Equities Surge, Bonds Lag as Risk Spikes

$QQQ is up 20.8% from the Mar 30 low. $TLT is near the bottom of its 3-month range. Risk is screaming. Bonds are not applauding.

SPY Surge, VIX Plunge: Fear Turns to Complacency

$SPY just ripped from 631.97 to 720.65 while the VIX fell from 31.05 to 17.50. That is not healing. That is a market rapidly repricing fear into complacency.

Success Comes When Comfort Is Stripped Away

When God wants to make you successful, he doesn't start by giving you comfort. He starts by taking it away. In silence, you hear Him clearer.

Fed Split, Japan's Massive Yen Defense, Markets on Borrowed Time

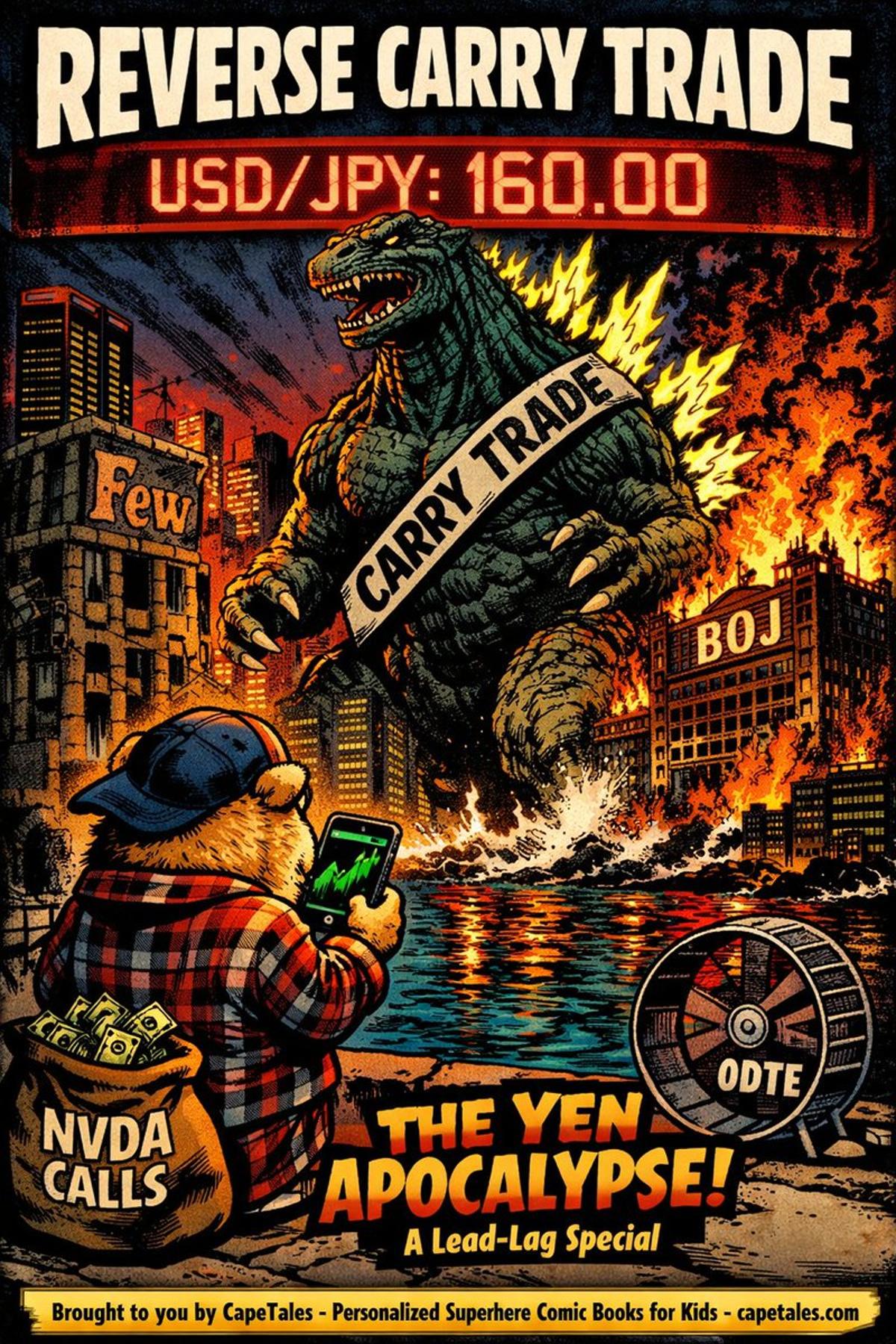

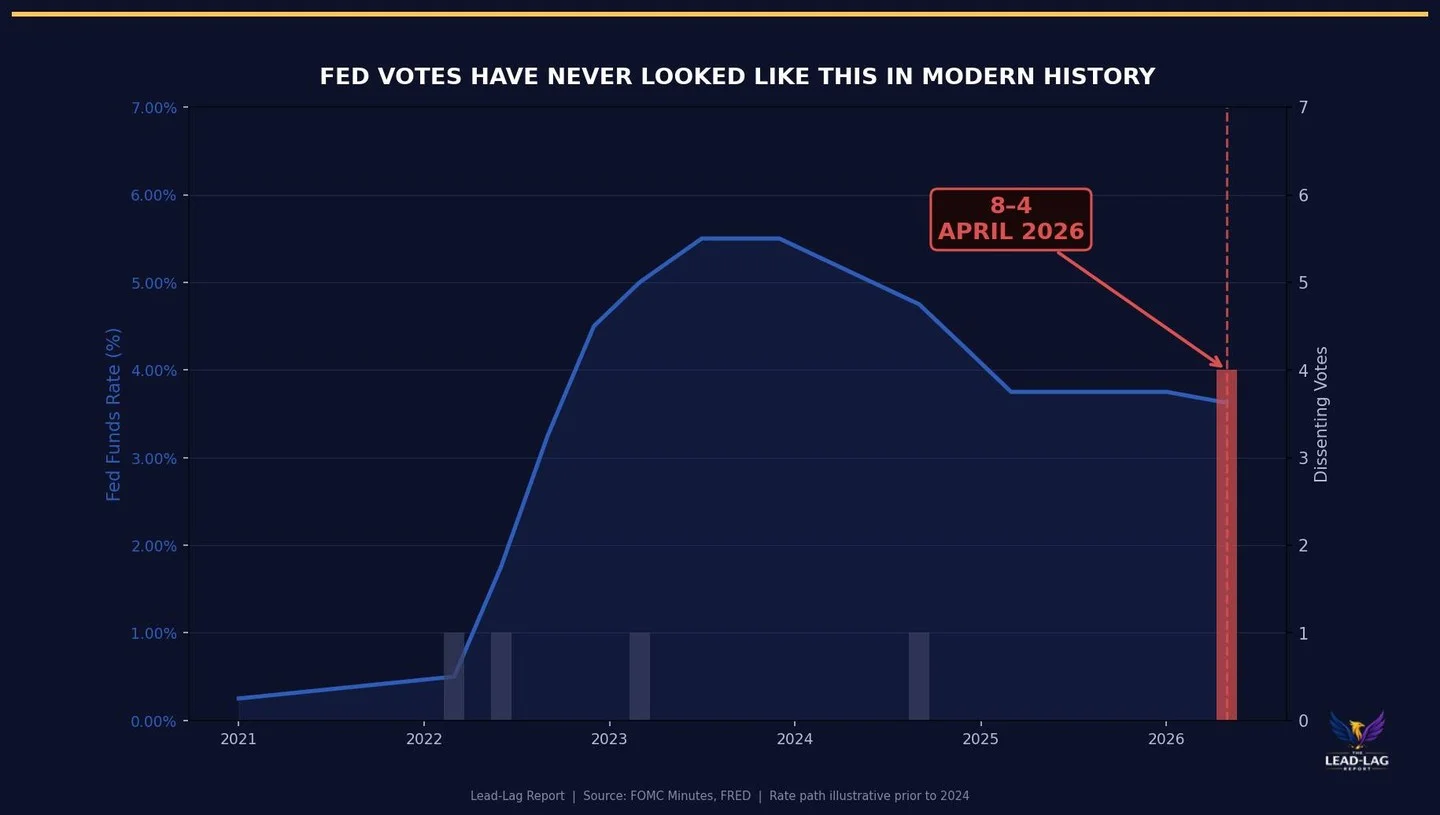

The Fed just split 8-4. Most divided vote since October 1992. Japan torched ¥5.4 trillion — 7% of FX reserves — in a single day defending the yen at 160. S&P at a record. Nasdaq's best month since 2020. This is what borrowed...

