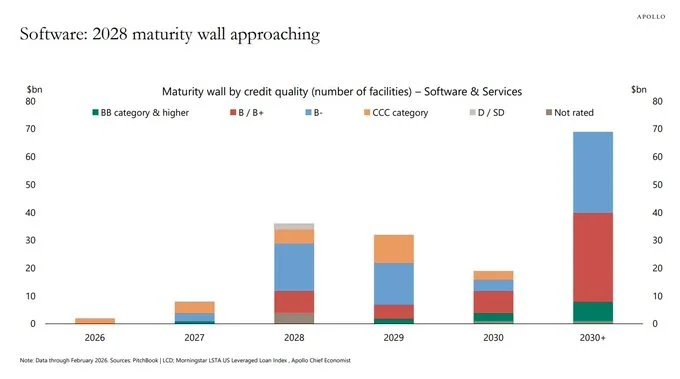

Coercive A&E Dominates $38B Software Maturity Market

The software maturity wall isn't a secret. Everyone has this chart. $38B in 2028. Mostly B and below. These aren't getting refinanced at par. They're getting extended. The only question is whether the A&E is consensual or coercive. And if the last...

OBDC's 25% NAV Discount Highlights Stale Marks

Blue Owl says the marks are real. Every sell-side analyst has a Buy. Yet $OBDC trades at a 25% discount to NAV. Finally had a chance to go through the portfolio. Found exactly what you'd expect: stale marks, understated software exposure,...

Cliffwater Blames Sentiment Amid $33B Fund Redemptions

Another one. Cliffwater facing 7%+ redemptions on their $33B fund. Their response: “Sentiment is driving the selloff more than fundamentals.” That’s what they all say. Right before the gates go up.

AI Giant Issues $25B Debt to Boost Stock

The AI poster child is issuing $25B in debt to buy back its own stock. Not to invest in AI. Not to acquire capabilities. To support the share price. That's the strategy. $CRM

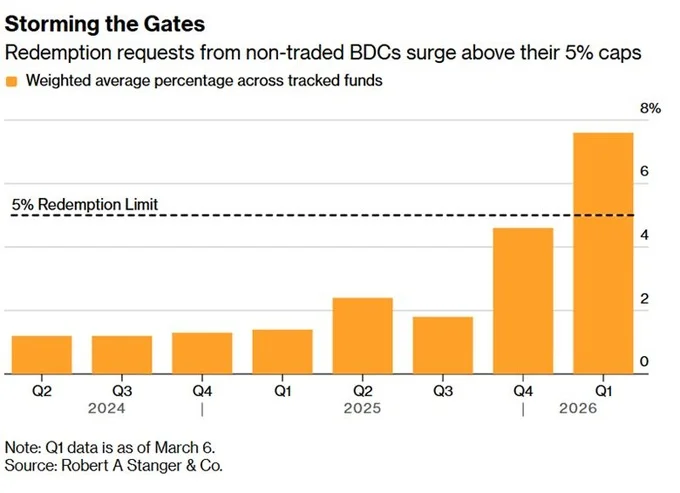

Non‑traded BDC Redemptions Surge Past 5% Limit, Eye Retirement Access

This is the chart the 401k conversation should start with. Non-traded BDC redemption requests blowing past the 5% redemption limit. Trajectory straight up. And the industry's next move is to open these products to retirement accounts.

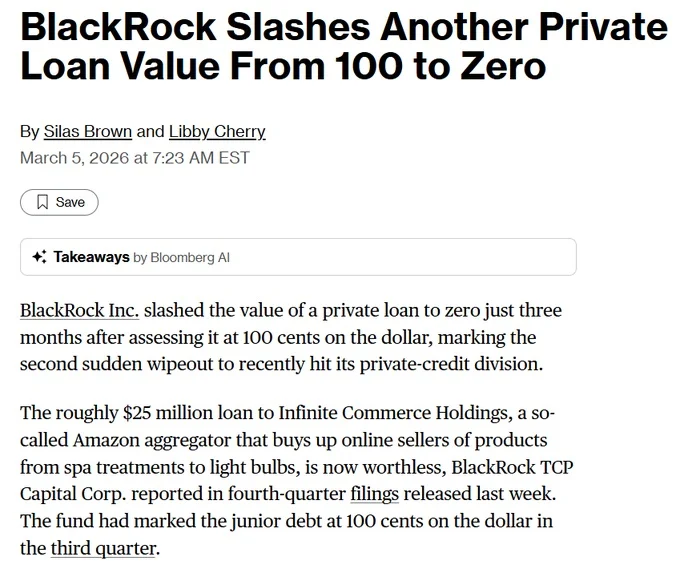

BlackRock Wipes Private Credit Loans to Zero in Three Months

Well well well... BlackRock marked a private credit loan at 100 cents on the dollar in Q3. By Q4, it was a big fat ZERO. Not 80. Not 50. ZERO. In 3 months. This is the second time $TCPC has done this recently....

UBS Predicts Private Credit Defaults Surpass 2008 Crisis Level

UBS's worst-case default rate for private credit is 15%. Up from 13% a month ago. For context, the 2008 leveraged loan default rate peaked at 10.8%. UBS is now modeling a scenario worse than the financial crisis for private credit. And they...

