ACH Volume Is Soaring. Here's How that Threatens Banks.

Companies Mentioned

Why It Matters

The accelerating ACH adoption erodes banks’ deposit bases and interchange income, while the higher same‑day limit could reshape corporate payment flows and intensify competition with real‑time rails.

Key Takeaways

- •ACH payments hit 35.2 billion, +5% YoY

- •Same‑day ACH limit proposed $10 million

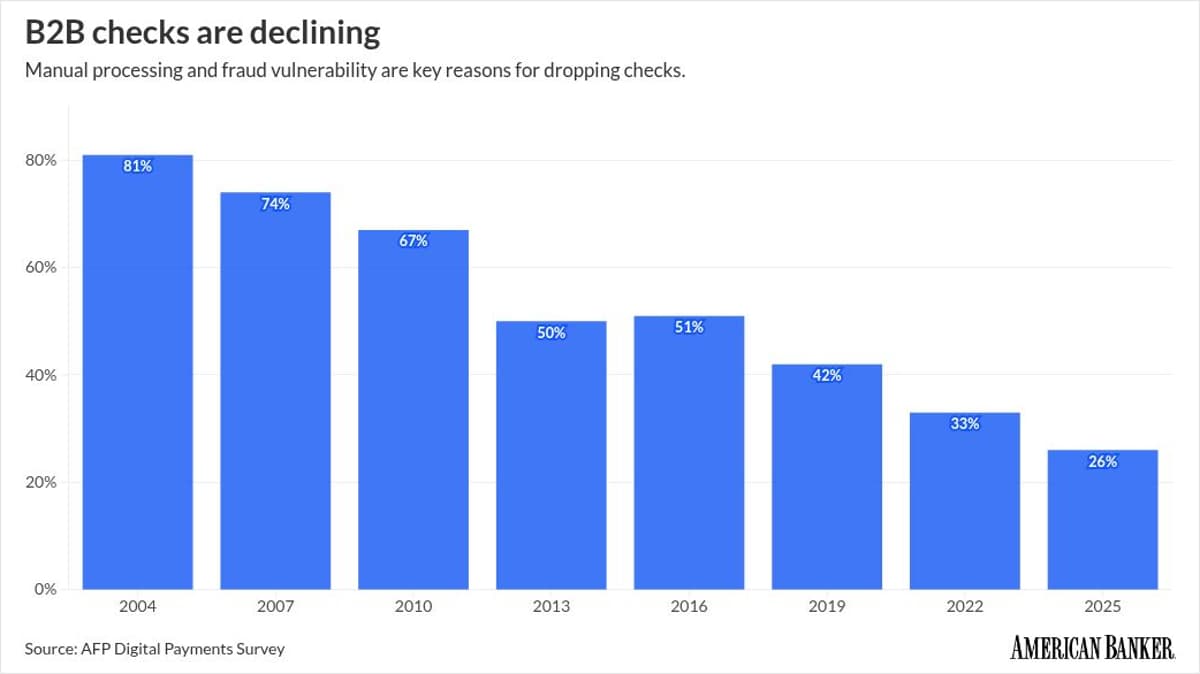

- •Checks now 26% of B2B payments, down 7 points

- •P2P volume rose 19.8% to 470 million

- •Real‑time rails still far behind ACH volume

Pulse Analysis

The ACH network posted a record 35.2 billion payments in 2025, representing a 5 percent increase over 2024 and moving the total value to $93 trillion. Growth was led by person‑to‑person transfers, which jumped 19.8 percent to 470 million transactions, and business‑to‑business payments, up 9.9 percent. At the same time, check usage in B2B contexts fell to 26 percent, a seven‑point drop since 2022, as firms chase lower‑cost, lower‑fraud alternatives. For banks, the shift means fewer deposits and reduced card‑interchange revenue as consumers park cash in digital wallets that settle over ACH.

Nacha’s proposal to raise the same‑day ACH per‑transaction ceiling from $1 million to $10 million would align the rail with the Clearing House’s RTP network and the FedNow instant‑payment service, both of which already support ten‑million‑dollar transfers. The higher limit could unlock larger corporate payments, making ACH a more attractive substitute for wire transfers and credit‑card settlements. New risk‑management rules slated for this year aim to curb business‑email‑compromise fraud by imposing baseline monitoring on all non‑consumer participants. Together, these changes could deepen ACH’s role in the payments ecosystem while preserving its low‑cost advantage.

Looking ahead, pay‑by‑bank initiatives from retailers such as Walmart and a growing roster of utilities and gas stations are feeding additional volume into the ACH system. Fintech platforms that aggregate consumer balances—Venmo, PayPal, and emerging digital‑banking apps—continue to divert funds from traditional deposit accounts, pressuring banks to innovate or partner. While real‑time rails are gaining traction, their transaction counts remain an order of magnitude lower than ACH’s monthly peak of 3.22 billion payments. Consequently, ACH is likely to remain the backbone of U.S. electronic payments for the foreseeable future, even as competition intensifies.

ACH volume is soaring. Here's how that threatens banks.

Comments

Want to join the conversation?

Loading comments...