Pre‑launch Period: Untapped High‑leverage ETF Marketing Window

Most ETF launches die in the gap between ticker drop and AUM. The pre-launch period — when the issuer is allowed to talk about the thesis but not the ticker — is the highest-leverage marketing window in ETF GTM, and...

AI‑Powered 80‑Agent Stack Beats Wholesaler Costs

Asset manager sales teams are still working off lists assembled by hand. AI changes the unit economics: an 80-agent stack that produces, qualifies, and personalizes outreach 24/7 — at a cost lower than one wholesaler. https://t.co/0Kbbd3qyUD

Reverse Carry Trade Explained: Oil, Yen, Japan Insights

I have been quiet long enough. This is perhaps the most important thread on X ever published. And the most powerful and impactful comic book you will ever read. If you want to understand the reverse carry trade, bookmark this. Oil, Yen, Japan,...

Shift From SEO to AI‑focused Schema for Advisor Discovery

Most advisors optimize for Google’s ten blue links while their HNW prospects are now asking ChatGPT, Perplexity, and Claude for advisor recommendations. The schema markup, citations, and bio harmonization that move the needle on AI visibility — and why it’s...

First Reverse Carry Trade Comic Drops in 24 Hours

I’m going to release my first ever comic book on the reverse carry trade in 24 hours. Fucked. Few. 🐦🔥 Goodnight.

Fed Split Signals Market Uncertainty, Not Certainty

The Fed held 3.50–3.75% on 2026-04-29… and it was an 8–4 vote. Four dissents. When policy is split like that, “certainty” in markets is a fantasy. VIX at 18.02 is the tell. Silence isn’t safety. It’s complacency. markets