Most Weekly BDC Discounts Are Mispriced—Learn Why

Everyone has a BDC take this week. Most of them are wrong. If you don't understand how they trade, what drives the discount, or why NAV isn't what you think it is, start here. https://www.junkbondinvestor.com/p/the-bdc-primer-part-1

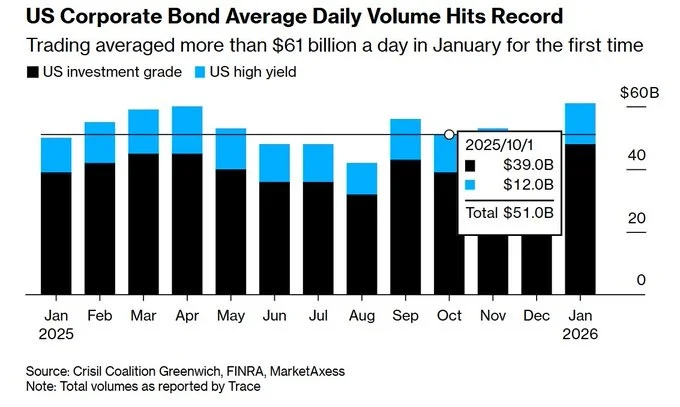

Demand Surge Compresses Bond Spreads Despite Record Issuance

Record bond issuance. Record trading volumes. Tighter spreads. More supply should widen spreads. Instead buyers are so hungry that more issuance actually improves liquidity and compresses risk premiums. This works until it doesn’t.

CLOs Bet on Yield While AI Threatens Software Holdings

This is the CLO market right now: Sellers: AI will destroy these businesses Buyers: Thanks for the yield Software is the largest sector in CLO portfolios globally. 10-15% concentration. Nearly half mature in the next 3 years. Someone here is wrong.

AMC Refires $2.5B to Trim Maturity Wall

AMC moving to clean up its maturity wall. $2.5B package taking out 2027 notes (12.75%) and 2029 TL If it prices well, decently lower interest burden. $AMC

Private Credit Bets on Software Amid AI Uncertainty

Five private credit firms just provided $1.4B for a software buyout of OneStream valued at $6.4B. Same week everyone’s asking whether AI will make these companies obsolete. The market is telling you software is at risk. The lenders are telling you...

Alphabet and Meta CDS Explode From Zero to Top Traders

A year ago, CDS on Alphabet and Meta didn't exist. Now they're among the most actively traded single-name contracts in the US market Nobody creates a default insurance market for fun... $GOOG $META

AI Disruption Drives Widening Credit Spreads Ahead of Earnings

AI disruption is hitting IG credit spreads, not just stock prices. Concentrix: BBB-rated, 455,000 call center employees. Paid 130bps concession to refinance. Stock down 24% last week. Spreads doubled in February. Credit markets pricing obsolescence before it shows up in earnings.

BDC Quarterly Letters: Refusing Write‑Downs, Defying Pressure

Every BDC quarterly letter should just say “we are choosing not to mark this down and you can’t make us.”

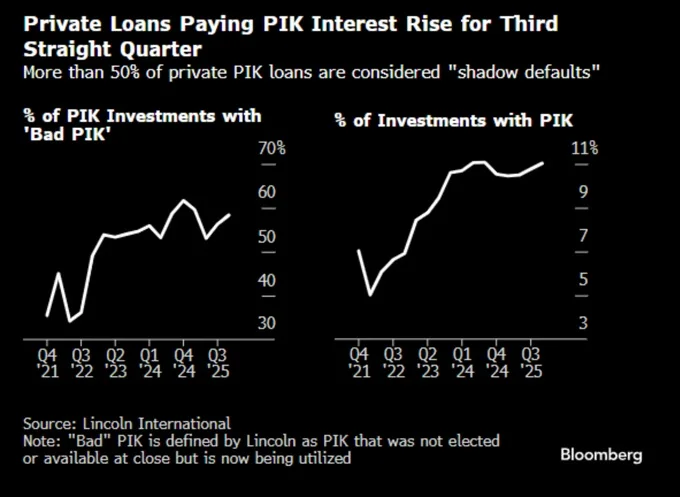

Most Private Credit PIK Is Bad Yet Labeled Performing

58% of PIK in private credit is "bad PIK" per Lincoln. Borrower stops paying cash. Lender accepts more debt instead. Everyone marks it at par. This is called "performing."

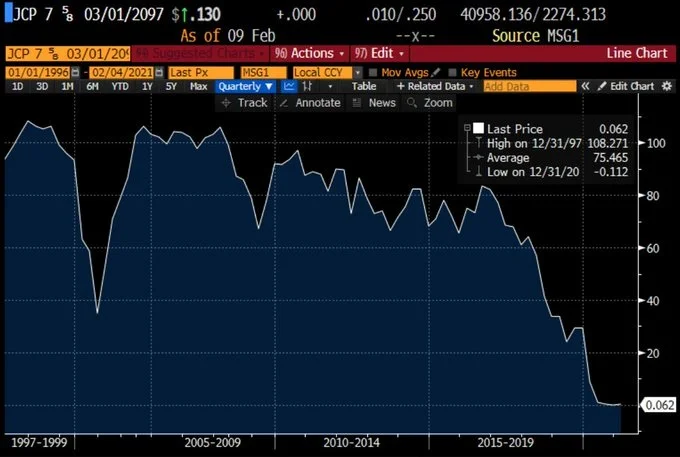

Google’s 100‑Year AI Bond: Ambitious or Foolhardy?

Google issuing a 100-year bond to fund AI capex. Remember JC Penney’s 100-year bond? Issued in 1997. Bankrupt in 2020. At least they got their basis back in coupons.