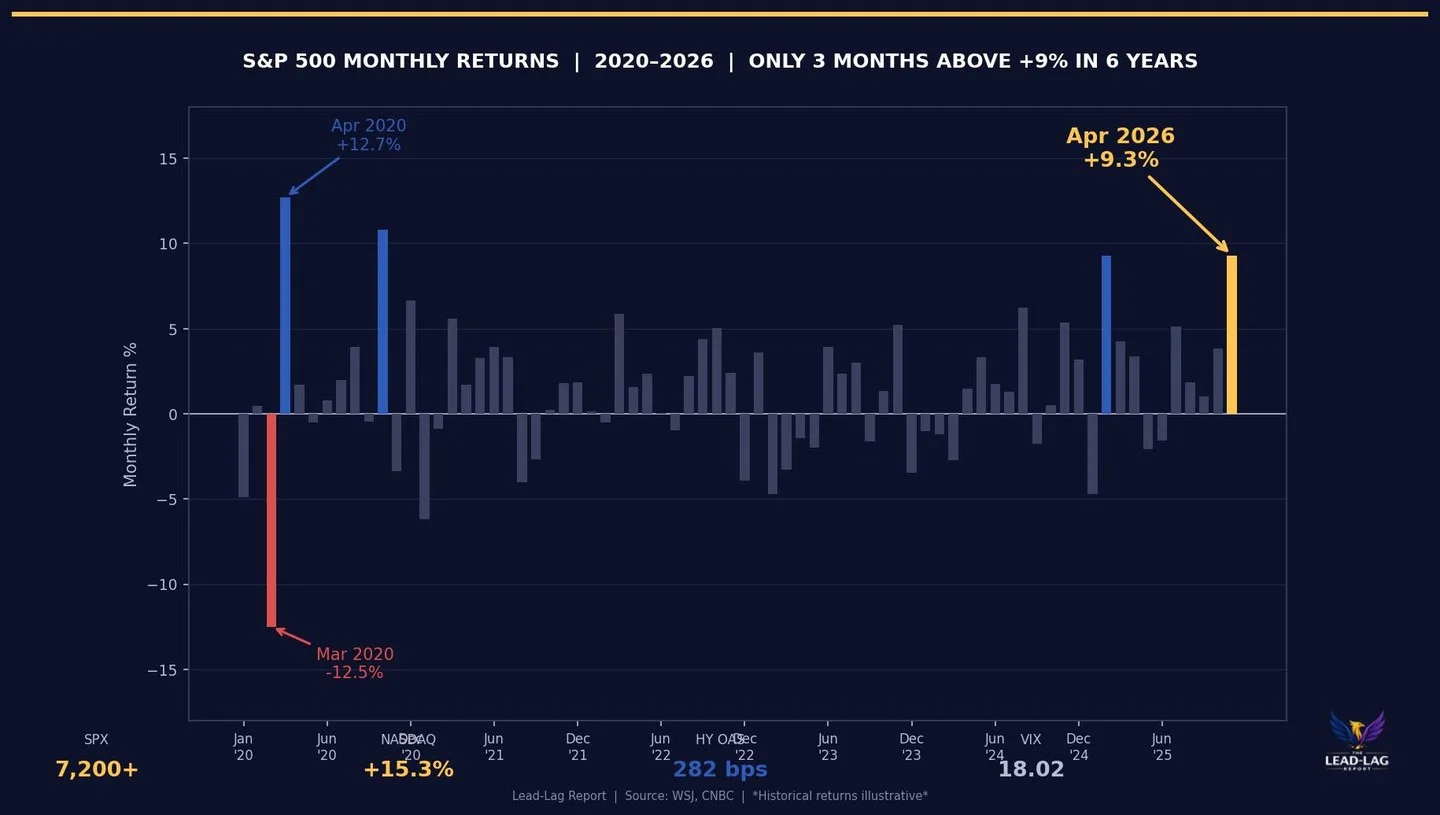

Record Highs and Low Volatility Signal Dangerous Market Crowding

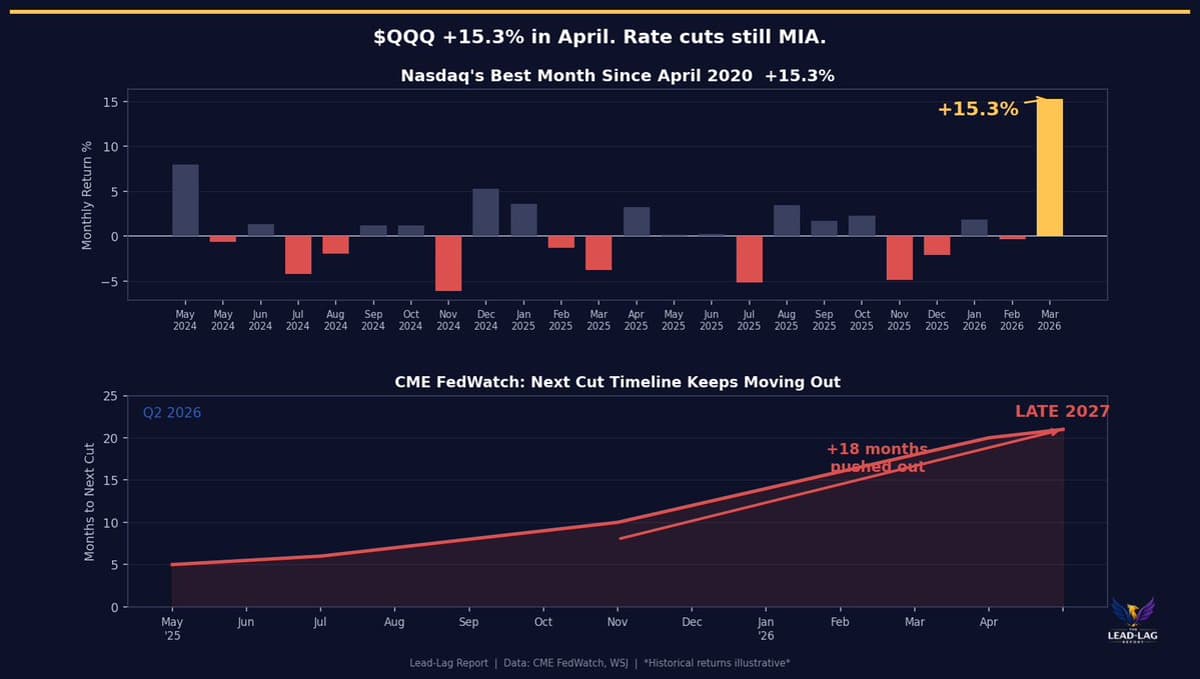

Record closes and “calm” volatility are a dangerous combo. SPX: first close above 7,200. Nasdaq: +15.3% in April. HY spreads: ~282 bps. VIX: 18.02. That’s not fear. That’s crowding. The unwind never rings a bell. markets

Nasdaq up 15% in April, HY Spreads Stay High

April +15.3% on Nasdaq… and HY OAS is ~282 bps. That’s not “risk-off.” $QQQ https://t.co/NMz38kcNP3

No Sleep, Still Gym: Stop Making Excuses

Slept for only 4 hours. Still at the gym this morning. The fuck is your excuse?

Tech Leads S&P to Record Amid Broad Sector Weakness

Five of eleven sectors are red on the year. The S&P just printed its tenth record of 2026 anyway. Intel +24% in a session. Tech now leads on every lookback for the first time this cycle. The whole rally is one sector deep. https://t.co/GoP96luvwI

Even Mother Teresa Doubted, yet Never Gave Up

Even Mother Teresa had her doubts about God. In the end, she did not relent.

27 Weekly Distributions: YieldBOOST ETFs Offer Double-Digit Returns

27 weekly distributions just dropped. Some of these YieldBOOST ETFs are paying double-digit weekly rates. Worth a look. https://t.co/GRt5SC6GPI @GraniteShares @WillRhind

New Income Strategies Replace Broken 4% Rule

Bonds are failing retirees. The 4% rule is broken. Covered call ETFs are leaving money on the table. Free CE credit panel TODAY at 1 PM ET with @TuttleCapital. What actually works for income in 2026. https://t.co/RQPLScxiYP

Fed Prioritizes Blame Avoidance Over True Price Stability

Fed watchers treat every print like it’s gospel. Newsflash: the Fed is a political institution wearing an economist costume. If you think they’re optimizing for “price stability” you haven’t been paying attention. They optimize for avoiding blame. That’s why policy lags reality… and why...

Growth Slowdown, Not Inflation, Will Be the Next Shock

Contrarian take: the next shock won’t be inflation. It’ll be growth rolling over while everyone’s still fighting ghosts.

Fed Claims Data Dependence, yet Cherry‑picks Numbers

If the Fed is “data dependent”… why does it feel like the data is whatever they need it to be?

All Signals Turn Risk-On, Rally Likely Ahead

All four signals just flipped Risk-On. Utilities lagging. Lumber outpacing gold. S&P 500 nearly 7% above its 200-day. The last time the model was this aggressive, the rally extended. Are you positioned for it? https://t.co/AUo8JQGNdw

Wealthy Families Ditch 60/40 for Smarter Strategies

Most $5M+ portfolios look exactly like a $200K portfolio. Same 60/40. Same S&P 500 index. Same bond allocation nobody wants anymore. The wealthiest families don't actually invest like this. Here's how they actually do it. 🧵

Trump Deregulation Yields $212B Savings, Markets Unaware

The Trump administration finalized 646 deregulatory actions in 2025 — against just 5 new regulations. That's a 129-to-1 ratio. Net cost savings: $211.8 billion. Roughly $600 per American. Most investors haven't priced any of it in yet. Thread on what's already changed 👇

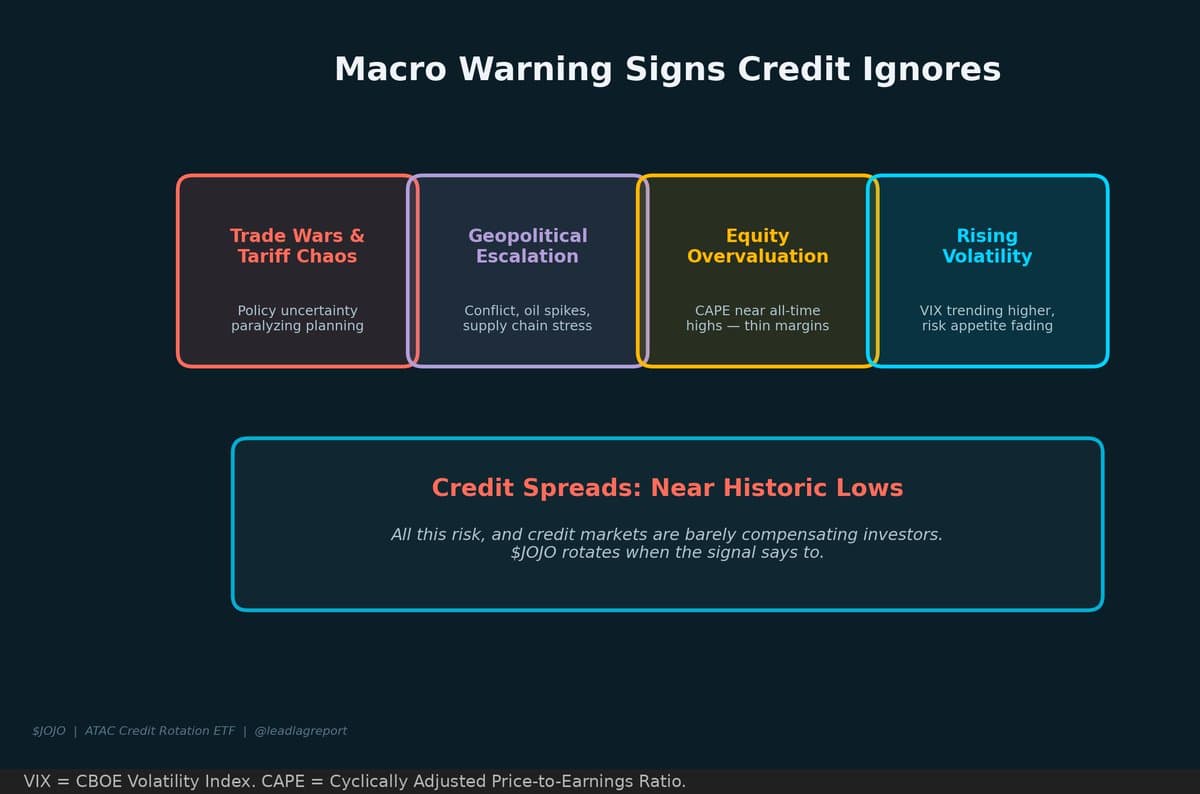

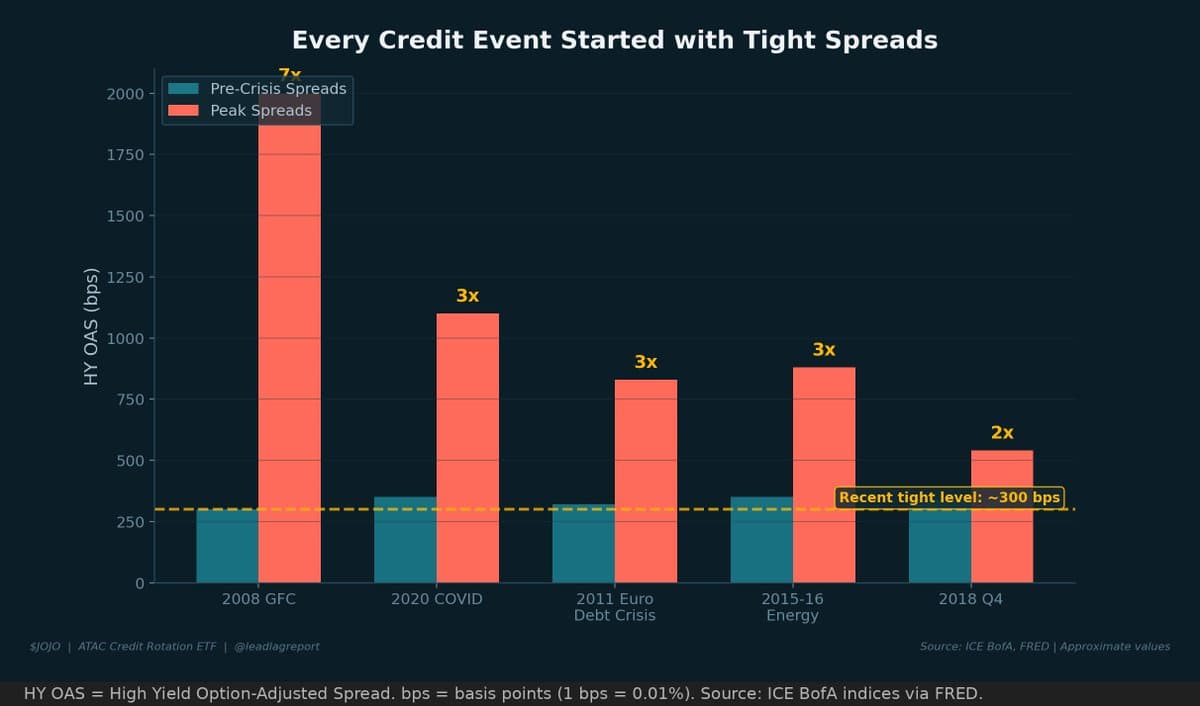

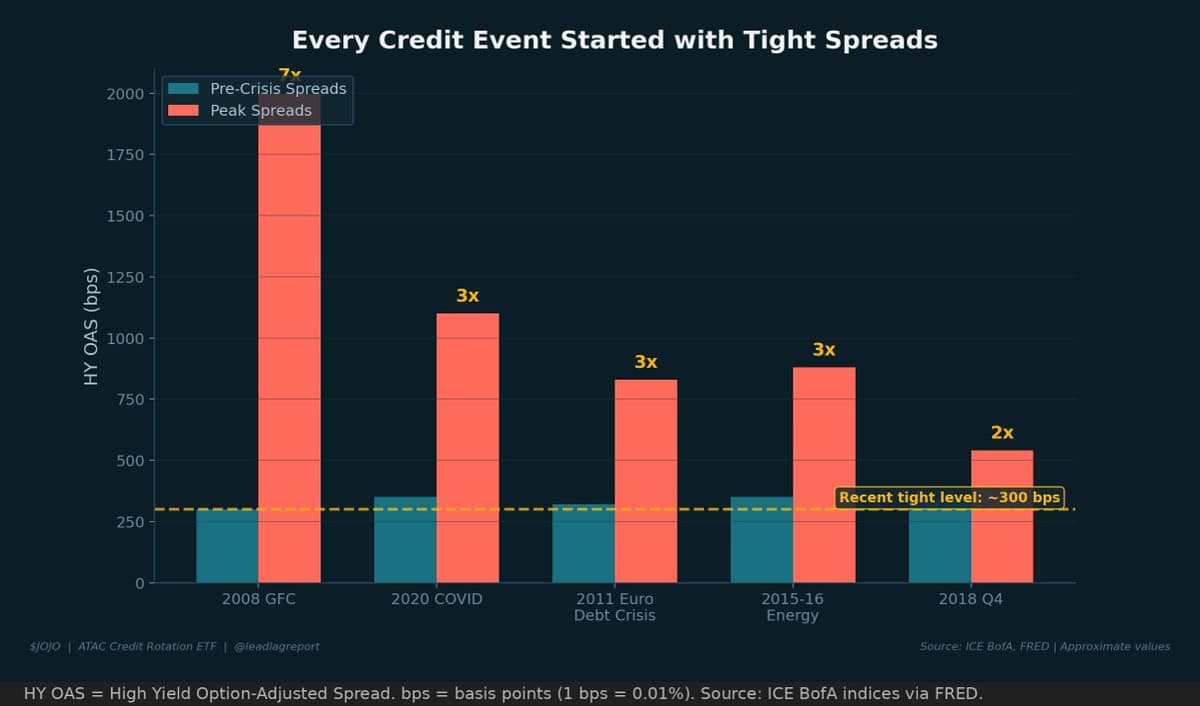

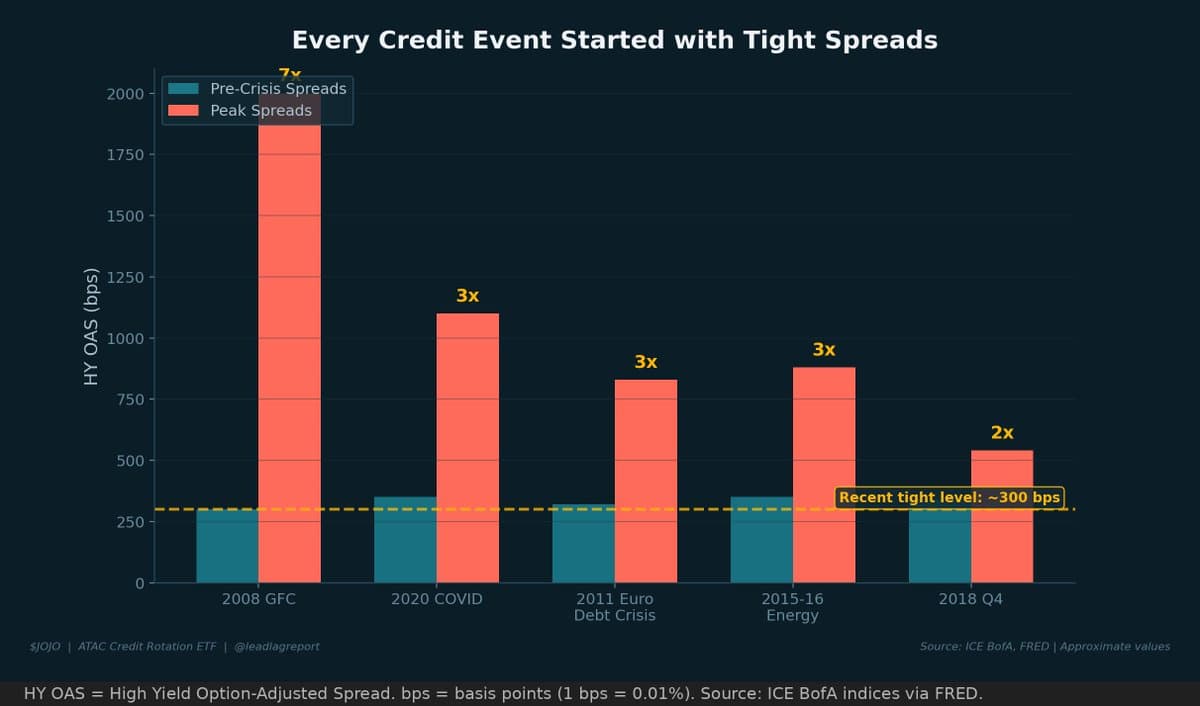

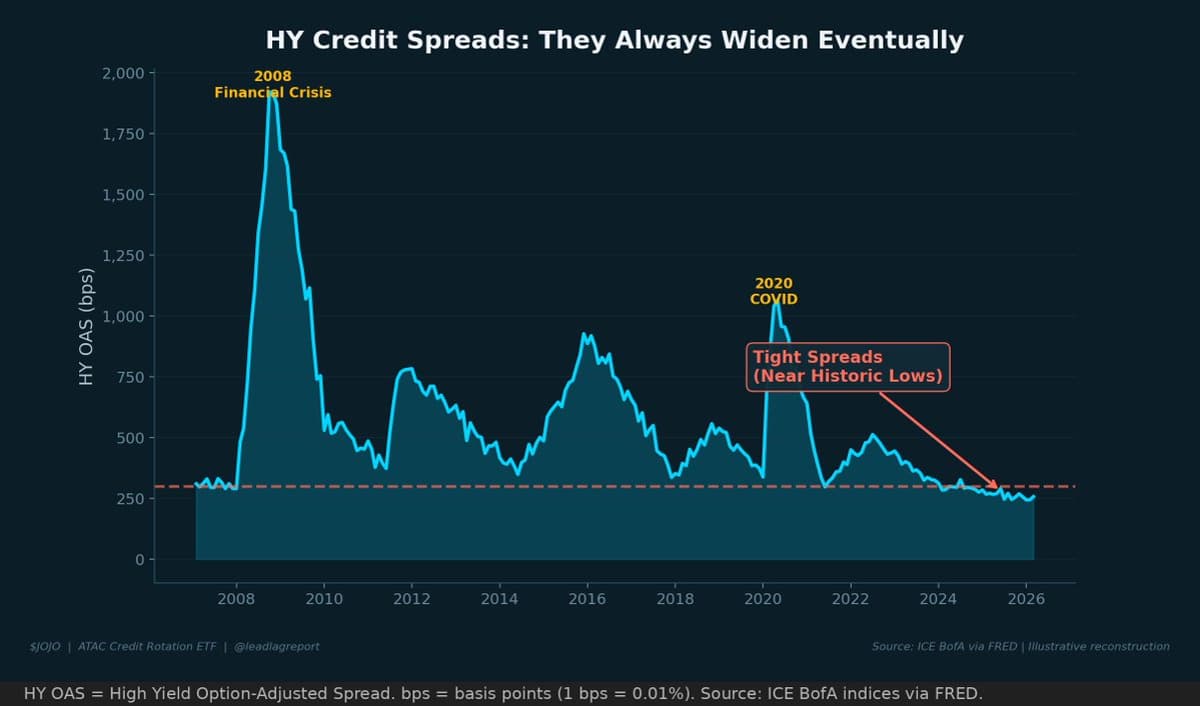

Credit Spreads Stay Tight Amid Rising Market Turbulence

Every major macro indicator flashes caution. Volatility rising. Equities under pressure. Geopolitical risk elevated. Yet credit spreads are asleep. $JOJO doesn't sleep. https://t.co/K90mNCoPv5

Regime Signals Reveal Winning Portfolio Framework Ahead

Gold near all-time highs. Oil elevated on Hormuz risk. IWM holding while long bonds struggle. These are regime signals — and they tell you exactly which portfolio construction framework survives what comes next. Wednesday I'm sitting down with Greg Babij of Sundial...

Trend‑following Beats 60/40; UHNW Go Beyond Passive Mix

The 60/40 portfolio fell 17.5% in 2022. Trend-following returned +20.1% the same year. Passive equity + bonds = the minority in a UHNW portfolio. Wed April 29, 12pm ET — Greg Babij (CIO, $500M+ MFO) breaks down how it's actually built. $5M+ only:...

Credit Spreads Signal Market Direction; Equity Lags Behind.

S&P 500 just hit 7,000 for the first time ever. HY credit spreads: 285 bps. Exactly where they sat in June 2007. One of these markets is wrong. Credit leads. Equity follows. Always has. https://t.co/r8IUinGk9s

Tight Spreads Signal Impending Volatility,

Every time spreads have been this tight, they widened violently. 2007. 2019. No one rang a bell then either. $JOJO is the bell. https://t.co/ae6yeTLVdx

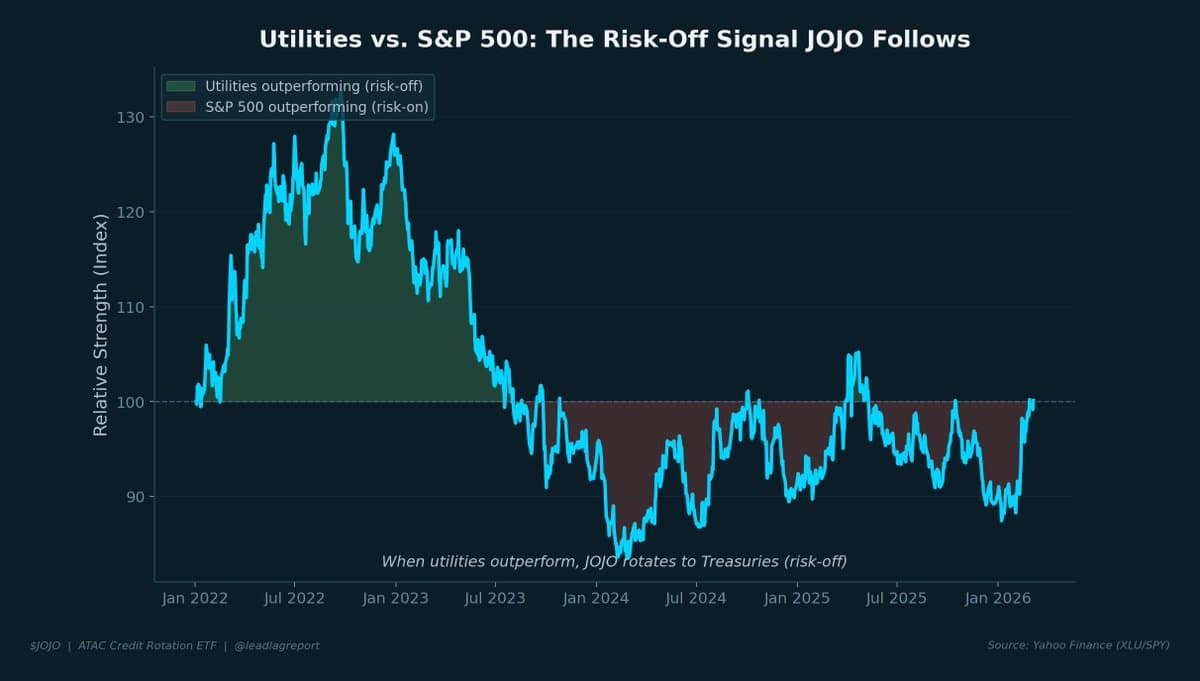

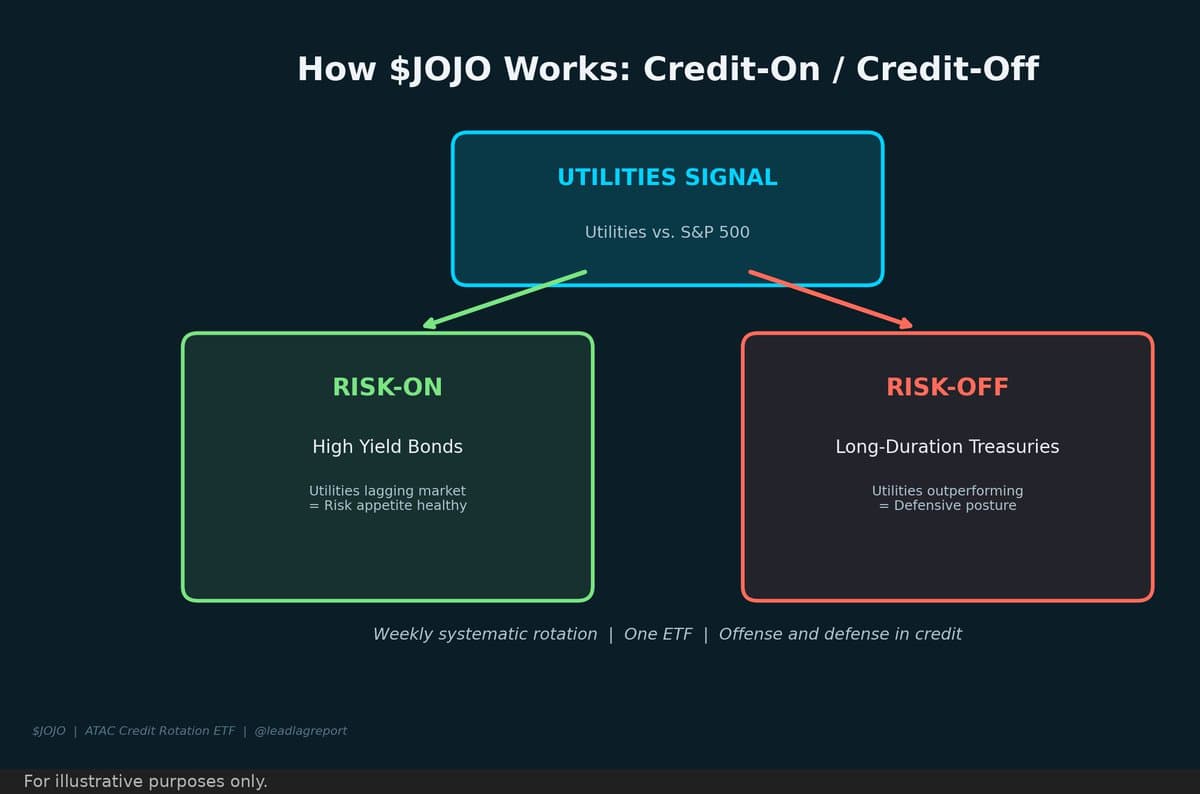

Utility‑Market Correlation Signals Risk Appetite, Guides $JOJO

Inter-market signals matter. The relationship between utilities and the broad market tells you something about risk appetite. $JOJO listens to that signal. @leadlagreport https://t.co/zaRxS4ePjI

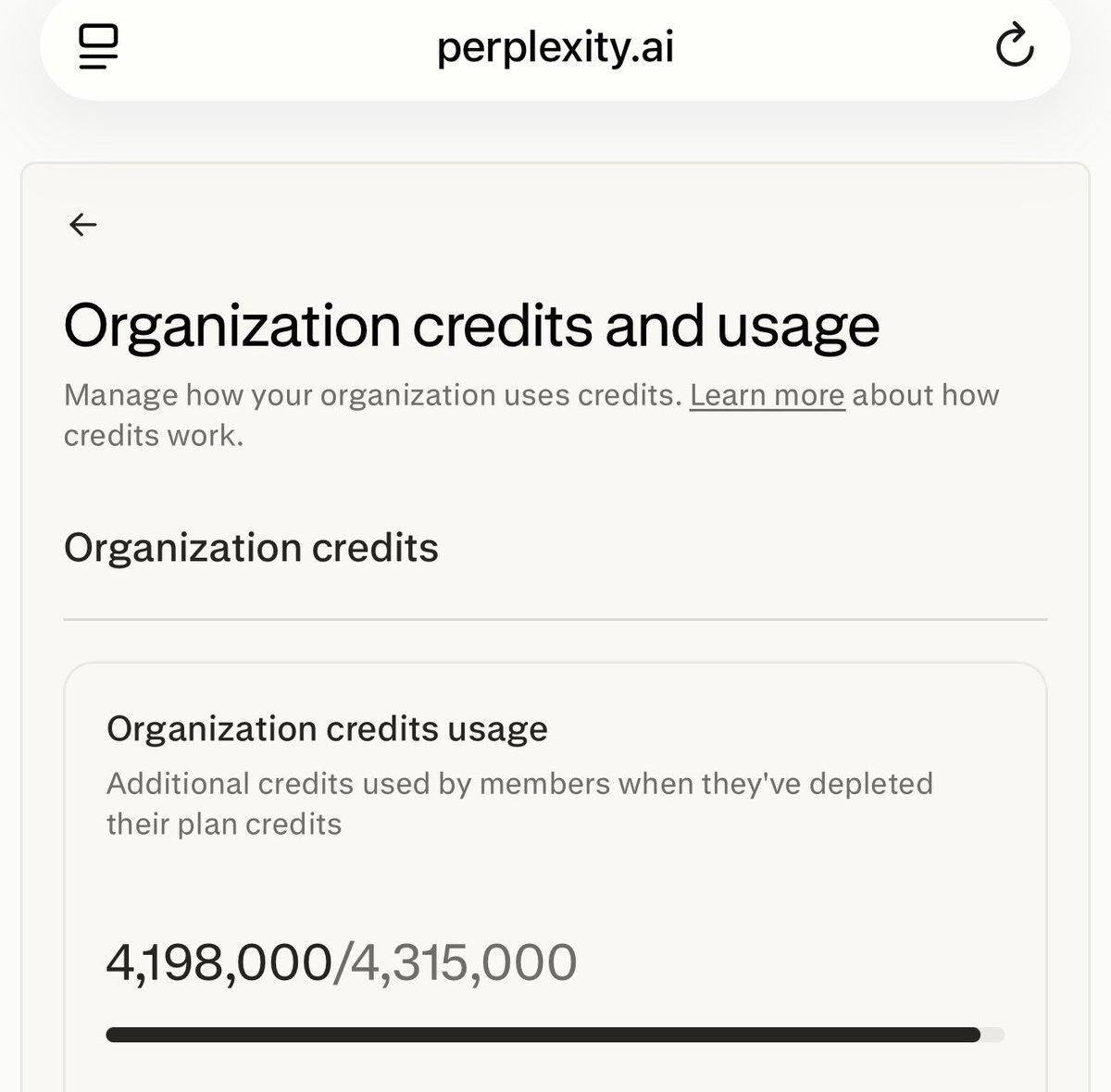

Spent $40k Building 70 AI Agents to Disrupt Finance

I have used over 4 million credits on Perplexity. Each credit is one penny. In 8 weeks. Ive built 70 AI agents. I’m about to disrupt the entire financial services industry for fund issuers and financial advisors. I’m about to remind you all...

Oil Slump Signals Waning Demand, Not Bullish Optimism

The narrative is that oil crashing is bullish — inflation cools, the consumer wins, rate cuts come sooner. Maybe. Or maybe oil is crashing because global demand is quietly rolling over and nobody wants to say it out loud. Energy...

Market Divided: Utilities Up, Treasuries Split, S&P Near

Utilities outperforming. Treasuries diverging. S&P sitting just below its 200-day moving average. The intermarket signals split 2-2 for first time since February. What does a market divided mean for your portfolio? https://t.co/bTNJ1cQFiS

Tiny Yield Premium, Huge Risk: Choose Smarter Credit

A sliver of extra yield over Treasuries for significant downside risk. That's not compensation. That's complacency. $JOJO offers a smarter approach to credit. https://t.co/cmg68D8cCS

Euphoric Markets Signal Imminent Bear Turnaround

Woke up, checked the markets. Everything green. Bulls are high-fiving each other. And I'm sitting here thinking — this is exactly when it gets dangerous. The tape feels euphoric right now. That is not a bullish signal, that's a warning....

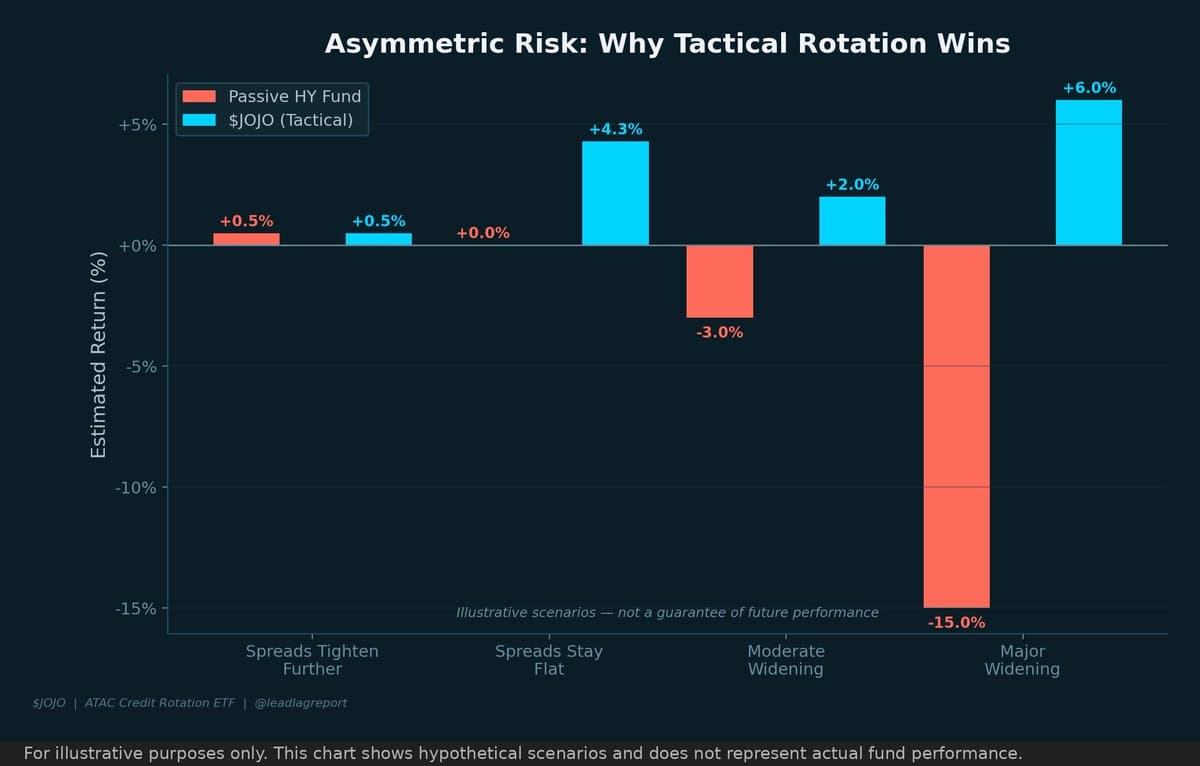

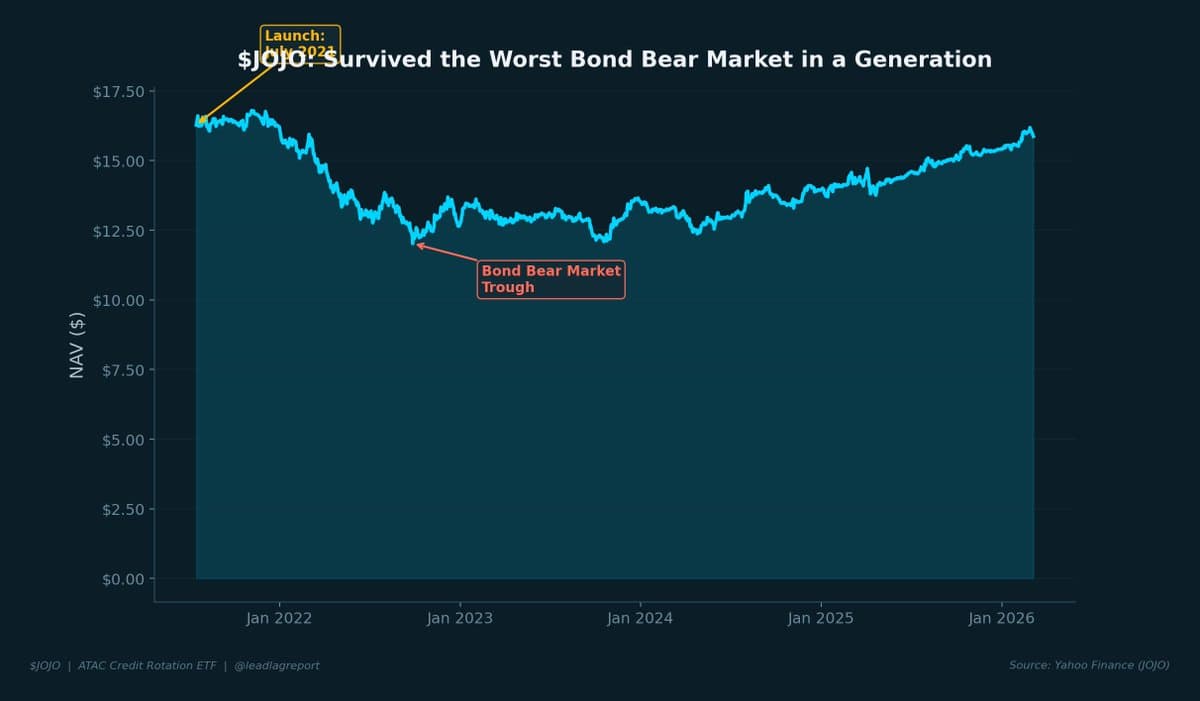

Worst Bond Cycle Makes Credit Rotation Essential

Every portfolio manager has a fund they believe in more than the market does. For me, that's $JOJO. The worst bond cycle in a generation is exactly why credit rotation matters. https://t.co/5FJoUQuUwE

JOJO Leverages Utilities Signals for Credit Rotation

Advisors looking for differentiation in fixed income: $JOJO uses utilities sector signals to rotate between risk-on and risk-off credit. Systematic, transparent, and timely. https://t.co/vNSFE0Fce0

Alliance

A 33-year-old global high-yield fund. 8% NAV discount — near the widest since 2022. 7.5% yield collected while you wait for the discount to compress. Is AllianceBernstein's AWF the unloved global income play right now? https://t.co/5wNRfc4Lcg

Dell Evolves Into AI Powerhouse, Not Just PCs

Dell just posted $113.5B in revenue. Up 19% YoY. $64B in cumulative AI orders. $43B in unfilled AI backlog. $30B in new buybacks. 20% dividend hike. This isn't a PC company anymore. $DLLL gives you 2x daily leveraged participation: https://t.co/ZjkBdri46R @GraniteShares

China's Consumer Rebound Hinges on Three E‑commerce Giants

China's consumer rebound isn't a headline. It's a tape. Alibaba, JD, Pinduoduo: the three names that make or break the story. @KraneShares lays it out. https://t.co/87UdsGYIfb

Gold's Rally Unwinds: Gravestone Doji Signals Hedge Collapse

Gold just printed a gravestone doji. While everyone cheered the ceasefire extension, the hedge trade quietly cracked. +36% in a year. -2.8% in a single session. One chart tells you what's really unwinding. https://t.co/2SqrR1yGxA

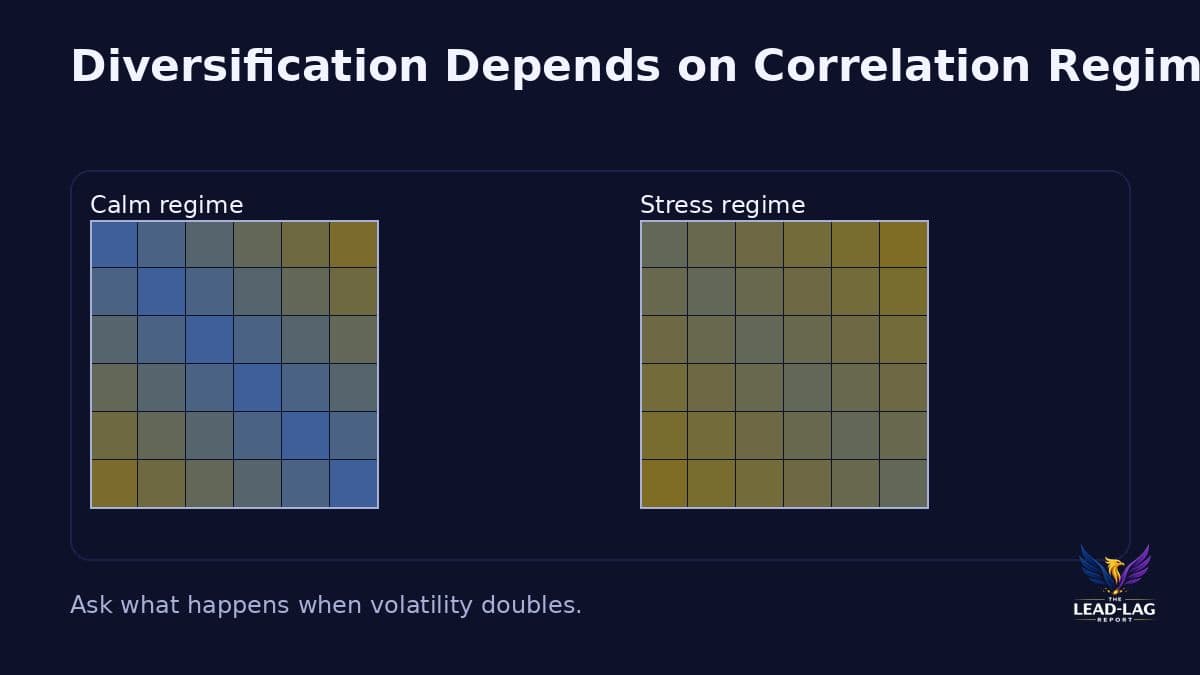

Watch All Markets Simultaneously for Edge

Risk-on: equities up, credit tight, EM leads, dollar weak. Risk-off: Treasuries rally, gold bid, yen strengthens, defensives lead. Most investors watch one market. The edge is watching all of them simultaneously. Divergence is the warning. $TLT $GLD $EEM https://t.co/wrXRW1Rzy6

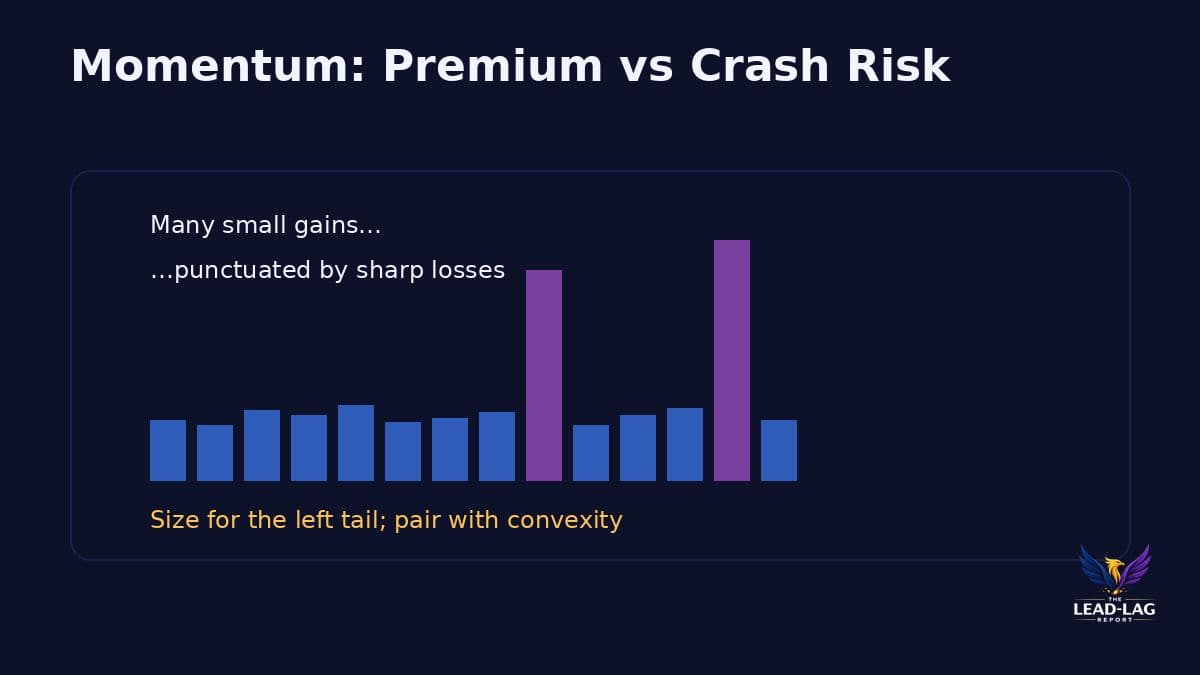

Momentum Shines, but Collapses During Market Reversals

Momentum investing works — until it catastrophically doesn't. 2009: factor crashed ~80% in weeks as beaten-down assets snapped back. 2020: COVID reshuffled winners overnight. The strategy that excels in trends fails hardest in reversals. Know your failure mode. $MTUM https://t.co/i22r0zoGHl

Tight Spreads Signal Risk, Not Safety

2007: Spreads were tight. Everyone was comfortable. Then Bear Stearns. Then Lehman. The lesson? Tight spreads are a setup, not a safety net. $JOJO knows the playbook. https://t.co/snHkbOgCAJ

Fed’s Rate Tightening Always Ends With Credit Cracks

The Fed's core dilemma: inflation requires higher rates. Credit breaks at higher rates. Every tightening cycle ends when something cracks — not when inflation hits target. 1982: S&L stress. 2007: housing. 2023: banks. Always the same story. $TLT https://t.co/Ogvr0NZVik

Gold Surges when Monetary Regimes Shift, Not Just Inflation

Gold doesn't shine every year. It shines during monetary regime changes. 1971: Bretton Woods collapses → gold 10x'd by 1980. Post-2008 QE era → gold 6x'd by 2011. The driver wasn't just inflation. It was confidence in the system itself. $GLD $GDX https://t.co/LTB2CfST8r

FMKT Slips 1% yet Stays Sole Deregulation-Focused ETF

The Free Markets ETF ( $FMKT ) ended trading at $21.97 today, down 1.01%. Even with today's slight dip, FMKT remains the market's only ETF focused on capturing value from deregulatory environments. https://t.co/1OVDiGBXUu

Markets Assume Peace, yet Signals Warn of Uncertainty

Three signals flashed green last week. One flashed yellow. S&P ripped +4.5%. Gold above $4,800. Oil collapsed below $85. The market just priced in peace. What if it's wrong? https://t.co/PPkEJEJRRN

Historic Low Credit Spreads Prompt Treasury Rotation

Everyone thinks credit is fine. That's exactly when it isn't. Spreads at historic lows mean you're getting paid almost nothing for risk. $JOJO rotates to Treasuries when the risk isn't worth the reward. https://t.co/su2AGVy5J5

Private Credit BDCs Cheap, High Yields Signal Buying Opportunity

Everyone says private credit is blowing up. BDCs are trading at 0.83x book. Yields are north of 6%. Default stats don't even measure the same thing. The "fire" is a buying opportunity. https://t.co/tKztIaLmRQ

JOJO Fund Survives Tough Market, Signal Still Works

I've spent years building $JOJO through a market that punished every bond strategy on the planet. The fund is still here. The signal still works. I'm asking you to look at it. @leadlagreport https://t.co/Yf5AlkpIwg